If you're between 50 and 70 and wondering whether your life insurance policy can do more than pay a death benefit, you're asking exactly the right question. This permanent life insurance cash value guide breaks down how the savings component inside these policies actually works, which policy types fit different goals, and what mistakes can quietly erode the value you've spent years building. Whether you're focused on retirement income, legacy preservation, or protecting a business you've spent decades growing, understanding cash value is the foundation for making a smart decision.

Table of Contents

- Key takeaways

- Understanding permanent life insurance and cash value

- How cash value grows over time

- Accessing your cash value: what you need to know

- Choosing the right policy for your goals

- Common mistakes that cost policyholders dearly

- My take on cash value life insurance after years in the field

- How Premier72 can help you build a smarter plan

- FAQ

Key takeaways

| Point | Details |

|---|---|

| Cash value grows tax-deferred | Your policy's savings component compounds without annual income tax, giving it a meaningful edge over taxable accounts. |

| Policy type determines growth style | Whole life offers guaranteed growth; indexed and variable universal life tie growth to market performance with varying risk. |

| Loans beat withdrawals | Borrowing against cash value is tax-free and keeps the policy intact; withdrawals reduce your death benefit permanently. |

| Surrender charges can last years | Early cancellation can wipe out accumulated value, with charges extending up to 16 years on some policies. |

| Match policy to your timeline | The right permanent life policy depends on your risk tolerance, retirement timeline, and legacy goals. |

Understanding permanent life insurance and cash value

Permanent life insurance is exactly what the name suggests: coverage designed to last your entire life, not just a set term. Unlike term insurance, which expires after 10, 20, or 30 years with no residual value, a permanent policy builds a cash value component alongside the death benefit. That cash value functions like a tax-sheltered savings account inside your policy, growing over time as you pay premiums.

Every premium payment you make gets split. One portion covers the cost of insurance and policy fees. The rest flows into the cash value account, where it grows on a tax-deferred basis, meaning you owe no annual income tax on the gains. That compounding effect over 10, 20, or 30 years can add up to a substantial asset.

There are four main types of permanent life insurance, each with a different approach to cash value growth:

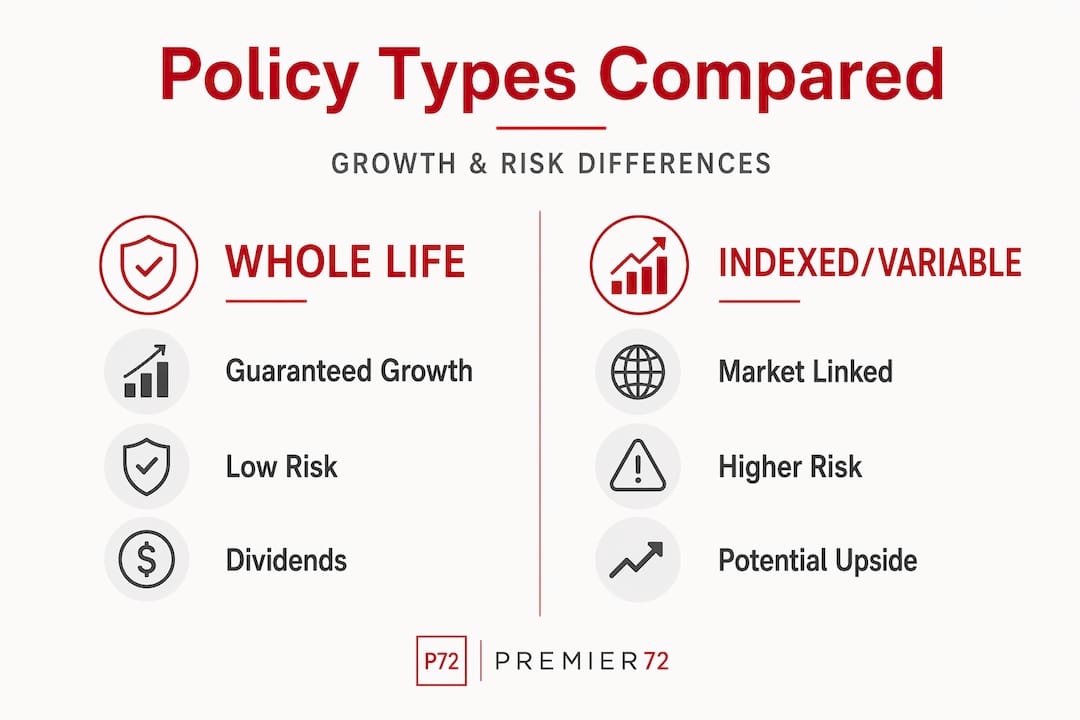

- Whole life: Guaranteed premiums, guaranteed death benefit, and guaranteed cash value growth. Predictable but typically slower growth.

