Life insurance funds charitable bequests by delivering a tax-free death benefit directly to a named charity, bypassing probate and often providing a gift far larger than the total premiums paid. This mechanism, formally called a charitable life insurance bequest, gives families a way to honor philanthropic values without reducing the assets they leave to heirs. The strategy works through beneficiary designations, policy ownership transfers, or advanced trust structures. Premier72 works with families and business owners who want to build a legacy that serves both their loved ones and the causes they care about most.

Why life insurance funds charitable bequests better than a will

A will-based charitable gift moves through probate. That process takes months, sometimes years, and reduces the final amount through court fees and administrative costs. Life insurance bypasses that process entirely.

Beneficiary designations override wills, meaning a charity named on a life insurance policy receives the death benefit directly once the claim is processed. No court involvement. No waiting. The charity gets the full amount, on time, without legal friction.

Permanent life insurance policies can pay out death benefits several times higher than the total premiums paid. That amplification is the core reason families choose this approach. A donor who can afford $300 per month in premiums may ultimately deliver a $500,000 gift to a cause they believe in. No other giving vehicle produces that kind of leverage at a predictable cost.

Life insurance proceeds paid to a charity are also fully deductible for estate tax purposes. That deduction can reduce or eliminate estate taxes for heirs, which means the charitable gift does not come at the family's expense. Both goals, giving generously and protecting heirs, can be achieved at the same time.

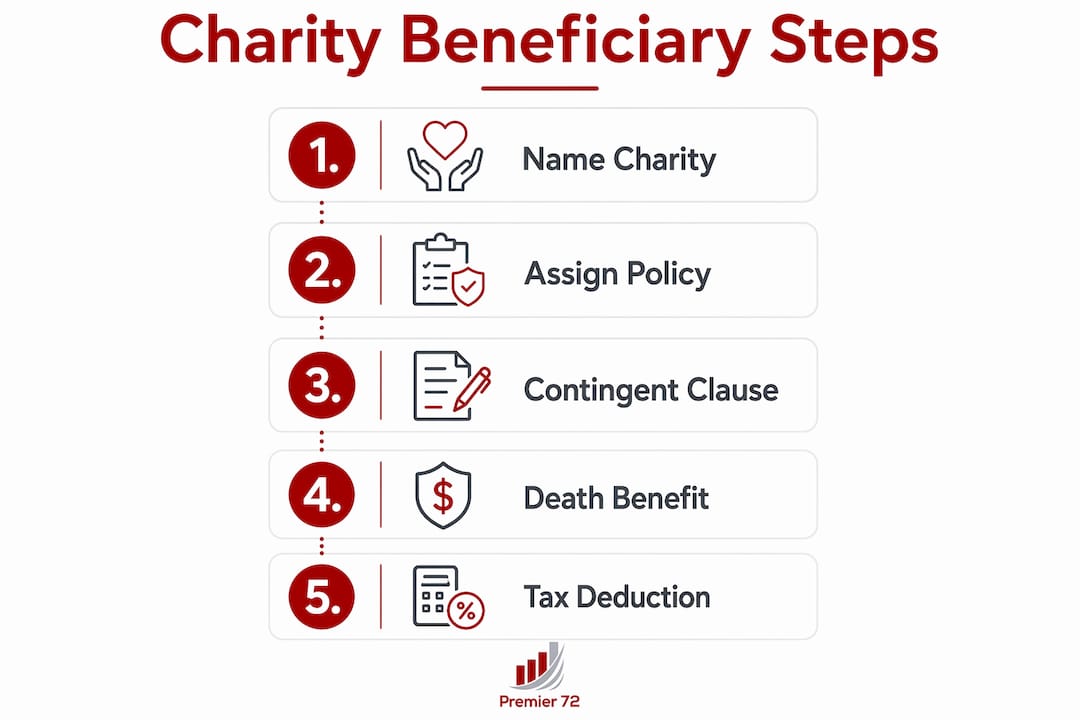

How naming a charity as beneficiary works

Naming a charity as a life insurance beneficiary is the simplest method available. You contact your insurance company, request a beneficiary change form, and list the charity by its legal name and tax ID number. No attorney required. No court approval needed.

The advantages are clear:

- Probate bypass. The death benefit goes directly to the named charity once the claim is filed, avoiding administrative delays that slow will-based gifts.

