Life insurance is defined as the most reliable tax-efficient liquidity tool available to business owners planning a financial legacy. The role of life insurance in wealth transfer goes far beyond income replacement. For Baby Boomer business owners preparing to exit, retire, or pass a company to the next generation, life insurance funds estate taxes, settles business debts, equalizes inheritances among heirs, and prevents forced asset sales at the worst possible moment. With the federal estate tax exemption raised to $15 million under the One Big Beautiful Budget Act, planning has shifted toward state-level taxes, liquidity timing, and maximizing step-up in basis. Life insurance sits at the center of every effective strategy.

How does life insurance support business succession and liquidity?

The most urgent problem at the death of a business owner is cash. Estate taxes, outstanding debts, and buy-out obligations come due quickly. Heirs who inherit a business but lack liquid funds face a brutal choice: sell assets at distressed prices or lose the company entirely.

Life-insurance-funded buy-sell agreements solve this directly. The policy delivers the exact funds needed at death, allowing surviving partners or heirs to purchase the deceased owner's share at fair market value without liquidating equipment, real estate, or inventory. That means the business continues operating and the family receives full value for what was built over decades.

Life insurance delivers cash within weeks of death. Other assets, including real estate and business equity, can take months or years to liquidate. That speed difference is the entire argument for keeping life insurance at the core of any succession plan.

Coverage sizing matters as much as policy type. Financial planning guidance calls for 5–10 times annual income in coverage to cover taxes, debts, and succession costs adequately. A business owner generating $400,000 annually should carry between $2 million and $4 million in coverage at minimum, and that figure must be recalibrated as the business grows.

Key liquidity applications for life insurance in business succession include:

- Buy-sell funding: Provides the cash for partners or heirs to complete a business transfer at fair market value without selling assets

- Estate tax payment: Covers federal and state estate tax obligations so heirs keep the business intact

- Debt settlement: Pays off business loans or personal guarantees that would otherwise burden the estate

- Inheritance equalization: Delivers equivalent value to heirs who do not inherit the business directly

Pro Tip: Review your buy-sell agreement and life insurance coverage together every two to three years. Business valuations rise, and a policy that was adequate five years ago may leave your heirs significantly short today.

Which life insurance policy type best fits wealth transfer goals?

Not every policy serves the same purpose. Choosing the wrong type is one of the most common and costly mistakes business owners make when building a legacy plan.

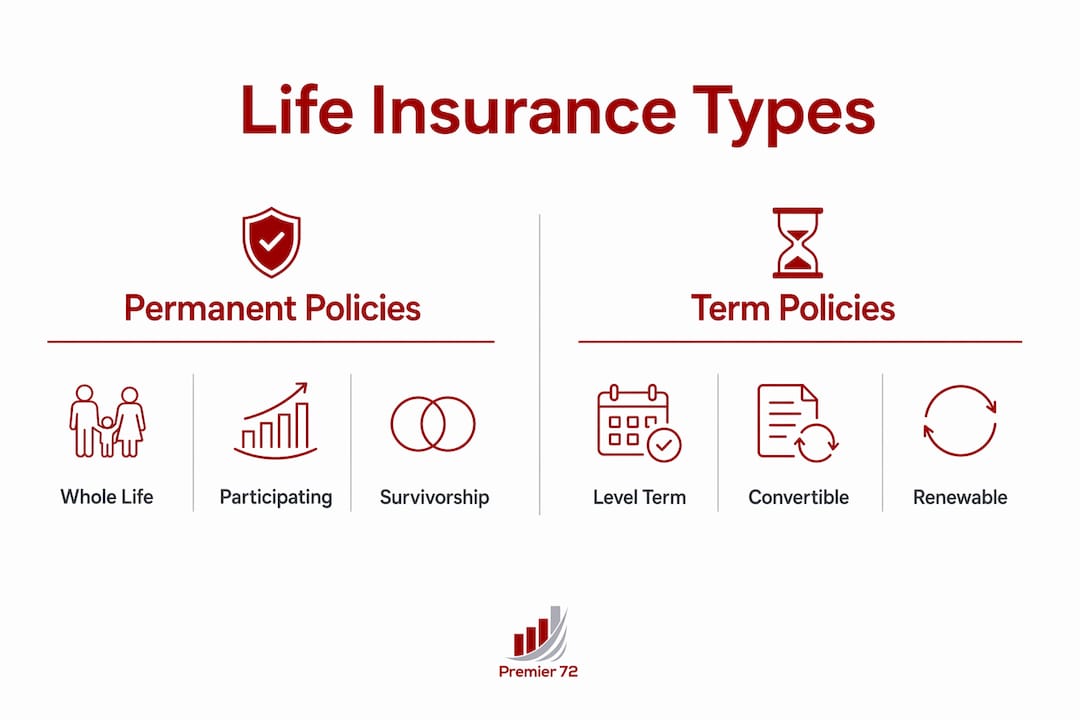

Here is how the main policy types compare:

