Most people assume life insurance is either too expensive or too complicated to bother with. That assumption costs families dearly. What is term life insurance, really? At its core, it's the most straightforward form of life coverage available: you pay a fixed premium for a set number of years, and if you die during that period, your beneficiaries receive a tax-free payout. No investment component, no mystery. Just protection during the years your family needs it most.

Table of Contents

- Key takeaways

- What is term life insurance and how does it work

- Term life vs. whole life: understanding the key differences

- Choosing the right term length and coverage amount

- Underwriting, policy options, and pitfalls to avoid

- Putting term life insurance to work in your financial plan

- My take on term life insurance

- How Premier72 can help you protect what matters

- FAQ

Key takeaways

| Point | Details |

|---|---|

| Fixed coverage window | Term life covers a defined period, typically 10 to 30 years, at a locked-in premium. |

| Affordable protection | A healthy 30-year-old can get meaningful coverage for as little as $20 to $30 per month. |

| Tax-free death benefit | Beneficiaries receive a lump-sum payout free of federal income tax if the policyholder dies during the term. |

| Conversion matters | Policies with conversion riders let you switch to permanent coverage later without a new medical exam. |

| Match term to obligations | Align your coverage period with your mortgage, dependent children, or income replacement window. |

What is term life insurance and how does it work

The term life insurance definition is simple: you purchase coverage for a fixed period, pay consistent premiums throughout, and your beneficiaries collect a death benefit if you pass away while the policy is active. When the term ends, coverage stops. There is no cash buildup, no investment account, and no refund of premiums paid.

Term lengths typically run 10, 15, 20, or 30 years. A 20-year policy bought at age 35 keeps you covered until 55. That window often lines up with the years when a mortgage is outstanding, children are still at home, or a surviving spouse would struggle to replace your income alone.

Premiums can be as low as $20 to $30 per month for a healthy 30-year-old, depending on coverage amount and term length. That affordability exists because the insurer is only covering mortality risk. There is no cash-value account being built behind the scenes, which is exactly what makes term so much cheaper than permanent alternatives.

Coverage is available from $50,000 to over $25 million, and beneficiaries receive a tax-free lump sum if the policyholder dies within the term with premiums current. The death benefit can pay off a mortgage, replace years of lost income, fund a child's education, or cover final expenses without creating a tax burden for the people left behind.

Pro Tip: When comparing policies, look at the death benefit per dollar of monthly premium, not just the headline coverage number. A $500,000 policy at $30/month is a very different value than one at $55/month for the same term and health class.