- Flexibility. You can name a charity as a partial beneficiary, splitting the death benefit between family members and one or more organizations.

- Revocability. Unlike some irrevocable trust structures, a standard beneficiary designation can be changed at any time while you are alive.

- Estate tax deduction. The full amount paid to the charity is removed from your taxable estate, which lowers the estate tax burden on everything else you leave behind.

- Policy type options. Term life, whole life, and universal life policies all support charitable beneficiary designations.

Pro Tip: Name the charity as a contingent beneficiary if you want the death benefit to go to family first. If all primary beneficiaries predecease you, the charity receives the full amount. This costs nothing and adds a meaningful safety net for your philanthropic goals.

How to donate an existing life insurance policy to charity

Donating an existing policy is a more advanced move, but it carries significant tax advantages. When you transfer ownership of a policy to a qualified charity, the charity becomes the new owner and eventual beneficiary. You give up control of the policy in exchange for a tax deduction.

The tax math works like this:

- Claim an income tax deduction. When you donate a policy, you may claim an itemized deduction based on the policy's fair market value or your adjusted cost basis, whichever is lower. The IRS determines fair market value using the policy's interpolated terminal reserve value.

- Avoid income tax on cash value. If you surrendered the policy for its cash value instead of donating it, you would owe ordinary income tax on any gain above your cost basis. Donating the policy avoids that tax entirely.

- Remove the death benefit from your estate. Once the charity owns the policy, the death benefit is no longer part of your taxable estate. That removal can produce meaningful estate tax savings for large estates.

- Continue paying premiums for additional deductions. If you keep paying premiums after the transfer, each premium payment may qualify as an additional charitable deduction.

Pro Tip: Watch the three-year rule. Transfers made within three years of death can pull the policy's value back into your taxable estate under IRS rules. Make irrevocable transfers well before you need them to count.

The most common mistake families make is waiting too long. A policy donated at age 75 with a serious health condition may not clear the three-year window. The time to act is when you are healthy and the transfer is clearly not imminent.

Advanced strategies: charitable trusts and legacy planning

Life insurance becomes a planning tool at a different level when combined with charitable remainder trusts (CRTs) and retirement asset strategies. These approaches suit families with larger estates, significant IRA balances, or both.

Using life insurance to replace an IRA left to charity

The SECURE Act and SECURE 2.0 changed the rules for inherited IRAs. Non-spouse heirs must now withdraw inherited IRA funds within 10 years. Every dollar they withdraw is taxed as ordinary income. For a $1,000,000 IRA, that tax burden can be substantial.

One solution is to leave the IRA directly to charity, which pays no income tax on the withdrawal, and use whole life insurance to replace that asset for heirs with an income-tax-free death benefit. The charity gets the full IRA value. The heirs get a death benefit equal to or greater than what they would have received after taxes. Everyone wins.

Charitable remainder trusts and life insurance

A CRT pays income to you or your heirs for a set period, then transfers the remaining assets to a named charity. Life insurance fits into this structure in two ways:

- Wealth replacement. Families sometimes use a portion of the CRT income stream to fund a life insurance policy inside an irrevocable life insurance trust (ILIT). The ILIT pays a death benefit to heirs, replacing the wealth that will eventually pass to charity.

- Testamentary funding. A life insurance policy can be structured to fund a CRT at death, providing the charity with a large, immediate asset base while generating income for surviving family members.

| Strategy | Primary benefit | Best suited for |

|---|---|---|

| Beneficiary designation | Probate bypass, simplicity | Most families |

| Policy ownership transfer | Income tax deduction, estate removal | Existing policy holders |

| IRA to charity plus life insurance | Offset inherited IRA tax burden | Large IRA owners |

| CRT with wealth replacement | Income stream plus charitable gift | High-net-worth estates |

Life insurance in wealth transfer works best when the strategy matches the family's actual financial picture, not a generic template.

What to consider before you commit to a plan

Choosing the right approach requires honest answers to a few practical questions. The wrong structure can create tax problems or leave heirs in a worse position than expected.

- Which policy type fits the goal? Term life works for a time-limited charitable commitment. Permanent policies (whole life or universal life) work better for long-term or irrevocable charitable strategies because they build cash value and do not expire.

- How will heirs be affected? Life insurance can ensure heirs receive an income-tax-free death benefit while the charity receives its gift. The key is sizing the policy correctly so neither goal is shortchanged.