- Universal life (UL): Flexible premiums and death benefit, with cash value tied to current interest rates. More adaptable than whole life.

- Indexed universal life (IUL): Cash value growth linked to a market index like the S&P 500, with a floor (often 0%) to protect against losses and a cap to limit gains.

- Variable universal life (VUL): Cash value invested in sub-accounts similar to mutual funds. Highest growth potential, but also the most investment risk.

Pro Tip: Permanent life insurance is 5 to 15 times more expensive than term for the same death benefit. Before committing, confirm you can sustain the premiums for the long haul.

How cash value grows over time

The mechanics of cash value growth vary significantly depending on which type of policy you hold. Understanding these differences is not optional. It directly determines how much you'll have available when you need it.

| Policy Type | Growth Mechanism | Risk Level | Downside Protection |

|---|---|---|---|

| Whole life | Guaranteed rate set by insurer | Low | Yes, fully guaranteed |

| Universal life | Based on current interest rates | Low to moderate | Partial (minimum interest floor) |

| Indexed universal life | Linked to index (e.g., S&P 500) | Moderate | Yes (0% floor typical) |

| Variable universal life | Sub-account investment performance | High | No guarantee |

Whole life policies grow at a rate the insurance company sets, often supplemented by dividends from mutual insurers. The growth is slow but certain. Universal life policies fluctuate with prevailing interest rates, which means years of low rates translate to slower accumulation.

Indexed universal life offers a middle ground that many in the 50-70 age group find appealing. Your cash value participates in index gains up to a cap, and a floor prevents losses in down years. You won't capture every bull market rally, but you also won't watch your policy value collapse in a recession.

Variable universal life carries real investment risk. In strong markets, growth can outpace every other policy type. In bad years, your cash value can drop. For someone at 65 relying on this as part of a retirement income strategy, that volatility deserves serious thought.

One factor that accelerates growth across all policy types is overfunding. Paying more than the minimum required premium pushes more money into the cash value account faster. Just be careful not to overfund past IRS limits, or your policy becomes a modified endowment contract (MEC), which changes the tax treatment of loans and withdrawals.

Pro Tip: Consistent premium payments in the early years of a permanent policy matter more than most people realize. Early contributions have the longest time to compound, so underpaying in years one through five can significantly reduce your long-term cash value.

Accessing your cash value: what you need to know

Having cash value is one thing. Knowing how to access it without triggering unintended tax bills or jeopardizing your coverage is another. There are three primary methods, and they are not equal.

-

Policy loans. You borrow against your cash value using it as collateral. Policy loans are tax-free and do not require credit approval. Your cash value continues earning interest or dividends even while the loan is outstanding. The catch: unpaid loans accrue interest, and if the outstanding balance grows large enough, it can trigger a policy lapse. If the policy lapses with an outstanding loan, the entire loan balance becomes taxable income.

-

Withdrawals. You can pull money directly from the cash value account. Withdrawals up to your basis (the total premiums you've paid) come out tax-free. Anything above that is taxable as ordinary income. Withdrawals also permanently reduce your death benefit, which matters if legacy planning is part of your goal.

-

Policy surrender. You cancel the policy entirely and receive the cash surrender value, which is the cash value minus any surrender charges and outstanding loans. Early surrender charges can extend up to 16 years on some policies and can seriously reduce what you actually receive.

One option worth exploring if long-term care is a concern: long-term care riders allow you to access your death benefit early if you cannot perform two of six activities of daily living or have a cognitive impairment. This gives your policy a dual purpose without requiring you to surrender it.

Pro Tip: Treat policy loans like a real debt. Set a repayment schedule and stick to it. Letting loan interest compound unchecked is one of the most common ways people accidentally lapse a policy they've been funding for decades.

Choosing the right policy for your goals

Not every permanent life policy fits every situation. At 55 with a 20-year runway before retirement, you have time to absorb some market risk and benefit from indexed or variable growth. At 68 with a near-term income need, guaranteed whole life growth may serve you better even if the returns are modest.

Here's a practical comparison to help frame the decision:

- Whole life suits people who want predictability, guaranteed growth, and a policy that won't surprise them. It works well for legacy planning where the death benefit amount matters more than maximizing cash value.

- Universal life offers flexibility if your income varies year to year, which is common for business owners. You can adjust premiums within limits, which helps during lean years.

- Indexed universal life fits people who want market-linked upside without the risk of actual loss. It's one of the more popular choices for the 50-70 group for exactly that reason.

