If you've heard that indexed universal life insurance puts your money directly into the stock market, you've heard wrong. What is indexed universal life insurance, really? It's a permanent life insurance contract that links your cash value growth to a market index, like the S&P 500, without ever buying a single share of stock. The policy gives you lifelong coverage, a tax-deferred savings component, and protection against market losses. For Baby Boomer business owners and retirees thinking seriously about retirement income and legacy planning, understanding exactly how this product works, and where it falls short, is worth your time.

Table of Contents

- Key takeaways

- What is indexed universal life insurance and how it works

- Benefits and drawbacks for Baby Boomers

- The indexed universal life policy setup process

- Practical strategies for retirement income and legacy planning

- My perspective on IUL and what most people get wrong

- How Premier72 can help you plan with confidence

- FAQ

Key takeaways

| Point | Details |

|---|---|

| Market-linked, not market-invested | IUL credits interest based on index performance but never directly invests in stocks. |

| Downside protection has limits | The 0% floor stops negative crediting, but policy fees still reduce cash value in flat years. |

| Caps and participation rates matter | These two parameters, not just the cap rate, determine what you actually earn each year. |

| Active management is non-negotiable | Rising insurance costs with age require ongoing policy reviews to avoid lapse. |

| Tax-advantaged income potential | Policy loans can provide tax-free retirement income when the policy stays properly funded. |

What is indexed universal life insurance and how it works

Indexed universal life insurance (IUL) is a form of permanent life insurance with two core components: a death benefit that lasts your entire life, and a cash value account that grows based on the performance of a market index. The industry-standard term is "indexed universal life," and you'll see it abbreviated as IUL throughout financial planning circles. As a permanent life insurance product, it does not expire like a term policy. You pay premiums, a portion covers insurance costs, and the rest builds cash value.

Here is what makes IUL fundamentally different from investing in an index fund: your cash value is never actually placed into the market. Instead, the insurance company credits your account with interest calculated by a formula tied to index movements. This distinction matters enormously. You don't capture dividends, and you don't own any underlying securities. Indexed growth differs from direct market returns, meaning the S&P 500 going up 22% in a year does not mean your policy earns 22%.

Three parameters govern what you actually receive:

- Floor: Typically set at 0%, this means your credited interest never goes negative, even when the index drops. Your cash value is protected from being reduced by market losses, though not from policy fees.

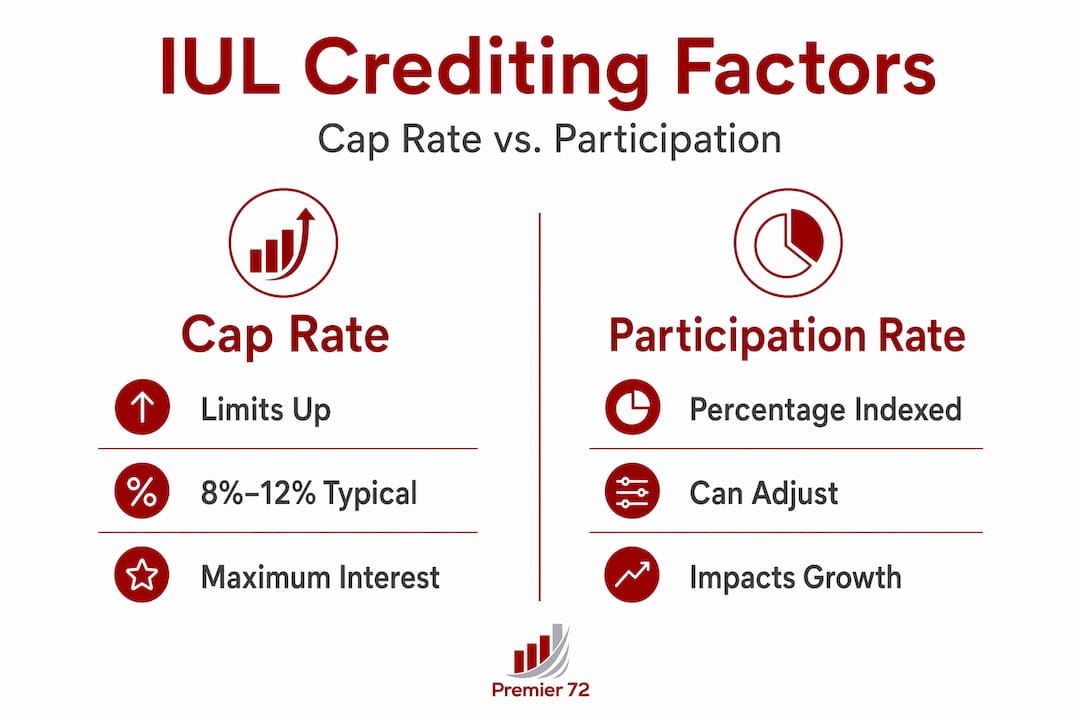

- Cap: The maximum credited interest rate in any period, typically ranging from 8% to 12%. If your cap is 10% and the index returns 18%, you receive 10%.

