Most Baby Boomer business owners think of life insurance as a death benefit. Full stop. But why life insurance is a retirement asset is a question worth sitting with, because permanent life insurance carries a second financial engine that most people never fully use. That engine is cash value. It grows quietly over time, tax-deferred, and it can be accessed during your lifetime to supplement retirement income, cover gaps, or protect your portfolio during a market downturn. This article breaks down how that works, what the tax rules actually say, and how to use it wisely.

Table of Contents

- Key takeaways

- Why life insurance is a retirement asset: the core mechanics

- Tax advantages and the risks you need to know

- Using life insurance as a buffer asset

- Life insurance versus other retirement assets

- Practical steps for business owners

- My take on what most owners get wrong

- How Premier72 helps you put this into practice

- FAQ

Key takeaways

| Point | Details |

|---|---|

| Cash value is a living benefit | Permanent life insurance builds tax-deferred cash value you can access before death through loans or withdrawals. |

| Policy loans can be tax-free | Loans against cash value are typically not taxable as long as the policy stays in force and does not lapse. |

| Buffer asset strategy works | Using policy loans during market downturns protects your investment portfolio from forced selling at low prices. |

| Policy design matters greatly | Policies built for retirement income need to prioritize early cash value growth, not just death benefit size. |

| Life insurance supplements, not replaces | Cash value rarely covers full retirement expenses alone and works best alongside IRAs, 401(k)s, and other assets. |

Why life insurance is a retirement asset: the core mechanics

Most people own term life insurance. It is affordable, straightforward, and does exactly one thing: pay a death benefit if you die during the coverage period. Term life provides only that death benefit, with no cash value built up over time. When the term ends, so does the policy. There is nothing to access, borrow against, or carry into retirement.

Permanent life insurance works differently. Whole life, universal life, and indexed universal life policies all include a cash value component that builds over time alongside the death benefit. Whole life policies offer a death benefit and tax-deferred cash value growth that can be used to supplement retirement income. That distinction is the entire foundation of why permanent life insurance qualifies as a retirement asset.

Here is how the mechanics break down:

- Premium allocation: A portion of each premium payment funds the death benefit. The remainder goes into the cash value account, where it grows over time.

- Tax-deferred growth: The cash value compounds without annual tax liability. You do not owe taxes on the growth each year the way you would with a taxable brokerage account.

- Policy loans: You can borrow against your cash value at any time, for any reason. The loan does not require credit approval, and the cash value itself continues to earn dividends or interest while the loan is outstanding.

- Withdrawals: You can also take direct withdrawals up to your cost basis, typically tax-free. Amounts above your basis may be taxable.

- Death benefit: Whatever cash value remains, plus the base death benefit, transfers income-tax-free to your beneficiaries. The death benefit is a federally income-tax-free guaranteed payout, making it a powerful legacy transfer tool.

Pro Tip: When comparing policy loans versus withdrawals, loans preserve your cash value's ability to keep earning dividends, while withdrawals permanently reduce the account balance. For retirement income planning, loans are almost always the better access method.

Tax advantages and the risks you need to know

The tax treatment of life insurance cash value is genuinely favorable. Cash value grows tax-deferred and loans against it are generally not treated as taxable income, provided the policy remains active. That combination gives you a retirement income source that does not show up on your tax return in the same way that IRA distributions or Social Security income does.

But there is a real risk that most people do not hear about until it is too late.

If your policy lapses or you surrender it while you have outstanding loans, the IRS treats the loan balance as a distribution. That means the entire outstanding loan amount, minus your cost basis, becomes taxable income in the year the policy terminates. A 2025 Tax Court ruling in Fugler v. Commissioner confirmed this directly, holding that taxable gain arises from loan discharge upon policy lapse. The tax bill can be substantial and arrives with no warning if you are not monitoring your policy.

"Tax court rulings underscore the importance of policy management to avoid costly taxable events during retirement life insurance use."

The practical takeaways on tax risk are worth spelling out clearly:

- Monitor your loan balance against your cash value every year, not just when you take a loan.

- Understand your policy's minimum cash value threshold. If loans erode it too far, the policy can lapse automatically.

- Work with your advisor to stress-test the policy under different loan and interest scenarios, especially if you plan to borrow heavily in early retirement.

- Keep records of your cost basis. This determines how much of any withdrawal is tax-free.

Effective retirement use of life insurance requires ongoing monitoring of loan balances to keep the policy in force and prevent unintended taxable distributions.

Using life insurance as a buffer asset

This is where the strategy gets genuinely interesting for business owners who have built real wealth.

Sequence-of-returns risk is one of the most underappreciated threats in retirement planning. It refers to the danger of experiencing significant market losses in the early years of retirement, when you are also drawing down your portfolio. Selling investments at depressed prices to fund living expenses locks in losses and permanently reduces the capital available for recovery. The math is unforgiving.

