Most people assume their health insurance will handle everything if they get seriously sick. It won't. Critical illness insurance, formally known as critical illness coverage, exists precisely because a cancer diagnosis or heart attack creates financial damage that goes far beyond hospital bills. Lost income, mortgage payments, childcare, travel to treatment centers — none of that shows up on a medical invoice. Understanding what is critical illness insurance, and what it actually does, can mean the difference between financial recovery and financial ruin.

Table of Contents

- Key takeaways

- What critical illness insurance is and how it works

- Benefits and limitations worth understanding

- How critical illness insurance compares to other coverage types

- Choosing the right critical illness policy

- My honest perspective on this coverage

- How Premier72 can help you protect what you've built

- FAQ

Key takeaways

| Point | Details |

|---|---|

| Lump sum on diagnosis | You receive a one-time cash payment when diagnosed with a covered illness, not reimbursement for specific bills. |

| Flexibility defines the value | The payout can cover medical costs, living expenses, lost income, or anything else you choose. |

| Pre-existing conditions aren't covered | Policies use "first after" rules, covering only illnesses diagnosed after your policy starts. |

| It fills gaps other insurance misses | Critical illness coverage works alongside health, life, and disability insurance, not instead of them. |

| Policy definitions drive claim outcomes | How your insurer defines a covered condition directly affects whether your claim gets approved. |

What critical illness insurance is and how it works

Critical illness insurance is a supplemental policy that pays a one-time lump sum upon diagnosis of a serious illness such as cancer, a heart attack, or a stroke. Unlike traditional health insurance, which reimburses specific medical expenses, this payout goes directly to you with no requirement to submit receipts or justify how you spend it.

The mechanism is straightforward. You purchase a policy, pay regular premiums, and if you are diagnosed with one of the illnesses listed in your policy, you file a claim and receive the agreed payout amount. That amount is typically a fixed sum you selected when you enrolled, often ranging from $10,000 to $100,000 or more depending on the policy.

What most policies cover:

- Cancer (most types, with some exclusions for early-stage or non-invasive forms)

- Heart attack

- Stroke

- Major organ transplant

- Kidney failure

- Coronary artery bypass surgery

- Multiple sclerosis

- Paralysis

Coverage lists vary significantly between insurers, so reviewing the specific conditions named in any policy before purchasing is non-negotiable.

Two underwriting concepts shape who qualifies and when claims trigger. The first is the first after rule, which means coverage applies only to conditions diagnosed after the policy takes effect. The second is the pre-existing condition exclusion. Underwriting assumes the insured is in good health at enrollment, so illnesses you already have or have been treated for before purchasing are excluded from coverage.

Pro Tip: Apply for critical illness coverage while you are still healthy. Premiums are lower, your options are broader, and you won't face exclusions for conditions that haven't developed yet.

The lump sum itself is what makes this product powerful. No receipt submission is required, and you can use the money for medical deductibles, rent, groceries, travel to specialized care, or paying down debt while you recover. That flexibility is the core value proposition.

Benefits and limitations worth understanding

The financial protection benefits of critical illness insurance are real, but they come with meaningful limits. Knowing both sides helps you make a smarter coverage decision.

Where critical illness coverage genuinely delivers:

Critical illness insurance provides flexibility to pay for both medical and nonmedical expenses upon diagnosis. Your regular health plan might cover your surgery, but it won't cover the three months of mortgage payments you miss while recovering. It won't replace your lost income or pay for the flight your spouse takes to be with you at a treatment center across the country. The lump sum handles all of that.

Tax treatment is another advantage worth noting. In many cases, payouts are often tax-free, though tax treatment varies by jurisdiction and how the policy is structured. If your employer pays your premiums, for example, the tax treatment of the benefit may differ. Verify this with a financial advisor based on your specific situation.

"The payout isn't about covering what your health insurance missed. It's about keeping your financial life intact while you focus on getting well. That distinction is what most people don't realize until they actually need it."

Where the limitations bite:

Critical illness insurance policies vary widely in definitions, qualifying conditions, and payout criteria. A "heart attack" under one policy might require specific enzyme level thresholds or EKG changes. If your diagnosis doesn't meet the exact wording, the claim is denied.

Some insurers require a survival period after diagnosis before the payout is released. A 14-day survival requirement is common. If the insured passes away before meeting that threshold, the claim may not pay out at all.

Additional limitations to factor in:

- No payout if you never make a claim, since most policies carry no cash value

- Higher premiums for older applicants or those with a complicated health history

- Coverage gaps for illnesses not named in the policy, regardless of severity

- Strict diagnosis triggers that may exclude less severe versions of covered conditions

Understanding these limitations isn't discouraging. It's how you shop smarter and ask better questions before signing.