- Participation rate: The percentage of index gains that get credited to you. A 90% participation rate on a 10% index gain means you're credited 9%.

These three parameters interact. Focusing only on the cap rate is misleading because participation rates can be adjusted by the insurer over time, and the combination of all three determines your actual credited interest in any given year.

IUL also gives you flexibility most permanent policies don't. You can adjust your premium payments within limits, and you can often change your death benefit. Common crediting strategies include annual point-to-point (comparing the index at the start and end of a 12-month period), monthly averaging, and volatility-controlled indexes designed to smooth out return swings.

Pro Tip: Ask your advisor to run illustrations under three crediting scenarios, not just the current assumption. Seeing guaranteed, mid-range, and high-return projections side by side gives you a far more realistic picture of what to expect.

Benefits and drawbacks for Baby Boomers

IUL offers a real set of advantages for people in the 55-to-75 age range who are thinking about retirement income, business succession, and legacy planning. But it also carries drawbacks that don't get nearly enough attention in sales conversations.

The genuine benefits

IUL as a retirement asset works because it combines several features in one product that you'd otherwise have to assemble separately:

- Lifelong coverage with no expiration date, regardless of future health changes

- Tax-deferred cash value accumulation that doesn't generate a 1099 each year

- The 0% floor, which means a bad market year doesn't directly wipe out your credited interest

- Premium flexibility, so you can pay more in strong income years and reduce payments later

- Access to cash value through policy loans, which can serve as a supplemental income stream in retirement

The drawbacks you need to know

The 0% floor does not protect cash value from policy fees. This is one of the most misunderstood aspects of IUL. In a year when the index returns 0% or less, you receive 0% credited interest, but the insurance company still deducts its cost of insurance charges and administrative fees. Your cash value can, and often will, decline in flat or down years.

Caps and participation rates also limit how much of a bull market you actually capture. In the years when equity markets deliver their biggest gains, your IUL policy's credited interest is capped well below those gains.

Here's a direct comparison of the three main permanent life insurance options:

| Feature | IUL | Whole life | Variable universal life |

|---|---|---|---|

| Cash value growth | Index-linked (capped/floored) | Guaranteed + dividends | Direct market investment |

| Downside protection | 0% floor on crediting | Guaranteed minimum | No floor, full market risk |

| Growth potential | Moderate (capped) | Lower but predictable | Higher but volatile |

| Premium flexibility | Yes | Limited | Yes |

| Complexity | High | Moderate | Very high |

IUL sits in the middle. It's more growth-oriented than whole life but less risky than variable universal life. The catch is the complexity. Sales illustrations can be misleading when treated as investment projections, and regulators have taken notice. The NAIC has signaled increasing scrutiny around illustration practices to reduce consumer confusion about non-guaranteed assumptions.

Pro Tip: If a policy illustration only shows one scenario, treat that as a red flag. Request a guaranteed scenario and a mid-level assumption scenario before signing anything.

The indexed universal life policy setup process

Understanding what you're getting into before you apply saves you weeks of frustration. Here's what to expect when setting up an IUL policy:

-

Application submission. You complete a formal application that includes health history, financial information, and your coverage and premium goals. This is also where you choose the insurer, the death benefit structure, and any riders you want.

-

Underwriting and medical review. The insurer orders your medical records and typically requires a paramedical exam, including lab work. Lab results generally take about 7 to 10 days to process, and the full underwriting decision usually arrives within 4 to 6 weeks. Accelerated underwriting exists but isn't guaranteed for every applicant.

-

Illustration review and approval. Before the policy issues, you'll receive a detailed illustration. This document projects future cash values and death benefits under different assumptions. Review guaranteed, current, and mid-level scenarios. The NAIC's push for greater illustration transparency reflects how easily these projections can be misread as promised outcomes.

-

Initial premium payment and policy activation. Once you accept the policy, your first premium payment triggers activation. The cash value begins accumulating after internal charges are deducted.

-

Ongoing policy management. This step never ends. Rising cost of insurance with age means the charges drawn from your cash value increase every year. Annual or biannual policy reviews with your advisor help catch underfunding problems before they become irreversible. Policies that looked healthy at age 60 can face serious sustainability questions by age 75 if premium funding hasn't kept pace.