Life insurance cash value offers a solution. Policy loans during market losses can help you avoid forced selling, allowing your investment portfolio time to recover. Instead of liquidating equities at the bottom of a downturn, you draw on your policy loan to cover expenses. When markets recover, you resume portfolio withdrawals and repay the loan, or simply let it reduce the eventual death benefit.

Here is a simplified comparison of outcomes with and without a buffer asset strategy:

| Scenario | Without buffer asset | With buffer asset |

|---|---|---|

| Market drops 30% in year 2 of retirement | Must sell investments at a loss to fund expenses | Draw policy loan; investments stay intact |

| Portfolio recovery potential | Permanently impaired by forced selling | Full recovery possible with time |

| Long-term portfolio balance | Significantly lower | Substantially preserved |

| Legacy outcome | Reduced inheritance | Death benefit plus recovered portfolio |

Permanent life insurance can shift a retirement portfolio's efficient frontier by providing a low-volatility, tax-advantaged cash position that does not move with the stock market. Financial planners increasingly treat it as a non-correlated asset, not just a protection product.

Pro Tip: For the buffer strategy to work, the policy needs to be designed with maximum early cash value in mind. Traditional whole life policies sometimes emphasize death benefit size over early cash value, which limits your income flexibility. Ask your advisor specifically about paid-up additions and early cash value optimization.

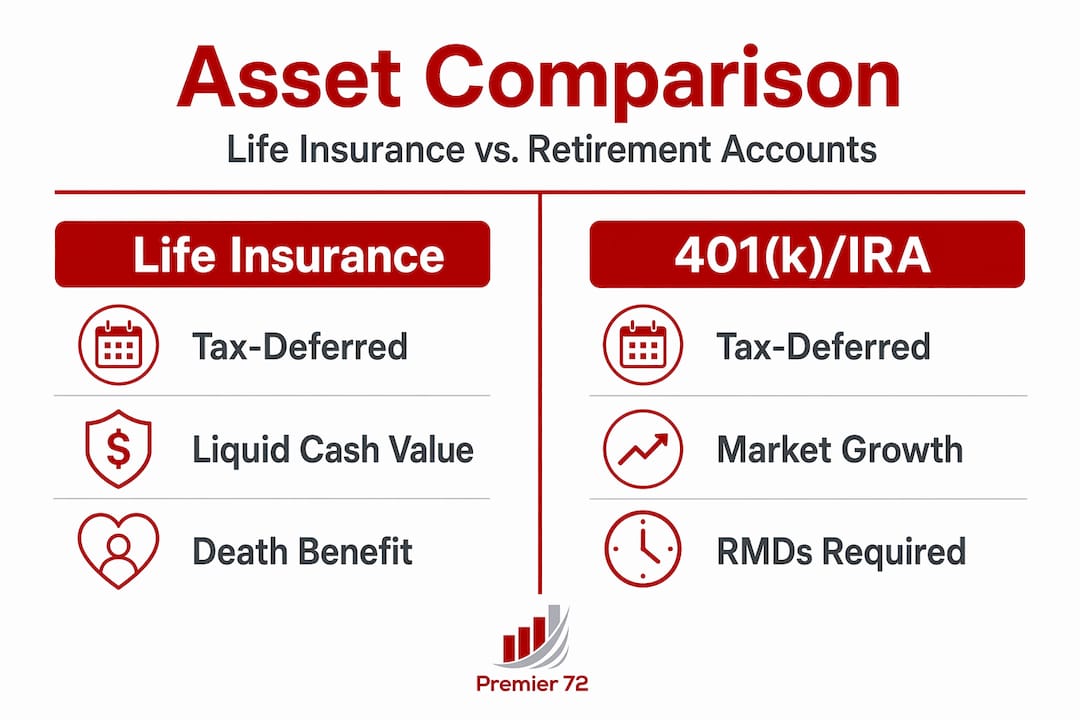

Life insurance versus other retirement assets

Understanding the benefits of life insurance for retirement requires honest comparison. Life insurance is not trying to beat your 401(k). It serves a different purpose, and knowing where it fits prevents both over-reliance and dismissal.

| Feature | Permanent life insurance | 401(k) / IRA | Annuity |

|---|---|---|---|

| Tax-deferred growth | Yes | Yes | Yes |

| Tax-free income access | Yes (via loans) | No (taxable distributions) | Partial |

| Death benefit to heirs | Yes, income-tax-free | Subject to income tax | Varies by contract |

| Market risk | Low to none | High | Low to moderate |

| Contribution limits | No IRS limit | Annual IRS limits apply | Varies |

| Liquidity | Good, via loans | Limited before 59½ | Often restricted |

| Long-term return potential | Lower than equities | Higher over long horizons | Moderate |

Life insurance cash value should supplement other retirement assets rather than replace them. The cash value available in most policies simply is not large enough to fund full retirement living expenses on its own. What it does exceptionally well is provide tax-advantaged liquidity, legacy transfer, and portfolio protection that other vehicles cannot replicate.

