A life insurance retirement income strategy uses properly structured permanent life insurance to generate tax-advantaged supplemental income while preserving wealth for your heirs and business successors. For Baby Boomer business owners, this approach solves a problem that 401(k)s and IRAs cannot: it combines tax-free income access, legacy protection, and business continuity funding inside a single financial vehicle. The industry term for this structure is a Life Insurance Retirement Plan, or LIRP. Under IRS Section 7702, permanent policies grow cash value tax-deferred and allow policy loans that are generally not counted as taxable income. That combination makes a LIRP one of the most tax-efficient tools available to business owners who have already maxed out traditional retirement accounts.

Which life insurance policies work best for retirement income?

Not all life insurance builds usable retirement income. Choosing the correct policy type is the single most consequential decision in this strategy, because many policies carry high insurance costs that drain the cash value you need for income. The two permanent policy types that fit a retirement income strategy are whole life and indexed universal life (IUL). Term life insurance carries no cash value and is not suitable for income generation. You can read more about why term falls short for this purpose.

Whole life insurance

Whole life delivers predictable, guaranteed cash value growth funded by fixed premiums and annual dividends from mutual carriers like MassMutual, Guardian, and New York Life. The growth rate is modest compared to equity markets, but it is contractually guaranteed. For business owners who want certainty above all else, whole life functions as the fixed-income anchor of a retirement income plan.

Indexed universal life insurance

IUL links cash value growth to a market index such as the S&P 500, with a floor that prevents losses in down years. Carriers like North American, Nationwide, and Allianz offer IUL products with participation rates and caps that determine how much index gain you capture. This structure gives you market-linked upside with downside protection, which is particularly valuable for owners whose business income already carries significant market risk. Premier72 has a detailed breakdown of IUL for retirees worth reviewing before you choose.

| Policy type | Cash value growth | Risk profile | Best for |

|---|---|---|---|

| Whole life | Guaranteed + dividends | Very low | Predictability, legacy focus |

| Indexed universal life (IUL) | Index-linked with floor | Low to moderate | Growth potential, tax diversification |

| Term life | None | N/A | Pure death benefit only |

Pro Tip: Ask your advisor to run an illustration showing the internal rate of return on cash value at age 65, 70, and 75. That single comparison reveals whether the policy is designed for income or primarily for the insurance company's profit.

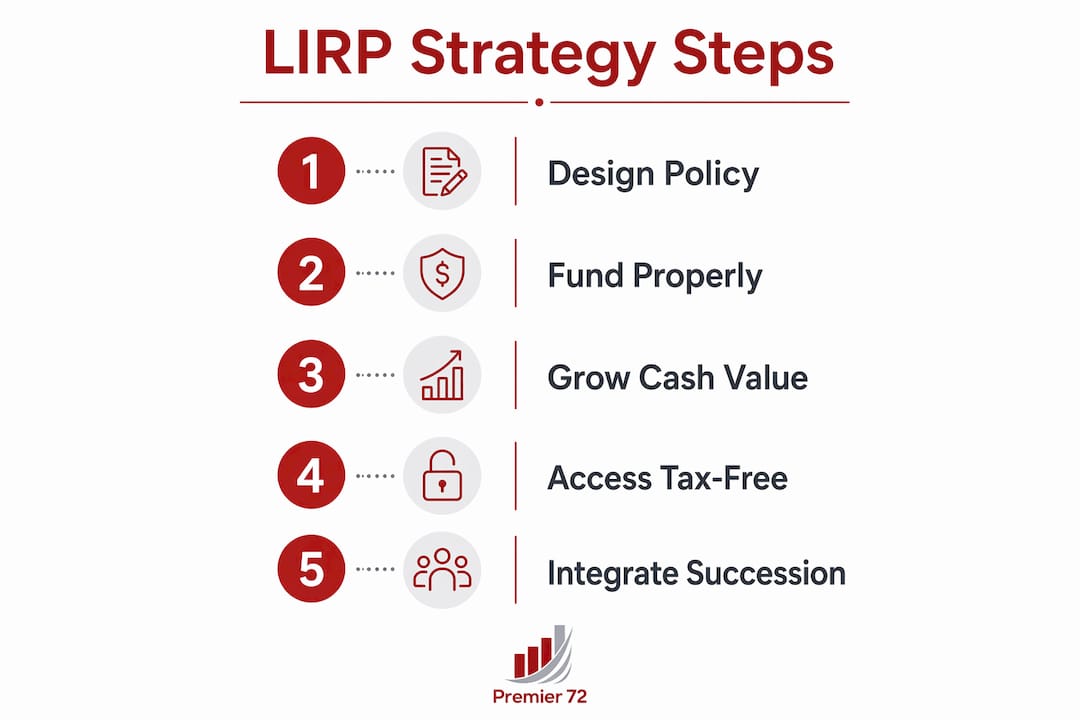

How to structure and fund a life insurance retirement income strategy effectively

Policy design determines whether your LIRP becomes a powerful income tool or an expensive disappointment. The IRS allows you to fund a permanent policy with premiums well above the base cost of insurance, and that overfunding is exactly what accelerates cash value growth. Policies must use the lowest possible insurance cost allowed under IRS code to maximize the cash available for retirement income. Every dollar that goes toward insurance cost is a dollar not compounding for you.