Practical strategies for retirement income and legacy planning

Used correctly, an IUL policy can play a meaningful role in a diversified retirement plan. The key word is "correctly."

Tax-advantaged income from policy loans. When structured properly, policy loans can be tax-free as long as the policy stays in force. Unlike withdrawals from a traditional IRA or 401(k), these loans do not generate taxable income. For retirees already managing their tax bracket carefully, this can be a meaningful advantage. Be aware that unpaid loans reduce the death benefit dollar for dollar.

Filling the gaps beyond contribution limits. IUL has no IRS contribution limits the way a 401(k) or Roth IRA does. Business owners who have maxed out qualified retirement accounts and still want tax-advantaged accumulation can use a well-funded IUL policy to extend that strategy.

Legacy and estate planning. The death benefit passes to your beneficiaries income-tax-free. For business owners who want to leave a specific financial legacy or fund a buy-sell agreement, the death benefit offers certainty that market-based assets cannot.

- Avoid underfunding the policy in early years. Paying minimum premiums may feel comfortable now but creates serious risk of lapse when insurance costs climb in your late 60s and 70s.

- Do not build a retirement income strategy around optimistic illustration returns. Retirees using IUL for income must prioritize policy sustainability through later years, because the costs only go up.

- Review your policy after any major financial change: business sale, market downturn, significant health change, or shift in your income needs.

- Work with an advisor who reviews the policy annually, not someone who sells it and moves on.

Pro Tip: If you're planning to use IUL cash value as a retirement income source, model your withdrawal strategy assuming the policy earns its mid-level illustrated rate, not the current assumption rate. That single adjustment gives you a far more resilient income plan.

My perspective on IUL and what most people get wrong

I've worked with business owners and retirees at various stages of financial planning, and IUL is one of the most consistently misunderstood products I encounter. Not because it's bad. Because the gap between how it's sold and how it performs is wider than clients expect.

The fee impact during zero-crediting years is something I find most clients genuinely do not grasp until I put the numbers on paper. Policy fees don't pause when the index goes flat. In a year where your credited interest is 0%, the insurance company is still drawing cost of insurance charges from your cash value. In your 60s, those charges are meaningful. In your 70s, they're significant. By your 80s, they can be severe if the policy hasn't been managed actively.

What I also observe is a mismatch between the illustration a client received at purchase and what the policy is actually doing years later. Real-world performance often differs from initial projections, particularly in periods of low or moderate market returns. The clients who come out ahead are the ones who review their policy every year, adjust premium funding when needed, and have an advisor who tells them the truth about the numbers.

IUL, as part of a broader strategy that includes business exit planning, qualified retirement accounts, and tax diversification, can be genuinely valuable. My view is that it works best when you go in with eyes open: realistic return expectations, a commitment to funding it properly, and a plan for managing it over decades, not just buying it and forgetting it.

— Asa

How Premier72 can help you plan with confidence

Retirement income planning for business owners is rarely simple. You're balancing a business exit, an estate, tax exposure, and income needs that may span 30 or more years. That's exactly the complexity Premier72 works through with clients every day.

Premier72 specializes in helping Baby Boomer business owners and retirees evaluate insurance-based strategies, including indexed universal life policies, within the context of a complete financial and legacy plan. The team helps you understand which policies are worth considering, how to read an illustration honestly, and how an IUL fits alongside your other retirement assets. If you're ready to explore whether an IUL policy belongs in your plan, start at Premier72.com for personalized guidance from advisors who understand both the business side and the financial security side of your retirement picture.

FAQ

What is indexed universal life insurance in simple terms?

IUL is a permanent life insurance policy where your cash value earns interest linked to a market index, with a floor that prevents negative crediting and a cap that limits maximum gains. It is not a direct investment in the stock market.

How does the 0% floor actually protect me?

The floor prevents your credited interest from going negative, but it does not stop policy fees from reducing your cash value. In a flat or down market year, your cash value can still decline because insurance charges continue regardless of index performance.

What returns can I realistically expect from IUL?

Credited returns depend on the index performance, your cap rate (typically 8% to 12%), and your participation rate. Real-world returns often fall below the current-assumption rates shown in illustrations, so planning around mid-level scenarios is more prudent.

How long does it take to set up an IUL policy?

The full indexed universal life policy setup process, from application through underwriting and policy activation, typically takes 4 to 6 weeks, depending on how quickly medical records and lab results are processed.

Can I use my IUL policy for retirement income?

Yes. You can access cash value through policy loans, which are generally tax-free as long as the policy stays in force. However, policy sustainability requires careful funding throughout your life, particularly as insurance costs rise with age.