| Policy Type | Cash Value | Premium Cost | Best Use Case |

|---|---|---|---|

| Whole Life / Participating Whole Life | Yes, grows tax-deferred | Higher | Long-term wealth transfer, retirement income supplement |

| Term Life | No | Lowest | Temporary coverage during high-debt or growth years |

| Survivorship (Second-to-Die) | No accessible cash value | Lower than individual | Estate tax liquidity at second death |

| Universal Life | Yes, flexible | Moderate | Flexible premium planning with permanent coverage |

Whole life and participating whole life are the workhorses of legacy planning. Participating whole life policies combine tax-deferred cash value accumulation, permanent coverage, and dividend potential. That combination makes them suitable as long-term wealth transfer vehicles, not just death benefit tools. The cash value also serves as a living asset you can borrow against during retirement.

Survivorship policies, also called second-to-die policies, insure two lives and pay out only after both insureds have died. Survivorship policies are cheaper than individual permanent policies, which makes them attractive for estate tax planning. The trade-off is significant: there is no accessible cash value during the couple's lifetimes, which limits flexibility if the business needs emergency liquidity.

Term insurance offers the lowest cost but no cash value and no permanent coverage. It works well during the years when debt is highest and the business is growing, but it is not a long-term legacy planning tool on its own.

The right sequence for most Baby Boomer business owners is to use a combination. A participating whole life policy builds permanent coverage and accessible cash value. A survivorship policy covers estate tax exposure at a lower premium. Term coverage fills any gap during the transition period before retirement.

- Assess your current business valuation and projected estate tax exposure

- Determine how much liquidity your heirs will need within 90 days of your death

- Match policy types to each liquidity need based on timing, cost, and access requirements

- Review the full portfolio annually with your insurance advisor and estate attorney

How do ilits and legal structures maximize tax efficiency?

Owning a life insurance policy in your own name is a common mistake with serious tax consequences. If policies are owned personally rather than through a properly structured legal entity, the death benefit is included in your taxable estate. That can trigger estate taxes on proceeds that were intended to pay those very same taxes.

An Irrevocable Life Insurance Trust, known as an ILIT, solves this problem. The ILIT owns the policy, not you. Because you no longer own the policy, the death benefit falls outside your taxable estate entirely. The trust then distributes proceeds to beneficiaries according to your instructions, free of estate tax.

ILIT ownership is critical to the tax efficiency of any life insurance strategy. Without it, the death benefit defeats its own purpose by increasing the taxable estate it was meant to protect.

Key structural considerations for tax-efficient wealth transfer using life insurance:

- ILIT ownership: The trust owns the policy and removes the death benefit from your taxable estate

- Crummey provisions: Annual gift tax exclusions fund ILIT premiums without triggering gift tax liability

- Trustee selection: An independent trustee avoids IRS challenges to the trust's validity

- Coordination with your will and other trusts: The ILIT must align with your broader estate documents to avoid conflicts or unintended distributions

Pro Tip: Set up the ILIT before purchasing the policy. Transferring an existing policy into an ILIT triggers a three-year lookback rule. If you die within three years of the transfer, the IRS pulls the death benefit back into your taxable estate.

Coordinating life insurance with legal structures like ILITs and timing policy funding correctly is the difference between a plan that works and one that erodes wealth at the exact moment it should be protecting it. This is not a task for a single advisor. It requires your estate attorney, CPA, and insurance advisor working from the same plan.

What pitfalls do baby boomer business owners face in legacy planning?

The biggest misconception among business owners is treating life insurance as income replacement rather than a strategic asset aligned with tax and succession goals. That framing leads to underinsurance, wrong policy types, and plans that collapse under real-world conditions.

Here are the most common pitfalls and how to avoid them:

- Static coverage in a growing business: Business valuations rise every year. A policy sized to your business value in 2018 may cover less than half of your current estate exposure. Recalibrate coverage regularly to keep pace with rising valuations.

- Survivorship policy trade-offs: Survivorship policies are cost-effective for estate tax planning, but they offer no cash value during the insureds' lifetimes. Do not rely on them as your only liquidity source.