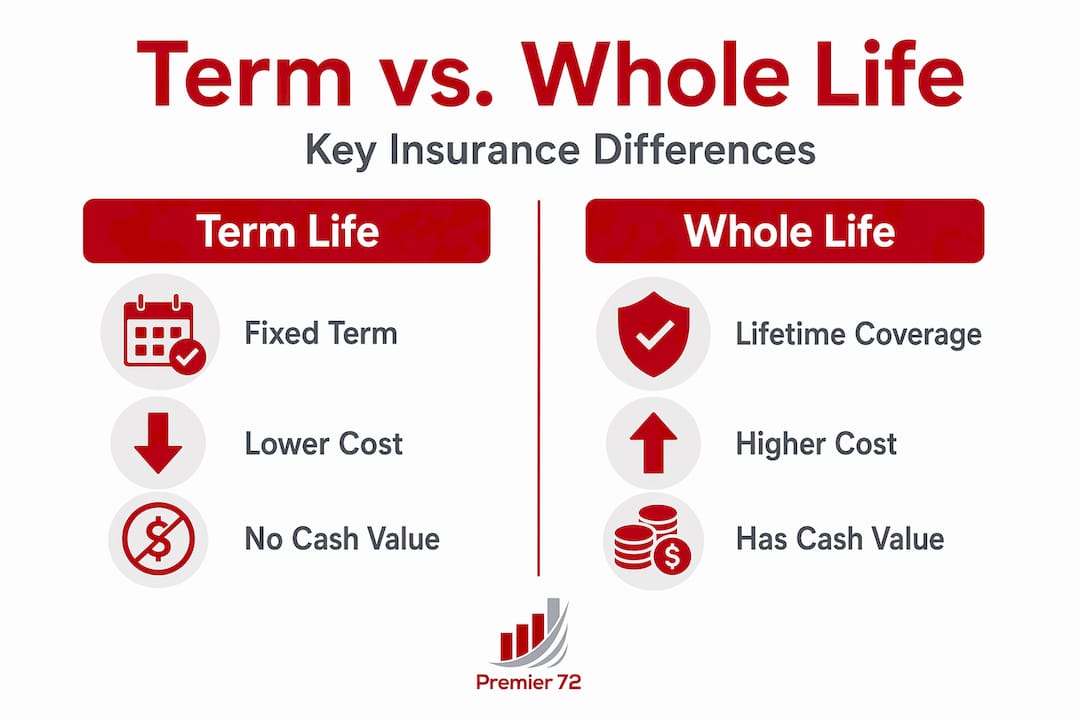

Term life vs. whole life: understanding the key differences

The term life insurance vs whole life debate comes down to one core question: do you need coverage for a defined period, or for your entire life? Each serves a different purpose, and confusing the two leads to either overpaying or under-protecting.

| Feature | Term life insurance | Whole life insurance |

|---|---|---|

| Coverage duration | Fixed term (10 to 30 years) | Lifetime |

| Monthly premiums | Low, fixed during term | Significantly higher |

| Cash value | None | Builds over time |

| Death benefit | Paid if death occurs in term | Paid regardless of timing |

| Best for | Income replacement, debt coverage | Estate planning, legacy transfer |

Term life is 5 to 10 times more affordable than permanent whole life insurance because it excludes the cash-value component. That difference is significant. A 40-year-old might pay $50/month for a 20-year term policy versus $500/month or more for an equivalent whole life policy.

The benefits of term life insurance are strongest when your financial obligations are time-bound. A mortgage gets paid off. Children grow up and become financially independent. At that point, term insurance can expire and the premium savings can be redirected to retirement accounts or other investments.

That said, term is not always the right call forever. Whole life policies carry different advantages for estate planning, business succession, or situations where permanent coverage is genuinely needed. Understanding which [whole life policies qualify](https://blog.acceleratedls.com/blog/why whole life policies qualify for life settlements) for certain financial strategies matters when you are thinking long-term.

Pro Tip: If you are unsure whether you will need permanent coverage down the road, buy a term policy with a strong conversion rider now. You lock in your current health rating and keep your options open without committing to the higher whole life premium today.

Choosing the right term length and coverage amount

This is where most people get stuck. They know they need coverage but have no framework for deciding how much or for how long. Here is a practical approach:

- Add up your financial obligations. Start with your mortgage balance, any outstanding loans, and estimated childcare or education costs. That total represents the minimum your family would need to stay financially stable without your income.

- Apply the income replacement rule. Financial planners recommend a death benefit equal to 10 to 12 times your annual salary as a general starting point. A household earning $80,000 per year should consider $800,000 to $960,000 in coverage.

- Match the term to your dependency timeline. If your youngest child is 3 years old and you want coverage until they finish college, a 20-year term makes sense. If you have 22 years left on your mortgage, a 25-year term lines up cleanly.

- Account for a spouse's income. If your partner earns enough to cover household expenses independently, you may need less coverage. If they do not work or earn significantly less, your coverage need goes up.

- Revisit the numbers every few years. Life changes. A second child, a new mortgage, or a career change can shift your coverage needs meaningfully.

4 in 10 U.S. adults reported having no life insurance as of early 2026. That gap often exists not because people don't care, but because they never had a clear framework for deciding what they actually need.

Pro Tip: Do not just calculate what you owe. Calculate what your family would need to maintain their lifestyle for 5 to 10 years without your income. Those two numbers are often very different.

Underwriting, policy options, and pitfalls to avoid

Understanding how underwriting works removes most of the anxiety from the application process. Insurers review your age, health history, family medical history, and lifestyle to set your premium rate. Younger and healthier applicants get better rates. That is why buying early, even when coverage feels unnecessary, is often the right financial move.

Lifestyle factors matter more than most people realize. Hobbies like scuba diving or private flying can affect your premiums or require working with carriers that specialize in higher-risk profiles. This is not apparent until you apply, which is why working with an experienced advisor before submitting an application saves time and money.

Here are the most common pitfalls to watch for:

- Ignoring conversion riders. Convertibility to permanent insurance without a new medical exam is one of the most valuable features in a term policy. If your health declines during the term, conversion keeps you insurable. Without it, you may not qualify for new coverage at any price.