For business owners, the dual benefit is particularly relevant. Permanent life insurance's dual benefits make it uniquely suited for owners balancing retirement income needs with the desire to transfer wealth to the next generation or fund a buy-sell agreement.

You should also understand the trade-off: accessing cash value through loans reduces the death benefit available to your heirs. Loans use cash value as collateral while allowing it to stay invested, but unpaid loans are deducted from the death benefit at the time of claim. Modeling both buckets separately, cash value for living needs and death benefit for legacy goals, helps you plan both without conflict.

Practical steps for business owners

If you are a Baby Boomer business owner evaluating whether retirement planning with life insurance makes sense for your situation, here is a practical framework to get started.

- Identify your retirement income gaps. Calculate what your expected income sources (Social Security, business sale proceeds, investment accounts) will cover versus what you actually need. Life insurance cash value can fill specific gaps, not the entire picture.

- Define your legacy goals. Are you trying to transfer wealth to children, fund a charitable gift, or provide for a surviving spouse? The death benefit size and structure should reflect those goals clearly.

- Choose the right policy type. Whole life offers guaranteed cash value growth and dividends. Indexed universal life ties growth to a market index with downside protection. Work with an advisor who can model both against your specific retirement timeline.

- Prioritize cash value in the policy design. Ask for illustrations that show cash value at ages 65, 70, and 75, not just the death benefit. A policy designed for retirement access looks different from one designed purely for protection.

- Set up annual policy reviews. Track loan balances, cash value growth, and dividend performance every year. This is not a set-and-forget asset.

Pro Tip: Life insurance fits naturally alongside business continuity planning. Key person coverage, buy-sell funding, and personal retirement income strategies can all draw from the same permanent policy framework, making the premium dollars work harder across multiple goals.

My take on what most owners get wrong

I have worked with enough Baby Boomer business owners to know that the most common mistake is not buying the wrong policy. It is buying the right policy for the wrong design. Whole life insurance sold primarily for its death benefit will underperform as a retirement income tool. The cash value builds slowly, the early years look terrible on paper, and most owners surrender the policy before it reaches its potential.

What I have seen work is a policy built from day one with retirement access in mind. That means paid-up additions, higher premium funding relative to the death benefit, and a clear plan for when and how loans will be taken. It also means treating the policy as part of a coordinated financial strategy, not a standalone product.

The other thing I would say plainly: do not let anyone sell you life insurance as a replacement for your 401(k) or investment portfolio. It is not. The long-term returns do not compete with equities over a 20-year horizon. What it offers is something different: stability, tax-favored access, and a death benefit that passes to your heirs without the income tax burden that retirement accounts carry. That combination has real value. Just understand what you are buying and why.

— Asa

How Premier72 helps you put this into practice

At Premier72, we work specifically with Baby Boomer business owners who are thinking seriously about retirement income, legacy protection, and what happens to the wealth they have spent decades building. Life insurance is one piece of a larger strategy that includes business continuity planning, exit readiness, and income protection. Our team helps you evaluate whether permanent life insurance fits your retirement picture, design policies built for cash value access rather than just death benefit size, and coordinate coverage with your broader financial plan. If you want a clear-eyed look at how to use life insurance in retirement as part of a real strategy, start the conversation with Premier72 today.

FAQ

What makes permanent life insurance a retirement asset?

Permanent life insurance builds cash value over time that you can access through loans or withdrawals during your lifetime. That cash value grows tax-deferred and can supplement retirement income without triggering income tax, as long as the policy stays in force.

Are policy loans from life insurance taxable?

Policy loans are generally not taxable income while the policy remains active. However, if the policy lapses or is surrendered with outstanding loans, the IRS treats the loan balance as a taxable distribution, as confirmed by a 2025 Tax Court ruling.

Is life insurance a good investment for retirement?

Life insurance is not a replacement for market-based investments, but it serves as a strong supplement. It offers tax-deferred growth, tax-favored access, portfolio protection during downturns, and an income-tax-free death benefit, features that traditional retirement accounts do not fully replicate.

How does a buffer asset strategy work in retirement?

A buffer asset strategy uses policy loans to cover living expenses during market downturns, preventing forced selling of investments at depressed prices. This protects portfolio longevity and gives your investments time to recover before you resume withdrawals.

Can whole life insurance policies be used for other financial purposes?

Yes. Whole life policies can fund buy-sell agreements, provide key person coverage for businesses, and serve legacy transfer goals. Whole life policies qualify for life settlements as well, offering additional exit options if your needs change.