A life insurance policy review is a systematic assessment of your existing coverage, beneficiaries, and contract terms to confirm they still match your current financial situation and family goals. Most people buy a policy and file it away, never revisiting it until a crisis forces the issue. That approach leaves families exposed. Coverage that made sense when you were 32, single, and renting an apartment may be dangerously inadequate at 45 with a mortgage, two kids, and a business partnership. The life insurance policy review steps outlined here give you a structured process to close those gaps before they cost someone you love.

What documents do you need before starting a policy review?

The life insurance evaluation process starts with paper, not analysis. You cannot evaluate what you cannot see, and many policyholders discover mid-review that they are missing critical documents. Gathering all related documents before you begin, including the original policy, riders, amendments, proof of premium payments, and recent statements, is the foundation of any credible review.

Here is the full life insurance policy checklist of documents to collect:

- Original policy contract: The master document that defines your coverage terms, exclusions, and obligations.

- All riders and amendments: Riders for disability waiver, accelerated death benefit, or long-term care can carry significant value that the cover page never mentions.

- Recent premium payment records: Confirms you are current and identifies any lapses or grace period issues.

- Policy statements or annual reports: For permanent policies, these show current cash value, loan balances, and dividend history.

- In-force illustrations: For universal life or whole life policies, these projections show how the policy performs under current assumptions going forward.

- Insurer and agent contact information: You will likely need to request updated documents or ask questions during the review.

Pro Tip: Request an updated in-force illustration directly from your insurer before the review. Insurers are required to provide one, and it gives you a current performance snapshot that a years-old policy statement cannot.

If you hold a term policy, the document list is shorter. If you hold a universal life or whole life policy, the in-force illustration is non-negotiable. Permanent policy reviews require this document to assess funding status and avoid the risk of a policy lapsing unexpectedly.

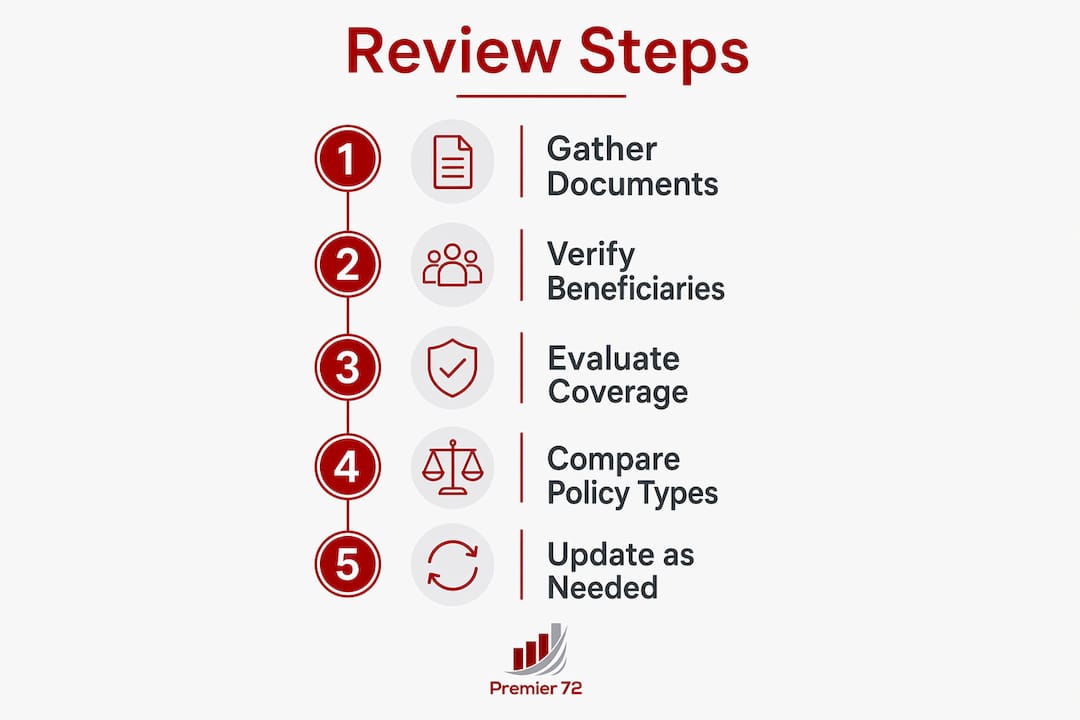

How do you systematically review coverage, beneficiaries, and contract details?