- Letting the policy expire without a plan. Renewing an expired term policy triggers large premium increases based on your current age and health, not your original rate. This is the most common failure point for policyholders.

- Treating it as set-and-forget. The 'set it and forget it' approach is risky; maintaining awareness of policy expiration and conversion options prevents costly coverage gaps.

- Underbuying to save on premiums. A $250,000 policy feels affordable until you realize it covers less than three years of your family's living expenses.

Pro Tip: Set a calendar reminder 2 years before your policy's expiration date. That gives you time to convert, replace, or restructure coverage before health changes or age-based pricing work against you.

Putting term life insurance to work in your financial plan

Knowing what term life insurance is matters far less than actually using it correctly within your broader financial picture. Here is how to move from understanding to action:

- Get quotes before you need coverage urgently. Rates are best when you are healthy. Waiting until after a diagnosis or health event limits your options significantly.

- Work with an advisor who understands your full financial picture. Online quote tools are useful for ballpark numbers, but they do not account for business ownership, estate considerations, or key-person coverage needs that may require a different structure.

- Integrate coverage with your estate plan. A term policy with a named beneficiary bypasses probate entirely. That means faster access to funds for your family when they need it most.

- Review your coverage after major life events. Marriage, divorce, a new child, a business acquisition, or a significant income change all warrant a fresh look at your coverage amount and term length.

Term life insurance is best viewed as income replacement, not as a savings vehicle or investment. When you frame it that way, the decision becomes much cleaner. You are buying protection for a specific window of financial vulnerability, and when that window closes, the need for that particular coverage closes with it.

For those thinking about viatical settlements or other advanced strategies tied to life insurance policies, understanding how term converts to permanent coverage first gives you the most flexibility.

My take on term life insurance

I've worked with enough families and business owners to know that most people make life insurance harder than it needs to be. They either avoid it entirely because they assume it's expensive, or they buy the wrong product because someone sold them on features they don't actually need.

What I've found is that term life insurance, chosen correctly, is one of the cleanest financial decisions you can make. You identify a window of financial vulnerability, you cover it, and you move on. The mistake I see most often is not the wrong coverage amount. It's the wrong policy structure. People buy term without conversion privileges, then find themselves uninsurable at 55 when they actually need permanent coverage for estate or business reasons.

The other thing I've learned is that the conversion rider conversation almost never happens at the point of sale. Advisors focus on the premium, the death benefit, and the term length. The conversion feature gets treated as a footnote. In my experience, it's often the most strategically important feature in the entire policy, particularly for business owners who may need permanent coverage later for buy-sell agreements or key-person planning.

My honest advice: don't buy the cheapest term policy you can find. Buy the one with the best conversion privileges from a carrier with strong permanent products. The premium difference is usually small. The difference in flexibility years from now can be enormous.

— Asa

How Premier72 can help you protect what matters

Choosing the right term life coverage is straightforward once you have the right guidance. At Premier72, we work with business owners, professionals, and families to build protection strategies that fit their actual financial picture, not a generic template. Whether you need income replacement coverage for your family, key-person protection for your business, or a term policy structured with the right conversion privileges for long-term flexibility, we help you get it right from the start. We also integrate life insurance into broader legacy and exit planning strategies so your coverage works as part of a complete financial plan, not in isolation. Reach out to Premier72 today to get a personalized review of your coverage needs.

FAQ

What does term life insurance mean?

Term life insurance is a policy that provides a death benefit for a fixed period, typically 10 to 30 years, in exchange for regular premium payments. If the policyholder dies during that period, beneficiaries receive a tax-free lump sum.

How does term life insurance work when the term ends?

When the term expires, coverage stops and no benefit is paid. Policyholders can renew, but renewal premiums increase substantially based on current age and health. Converting to permanent coverage before expiration is often the smarter move.

Is term life insurance worth it for most families?

Yes. Term life insurance's simplicity and affordability make it the most practical starting point for anyone with dependents, a mortgage, or income others rely on. It covers your highest-risk financial years at the lowest possible cost.

Who needs term life insurance most?

Anyone whose death would create a financial hardship for others. That includes parents with young children, homeowners with a mortgage, business owners with partners or employees, and anyone whose income supports a spouse or dependent family member.

Can you convert term life insurance to permanent coverage?

Yes, if your policy includes a conversion rider. Conversion to permanent insurance without a new medical exam preserves your insurability regardless of health changes that occur after the original policy was issued.