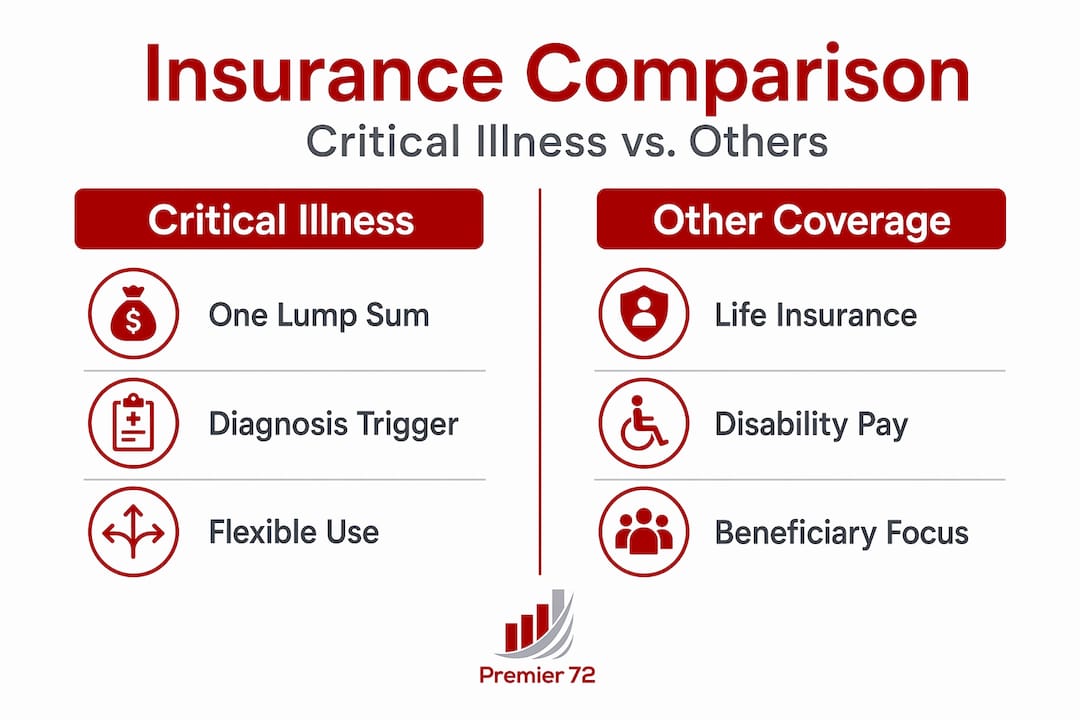

How critical illness insurance compares to other coverage types

The importance of critical illness insurance becomes clearest when you see how it fits alongside the other policies most people already carry.

Life insurance pays your beneficiaries when you die. Disability insurance replaces a portion of your income if you cannot work due to illness or injury. Critical illness insurance provides financial protection while you are alive, covering the financial disruption that happens during your diagnosis and recovery, regardless of whether you return to work.

These three products solve different problems. They are not interchangeable.

| Feature | Critical Illness Insurance | Life Insurance | Disability Insurance |

|---|---|---|---|

| When it pays | Upon covered diagnosis | Upon death | When unable to work |

| Payout type | Lump sum, one time | Lump sum to beneficiaries | Monthly income replacement |

| Who receives it | The insured, directly | Named beneficiaries | The insured |

| Use of funds | Unrestricted | Typically estate or family | Living expenses |

| Covers non-medical costs | Yes | Indirectly | Partially |

Critical illness coverage addresses short-term financial disruption in a way disability insurance doesn't fully cover, especially during the waiting period before disability benefits kick in. Many disability policies have elimination periods of 60 to 90 days before payments start. A critical illness lump sum can bridge that window directly.

Think of the combination this way. Life insurance protects your family if you're gone. Disability insurance sustains your income if you can't work. Critical illness coverage protects your financial stability the moment a serious diagnosis lands, before any of those other systems engage. For more on how disability coverage fits into this layered approach, the disability income insurance guide from Premier72 covers the specifics in detail.

Pro Tip: If you're a business owner, critical illness insurance takes on additional weight. Your business doesn't stop generating expenses because you're in treatment. A lump sum can fund operations, hire temporary help, or buy time for a succession plan to activate.

Choosing the right critical illness policy

Asking "should I get critical illness insurance" is the wrong starting question. The better question is: which policy structure actually fits my risk profile and financial plan?