- What are the valuation and filing requirements? Donated policies above certain thresholds require a qualified appraisal and IRS Form 8283. Skipping this step disqualifies the deduction.

- Is the charity a qualified 501(c)(3) organization? Only gifts to IRS-recognized charities qualify for estate and income tax deductions. Confirm the organization's status before structuring any transfer.

- Have you reviewed the policy recently? Many families check their life insurance policy infrequently, but beneficiary designations and ownership structures need periodic review as laws and family circumstances change.

The families who get this right treat it as a planning conversation, not a one-time transaction. A tax advisor, estate attorney, and financial advisor should all be involved before any irrevocable transfer is made.

Key Takeaways

Life insurance funds charitable bequests most effectively when the strategy is matched to the donor's estate size, tax situation, and family goals before any transfer is made.

| Point | Details |

|---|---|

| Probate bypass is automatic | Naming a charity as beneficiary sends the death benefit directly, skipping court delays entirely. |

| Amplified giving capacity | Permanent policies can deliver death benefits far exceeding total premiums paid, multiplying philanthropic impact. |

| Estate tax deduction applies | Life insurance proceeds paid to a charity are fully deductible, reducing the taxable estate for heirs. |

| Three-year rule is a real risk | Policy transfers made within three years of death may be pulled back into the taxable estate under IRS rules. |

| IRA plus life insurance is underused | Leaving an IRA to charity and replacing it with a life insurance death benefit for heirs eliminates inherited income tax. |

The flexibility most families never use

Most people I work with think of life insurance as a protection tool. They bought it to replace income if they died young. By the time they reach their 50s or 60s, the original purpose has faded, and the policy just sits there.

What surprises families most is how much flexibility a paid-up or low-cost permanent policy actually holds. You can redirect it. You can donate it. You can name a cause you have supported for decades and make that cause the largest gift you have ever given, without writing a check.

The piece I find underappreciated is the heir protection angle. Families often assume that giving to charity means giving something away from their children. The IRA-to-charity-plus-life-insurance structure flips that assumption entirely. The charity gets a tax-free asset. The heirs get a tax-free death benefit. The family pays less in estate taxes. That is not a compromise. That is a better outcome than most families achieve without planning.

The mistake I see most often is delay. Families wait until a health event forces the conversation, and by then the three-year rule becomes a real constraint. The best time to structure a charitable life insurance strategy is when you are healthy, your estate picture is clear, and you have time to make irrevocable decisions without pressure.

Work with advisors who understand both the tax code and your family's actual goals. Generic estate planning templates do not account for the specific mix of assets, relationships, and charitable intentions that make your situation unique.

— Asa

How Premier72 helps you build a giving legacy

Charitable giving through life insurance is one of the most tax-efficient strategies available to families with established estates. Premier72 works with business owners, professionals, and families to design life insurance and legacy plans that serve both philanthropic goals and family financial security.

Premier72's advisors understand the intersection of estate planning, tax strategy, and life insurance structuring. Whether you are considering a simple beneficiary designation or a more advanced approach involving charitable trusts and retirement assets, Premier72 builds plans around your specific situation. Connect with the Premier72 legacy planning team to explore how a charitable life insurance strategy fits your estate and the causes you care about most.

FAQ

What is a charitable life insurance bequest?

A charitable life insurance bequest is a gift made to a nonprofit organization through a life insurance policy, either by naming the charity as a beneficiary or by transferring policy ownership to the charity.

Does a life insurance gift to charity avoid probate?

Yes. Beneficiary designations on life insurance policies override wills and bypass probate entirely, sending the death benefit directly to the named charity once the claim is processed.

Can I get a tax deduction for donating a life insurance policy?

Yes. Donating an existing policy to a qualified 501(c)(3) charity may qualify for an income tax deduction based on the policy's fair market value, and future premium payments may also be deductible.

What is the three-year rule for charitable policy transfers?

The IRS three-year rule states that if you transfer a life insurance policy to a charity within three years of your death, the policy's value may be included back in your taxable estate. Transfers should be made well in advance to avoid this outcome.

How does life insurance protect heirs when I give to charity?

Life insurance can replace assets directed to charity by providing heirs with an income-tax-free death benefit. This approach is especially effective when a taxable IRA is left to charity and a whole life policy is used to deliver equivalent value to family members without the income tax burden.