- Treating life insurance as a set-and-forget asset: Life insurance must be integrated with buy-sell agreements and broader estate planning to function correctly. Policies that sit in isolation rarely deliver their intended outcome.

- Ignoring inheritance equalization: When one heir inherits the business and others do not, resentment and legal disputes follow. Life insurance equalizes inheritances by providing equivalent cash value to heirs who receive no business interest.

- Siloed advisors: Tax, legal, and insurance planning must be coordinated. A policy that is perfectly structured from an insurance standpoint can still fail if it conflicts with your estate documents or triggers unintended tax consequences.

The life insurance retirement income strategy for business owners works only when the policy is part of a coordinated plan. Standalone policies, mismatched coverage amounts, and outdated beneficiary designations are the most common reasons legacy plans fail to deliver.

Key takeaways

Life insurance is the most effective wealth transfer tool for business owners because it delivers tax-free liquidity faster than any other asset class, funds buy-sell agreements, and equalizes inheritances when structured correctly.

| Point | Details |

|---|---|

| Speed of liquidity | Life insurance pays within weeks of death, faster than any other estate asset. |

| Coverage sizing | Carry 5–10 times annual income to cover taxes, debts, and succession costs. |

| ILIT ownership | Own policies through an ILIT to keep death benefits out of your taxable estate. |

| Policy type selection | Match whole life, survivorship, and term policies to specific liquidity needs and timelines. |

| Regular recalibration | Review coverage every two to three years as business valuations rise. |

Why life insurance is the cornerstone most owners overlook

I have worked with enough Baby Boomer business owners to know that the conversation about life insurance almost always starts too late and too narrow. The owner sees a policy as a bill, not a balance sheet asset. That framing costs families real money.

The cleanest insight I can offer is this: when timing matters most, which is the first 90 days after a death, life insurance is the only asset that shows up on schedule. Real estate takes months to sell. Business equity takes longer. The IRS does not wait. Life insurance does not either, and that is exactly the point.

What I find most underused is the inheritance equalization function. A business owner with three children who leaves the company to one child and "something equivalent" to the others is setting up a family conflict. Cash from a well-sized policy, paid directly to the other two children through a properly structured trust, eliminates that dispute before it starts. I have seen families torn apart by exactly this scenario, and I have seen others navigate it cleanly because someone planned ahead.

The other thing I push hard on is the ILIT conversation. Most owners hear "irrevocable trust" and assume it means losing control. What it actually means is keeping the IRS out of your death benefit. That is a trade worth making every time.

Review your policy, your buy-sell agreement, and your estate documents together. Not separately. Not with three different advisors who never talk to each other. Together, with one coordinated plan.

— Asa

How Premier72 helps you build a legacy that lasts

Premier72 works directly with Baby Boomer business owners who are preparing for retirement, succession, or exit and need a plan that protects what they have built.

Through business continuity and legacy planning, Premier72 integrates life insurance strategy with buy-sell funding, estate planning coordination, and retirement income design. The goal is to maximize the after-tax wealth your heirs receive while keeping your business intact through the transition. Premier72 does not sell policies in isolation. Every recommendation connects to your broader succession and retirement plan. If your current coverage has not been reviewed against your current business valuation, that conversation needs to happen now. Explore Premier72's legacy planning approach and take the first step toward a plan your family can count on.

FAQ

What is the primary role of life insurance in wealth transfer?

Life insurance provides immediate, tax-free liquidity to heirs at death, funding estate taxes, settling debts, and enabling business succession without forced asset sales. It is the fastest and most reliable source of cash in any estate plan.

How does an ILIT protect life insurance proceeds from estate taxes?

An Irrevocable Life Insurance Trust owns the policy instead of the insured, removing the death benefit from the taxable estate entirely. Without ILIT ownership, the IRS includes the death benefit in the estate, which can trigger significant tax liability.

What type of life insurance is best for business succession planning?

Participating whole life insurance is the strongest long-term tool because it builds tax-deferred cash value and provides permanent coverage. Survivorship policies work well for estate tax liquidity at lower cost but offer no accessible cash value during the owners' lifetimes.

How much life insurance coverage does a business owner need?

Financial planning guidance recommends coverage equal to 5–10 times annual income to cover estate taxes, business debts, and succession costs. That figure should be reviewed every two to three years as the business grows in value.

Can life insurance prevent family disputes over inheritance?

Yes. Life insurance proceeds can be directed to heirs who do not inherit the business, providing equivalent value and eliminating the resentment that arises from unequal distributions of illiquid assets like real estate or business equity.