- Variable universal life is appropriate only if you have a genuine risk tolerance and a longer time horizon. It is not a conservative retirement tool.

If you're considering converting a whole life policy to a hybrid long-term care policy through a 1035 exchange, note that minimum cash value thresholds around $50,000 are typically required to make the exchange work. Planning for that threshold takes time.

Watch for modified endowment contract (MEC) status. If you overfund a policy past the IRS's seven-pay test limit, it becomes a MEC. Loans and withdrawals from a MEC are taxed differently, with gains coming out first and subject to a 10% penalty if you're under 59½.

Common mistakes that cost policyholders dearly

Most of the damage people do to their permanent life policies comes from misunderstanding how the product works, not from bad intentions. These are the errors worth knowing before they happen to you.

- Surrendering too early. Surrender charges can extend up to 16 years. Canceling a policy in the first decade often means receiving far less than the premiums you've paid in.

- Ignoring loan interest. Policy loans don't demand monthly payments, which makes it easy to forget about them. Accruing interest compounds silently until it threatens the policy's survival.

- Overfunding into MEC territory. Paying in too much too fast can trigger MEC status, which removes the tax-free loan advantage that makes these policies attractive in the first place.

- Underestimating premium commitments. Permanent life insurance premiums are long-term obligations. Buying more coverage than your budget can sustain reliably is a setup for lapse.

- Confusing loans and withdrawals. They feel similar but have very different tax consequences. Loans are tax-free; withdrawals above your basis are taxable income.

- Treating life insurance as your only long-term care plan. Life insurance should not be your primary LTC strategy. It can serve as a secondary option, but relying on it exclusively leaves you exposed.

"The biggest mistake I see isn't buying the wrong policy. It's buying the right policy and then managing it poorly for 15 years."

My take on cash value life insurance after years in the field

I've worked with enough business owners and professionals in the 50-70 range to say this plainly: cash value life insurance is a genuinely useful tool, but it is not what some agents make it out to be.

The people who benefit most are those who have already maxed out their 401(k) and IRA contributions and need another tax-advantaged place to put money. They're not replacing investments with life insurance. They're adding a layer that serves a specific purpose: tax-deferred growth, a death benefit for legacy, and a policy loan mechanism that doesn't show up on a credit report.

What I've seen go wrong is when someone buys a variable universal life policy at 62 because the projected illustrations looked impressive. Those illustrations assume consistent market returns. Real markets don't cooperate on schedule. When cash value drops right before someone planned to start drawing from it, the whole strategy unravels.

My honest view: permanent insurance works best when it's protection first and accumulation second. If you're buying it primarily because someone told you it's a better investment than a brokerage account, that framing is worth questioning. 23% of Americans buy life insurance partly to build cash value, but traditional investments often deliver higher returns for those without a specific need for lifelong coverage.

The right policy is the one that matches your actual goals, not the one with the most compelling sales illustration.

— Asa

How Premier72 can help you build a smarter plan

At Premier72, we work with business owners, professionals, and families in exactly this stage of life. You've built something real. Now the question is how to protect it, grow it, and pass it on without leaving money on the table or making decisions you can't reverse.

Our team helps clients evaluate permanent life insurance options in the context of their full financial picture, including retirement income planning, business succession, key person coverage, and legacy strategies. We don't lead with product recommendations. We start with your goals, your timeline, and your risk tolerance, then work backward to find the structure that fits.

If you're exploring how cash value life insurance fits into your retirement or legacy plan, we'd welcome the conversation. Reach out to Premier72 to schedule a consultation and get clarity on which options actually make sense for where you are right now.

FAQ

What is permanent life insurance cash value?

Cash value is a tax-deferred savings component built into permanent life insurance policies. It grows over time as you pay premiums and can be accessed through loans or withdrawals during your lifetime.

How is cash value different from a term life policy?

Term life insurance provides a death benefit for a fixed period with no savings component. Permanent life insurance builds cash value over time, giving you a living benefit in addition to the death benefit.

Can I access cash value without paying taxes?

Policy loans against your cash value are tax-free and do not require repayment on a fixed schedule. Withdrawals up to the amount of premiums you've paid also come out tax-free; amounts above that are taxable as ordinary income.

What happens if I surrender my policy early?

Surrendering a permanent life policy in the early years triggers surrender charges that can significantly reduce or eliminate your accumulated cash value. These charges can last up to 16 years depending on the policy.

Is permanent life insurance a good retirement investment?

Permanent life insurance works best as a protection product with tax-advantaged accumulation as a secondary benefit. For those who have already maximized traditional retirement accounts, it can serve as a useful supplemental strategy, but it is rarely the most efficient standalone investment vehicle.