This is the core of the life insurance policy audit, and it works best as a numbered sequence. Jumping between topics creates gaps. Work through each element in order.

-

Confirm owner and beneficiary information. Verify that the policy owner, insured, and all named beneficiaries are accurate. Check full legal names, Social Security numbers, and relationships. Outdated beneficiary data from events like marriage, divorce, or a beneficiary's death can delay or complicate payouts significantly.

-

Evaluate your coverage amount against current needs. Your death benefit should cover outstanding debts, replace lost income, and fund future obligations. Many financial professionals recommend 10 to 15 times annual income as a baseline for families with dependents. Run the math against your mortgage balance, childcare costs, college funding goals, and any business obligations.

-

Review all riders and contract features. Riders and contract provisions often carry the most practical value in a policy, yet most policyholders never read them after signing. A disability waiver of premium rider, for example, keeps your policy active if you become disabled and cannot pay premiums. Know what you have.

-

Check loan and withdrawal history for permanent policies. Policy loans reduce the death benefit and can trigger a lapse if the loan balance grows faster than the cash value. Reviewing loan and withdrawal balances is a required step for any universal or permanent policy review. If you have outstanding loans, calculate the impact on your death benefit now, not later.

-

Assess premium affordability and payment schedule. A policy you cannot afford to maintain is not protection. Confirm that your current premium fits your budget and that no payment schedule changes have occurred without your knowledge.

-

Run or request updated in-force illustrations. For universal life policies especially, in-force illustrations and loan history reveal whether the policy is on track or quietly underfunded. A policy that looks fine on the surface can be heading toward lapse if interest crediting rates have dropped since the original illustration was run.

Pro Tip: Do not rely on the policy cover page alone. The cover page shows the face amount and issue date. The real value and risk sit inside the riders, loan provisions, and contract language that most people never read.

Here is a quick comparison of what term and permanent policy reviews require:

| Review element | Term life policy | Universal or permanent life policy |

|---|---|---|

| Beneficiary check | Required | Required |

| Coverage amount evaluation | Required | Required |

| Rider review | Recommended | Required |

| In-force illustration | Not applicable | Required |

| Loan and withdrawal history | Not applicable | Required |

| Cash value assessment | Not applicable | Required |

The difference is real. Reviewing your life coverage on a term policy takes roughly an hour with the right documents. A permanent policy review is a deeper process that can take several hours and may require direct contact with your insurer or a licensed advisor.

When and why should you update your policy or beneficiaries?

Insurance providers recommend reviewing your policy at least annually and immediately after any significant life event. The logic is straightforward. Your life changes faster than your paperwork does.

The most common triggers for a policy update include:

- Marriage or divorce: A new spouse should almost always be added as a primary beneficiary. A divorce may require removing an ex-spouse, though some states automatically revoke beneficiary designations upon divorce and some do not.

- Birth or adoption of a child: New dependents increase your coverage needs and require beneficiary updates.

- Home purchase: A new mortgage is a major liability that your death benefit should be able to cover.

- Job change or income shift: A significant income increase or decrease changes both your coverage needs and your premium affordability.

- Retirement: Coverage needs often shift at retirement. Some obligations disappear; others, like supporting a surviving spouse, remain.

- Death of a named beneficiary: If a primary beneficiary dies before you and you have not named a contingent beneficiary, the death benefit may pass through probate.

Beneficiary errors are not just administrative inconveniences. They become legal and financial roadblocks during the worst moments of a family's life. Treat every beneficiary update as a formal, documented transaction.

Updating beneficiaries requires submitting the insurer's official Change of Beneficiary form with full legal names and identifying information, then obtaining written confirmation from the insurer. Keep that confirmation on file. Verbal updates and informal requests do not hold up during claims. This is a controlled-document process, and treating it as anything less creates risk.

What are the most common mistakes during a policy review?

Most policy review errors are not complicated. They are oversights that compound over time.

- Skipping beneficiary updates after life events. Beneficiary designations require time-sensitive reviews because errors become administrative and legal roadblocks during claims. A divorce finalized three years ago means nothing if the ex-spouse is still listed as primary beneficiary.

- Relying only on the cover page. The death benefit amount is one number. The contract features and riders define what the policy actually does and when. Ignoring them is like reading only the title of a legal contract.