Here's how to approach that decision with clarity:

-

List the conditions covered. Count how many conditions are explicitly named in the policy. Some basic policies cover as few as three. More comprehensive policies may cover 30 or more. The list matters because a condition not named is a condition not covered, regardless of how serious it is.

-

Examine the definitions, not just the names. A policy that covers "heart attack" means nothing until you read how the insurer defines it. Look for the clinical thresholds required for a valid claim. Policy definitions and claim requirements such as survival periods significantly affect whether a claim gets approved.

-

Assess your family history honestly. If heart disease runs in your family, or you have a genetic predisposition toward certain cancers, that information should drive both how much coverage you seek and when you buy it. The sooner you apply, the less likely those risks have already manifested.

-

Compare survival period requirements. A 14-day survival period is standard for many policies, but some require 30 days. If you're comparing two otherwise identical policies, the shorter survival period is almost always preferable.

-

Evaluate the insurer's claims reputation. Premium cost is not the only metric. Research the insurer's claim approval rates and read reviews from actual policyholders who filed claims. An inexpensive policy from a company that routinely disputes claims is not a good deal.

Pro Tip: Ask your insurer for the specific claims payout percentage before purchasing. Reputable insurers will share this data. A low payout ratio is often a signal that definitions are written to minimize approvals.

For business owners, integrating critical illness coverage into a broader financial plan means considering how a serious illness would affect not just personal finances but also key person obligations and business continuity. The disability insurance for business owners breakdown at Premier72 covers the business angle thoroughly.

My honest perspective on this coverage

I've worked with enough business owners and families going through serious health crises to know that the financial stress often outlasts the medical crisis itself. The bills stop, but the income gap doesn't close overnight. That's where I've seen critical illness coverage actually matter. Not as a product to sell, but as a tool that buys time and reduces panic when someone most needs to focus on recovery.

What conventional advice gets wrong is framing this as a luxury or an optional add-on. For anyone with a mortgage, dependents, or a business that depends on their presence, a serious diagnosis without a lump sum payment in reserve is a financial emergency layered on top of a health emergency.

The lump sum feature is genuinely empowering in a way monthly benefits are not. You receive money, and you decide what it's for. No prior authorizations. No claims adjusters asking for proof of how you spent Tuesday. That control matters enormously when everything else in your life feels out of your hands.

I also think most people wait too long to buy it. They apply after a health scare, which is when underwriting gets complicated and coverage gets expensive. The first after diagnosis rule is an underwriting reality that rewards early applicants. If you're healthy today and in your 30s or 40s, this is the moment to explore coverage, not after your next physical reveals a concern.

Critical illness coverage isn't a replacement for a thoughtful financial protection plan. It's one layer of a layered strategy, alongside life insurance, disability coverage, and long-term retirement planning. Done right, you should hope you never use it. And if you do, you'll be grateful it was there.

— Asa

How Premier72 can help you protect what you've built

A serious illness doesn't just affect your health. It can destabilize your business, derail your retirement timeline, and put your legacy at risk before you've had a chance to secure it. At Premier72, we help business owners, professionals, and families build financial protection strategies that account for the unexpected, including critical illness coverage designed to protect both personal finances and business continuity. Whether you're looking to layer critical illness coverage into an existing plan or starting from scratch, our advisors work through the specifics with you to ensure your protection strategy fits your actual life, not a generic template. Understanding term life insurance options is often the starting point, but critical illness coverage is where many protection plans have their most significant gaps.

FAQ

What does critical illness insurance cover?

Most policies cover cancer, heart attack, stroke, kidney failure, major organ transplant, and coronary artery bypass surgery, though covered conditions vary by insurer. Always review the policy's named conditions and clinical definitions before purchasing.

How does critical illness insurance work?

You pay premiums, and if you're diagnosed with a covered illness after your policy takes effect, you receive a lump sum payment directly. No receipts are required, and you can use the funds for any expense, medical or otherwise.

Is the critical illness insurance payout taxable?

In many cases the payout is tax-free, but tax treatment depends on your location and how your premiums are structured. If your employer pays the premiums, the benefit may be taxable, so confirming with a financial advisor for your specific situation is worthwhile.

Should I get critical illness insurance if I already have health insurance?

Yes, because health insurance covers medical bills while critical illness coverage replaces lost income, pays living expenses, and covers costs your health plan won't touch. The two products solve different financial problems.

What is the "first after" rule in critical illness policies?

The first after rule means your policy only covers conditions diagnosed after the policy is purchased. Pre-existing conditions diagnosed before enrollment are excluded, which is why applying while healthy is strongly recommended.