- Neglecting loan history on permanent policies. Policy loans accrue interest. If you borrowed against your cash value years ago and never repaid it, that balance may now be large enough to threaten the policy's viability.

- Not documenting submitted changes. Submitting a beneficiary change form without obtaining written confirmation from the insurer leaves you with no proof the change was processed.

- Assuming coverage is still adequate. A $500,000 policy purchased in 2010 may have covered your needs then. With inflation, a larger mortgage, and additional dependents, that same amount may now fall short.

Pro Tip: After submitting any policy change, follow up in writing and request a confirmation letter or updated policy page. File it with your original policy documents. This single habit prevents the majority of claim disputes.

Reviewing your term life insurance coverage annually against your family's evolving needs is the simplest way to catch these errors before they become permanent problems.

Key takeaways

A complete life insurance policy review requires verifying beneficiaries, evaluating coverage against current debts and dependents, auditing contract features and riders, and for permanent policies, running updated in-force illustrations to confirm the policy is properly funded.

| Point | Details |

|---|---|

| Gather documents first | Collect the original policy, riders, statements, and in-force illustrations before starting any review. |

| Beneficiary accuracy is critical | Outdated beneficiary designations cause claim delays; update them after every major life event. |

| Permanent policies need deeper review | Universal and whole life policies require in-force illustrations and loan history checks that term policies do not. |

| Coverage amount needs recalculation | Measure your death benefit against current debts, dependents, and future expenses, not the figure you chose years ago. |

| Document every change | Submit official insurer forms and obtain written confirmation for all beneficiary or coverage updates. |

Why most people get this wrong until it's too late

I have sat with families who discovered, after a loss, that the beneficiary on a $750,000 policy was an ex-spouse from a marriage that ended a decade earlier. The insurer paid the ex-spouse. The current family had no legal recourse. That outcome was not the result of a bad policy. It was the result of a review that never happened.

What surprises most people when they actually work through the steps to evaluate insurance is how much has changed since they signed the original application. Income is higher. Debts are different. Children have arrived. Business interests have grown. The policy that was "good enough" at signing is often misaligned by the time anyone looks at it again.

The other thing I see consistently is that people treat the death benefit number as the whole story. It is not. The riders, loan provisions, and contract language are where the real flexibility and risk live. A policy with a chronic illness rider, for example, can pay benefits while you are still alive if you meet the qualifying conditions. Most policyholders have no idea that feature exists in their own contract.

My advice is simple. Schedule a policy review the same way you schedule a physical. Once a year, no exceptions. After any major life event, immediately. Bring your documents, request an in-force illustration if you hold a permanent policy, and work through the checklist with someone who knows what they are reading. The whole life versus term comparison matters less than whether the policy you hold actually fits your life right now.

— Asa

How Premier72 can help you review and protect what matters

Reviewing a life insurance policy is straightforward when you know what to look for. When you are managing a family, a business, or both, the details get complicated fast.

Premier72 works with business owners, professionals, and families to review existing coverage, identify gaps, and build protection strategies that align with real financial goals. Whether you need a second opinion on a permanent policy's funding status, help updating beneficiary structures, or a full legacy planning conversation, Premier72 brings the advisory depth to make those decisions with confidence. If you are ready to take the next step, start with Premier72 and get clarity on whether your coverage is actually working for you.

FAQ

How often should you review your life insurance policy?

Insurance providers recommend reviewing your policy at least once per year and immediately after major life events such as marriage, divorce, childbirth, home purchase, or retirement.

What is the difference between reviewing a term and a permanent policy?

Term policy reviews focus on coverage amount and beneficiary accuracy. Permanent and universal life policy reviews also require in-force illustrations and a loan and withdrawal history check to confirm the policy is properly funded.

How do you update a beneficiary on a life insurance policy?

Updating a beneficiary requires completing the insurer's official Change of Beneficiary form with full legal names and identifiers, submitting it to the insurer, and keeping written confirmation on file.

How much life insurance coverage does a family need?

Many financial professionals recommend 10 to 15 times annual income as a starting baseline, adjusted for outstanding debts, number of dependents, and future expenses like college tuition or a surviving spouse's retirement income.

What happens if you never update your beneficiary designations?

Outdated beneficiary designations can direct death benefits to unintended recipients, including ex-spouses or deceased individuals, and the insurer is legally obligated to pay whoever is named on file regardless of your current wishes.