The critical compliance boundary is the Modified Endowment Contract, or MEC. If you fund a policy too aggressively relative to its death benefit in the first seven years, the IRS reclassifies it as a MEC and eliminates the tax-free loan advantage. Avoiding MEC status requires precise premium scheduling, which is why this is not a do-it-yourself project.

Here is a practical funding sequence to follow:

- Determine your income target. Work backward from the monthly income you want at retirement to calculate the required cash value at that date.

- Select the minimum death benefit. A lower death benefit relative to premium reduces insurance costs and maximizes cash value accumulation.

- Add a paid-up additions (PUA) rider. PUA riders let you pour additional premium directly into cash value with minimal insurance cost attached.

- Set a consistent funding schedule. Irregular or missed premiums slow cash value growth and can jeopardize policy performance projections.

- Review annually with your advisor. Policy performance, interest crediting, and your business income can all shift, requiring adjustments to keep the plan on track.

If you already hold an older, underperforming policy, a 1035 exchange lets you transfer its cash value to a better-designed policy without triggering a taxable event. This is one of the most underused tools in retirement income planning for business owners over 55.

Pro Tip: Have an independent advisor run a policy audit on any existing permanent life insurance you own. Many policies purchased in the 1990s and 2000s were designed for death benefit, not income, and a 1035 exchange can recover years of lost accumulation.

How to access cash value tax-free for retirement income

Cash value grows tax-deferred and can be accessed through two mechanisms: withdrawals and policy loans. Understanding the difference between them determines whether your income stays tax-free.

Withdrawals up to your cost basis (the total premiums you have paid) are tax-free. Once you exceed that basis, withdrawals become taxable. Policy loans, by contrast, are generally not taxable income regardless of the amount, as long as the policy remains in force. This distinction is why most LIRP income strategies sequence withdrawals first to exhaust the cost basis, then shift to policy loans for the remainder of retirement income.

Key points to manage carefully:

- Policy loans reduce your death benefit dollar for dollar until repaid.

- Outstanding loans trigger taxable income if the policy lapses, which is the most common and costly mistake in this strategy.

- Loan interest accrues against the policy; some IUL products offer wash loans where the credited interest offsets the loan interest, effectively making the loan cost-neutral.

- Policy loans do not count as taxable income, which means they do not affect Medicare surcharges or Social Security taxation thresholds. That is a material advantage over IRA distributions for owners with significant retirement income.

This tax-free income bucket gives you flexibility to manage your overall tax bracket in retirement, drawing from taxable accounts, Roth IRAs, and policy loans in a sequence that minimizes your total tax bill each year.

Common mistakes that undermine this strategy

Disciplined, professional planning is not optional in a LIRP. The tax advantages are real, but they depend on maintaining the policy correctly for decades. These are the mistakes that most frequently destroy the strategy:

- Triggering MEC status. Overfunding beyond IRS limits in the first seven years converts the policy to a MEC, eliminating tax-free loan access permanently.

- Stopping premium payments. Skipping premiums reduces cash value, can cause the policy to lapse, and may trigger a taxable event on any outstanding loans.

- Borrowing excessively without monitoring. Taking too much in policy loans without tracking the loan-to-cash-value ratio can push the policy toward lapse, especially in years when index crediting is low.

- Failing to coordinate with your broader plan. A LIRP works best as one component of a tax-diversified retirement plan that includes a 401(k), Roth IRA, and taxable accounts. Treating it as your only retirement vehicle creates dangerous concentration risk.

- Choosing the wrong advisor. Many insurance agents are trained to sell policies, not design income strategies. You need an advisor who understands both the insurance mechanics and your tax situation.

"The biggest risk in a life insurance retirement income strategy is not market loss. It is policy lapse caused by poor design or undisciplined management. A lapsed policy with outstanding loans creates a tax bill at exactly the moment you can least afford one."

Integrating this strategy with business succession and retirement planning

For business owners, a LIRP does not operate in isolation. It connects directly to your succession plan, your buy-sell agreement, and your overall retirement income plan. Life insurance is the most common funding vehicle for buy-sell agreements because it delivers a tax-free lump sum to surviving partners at precisely the moment the business needs liquidity. That same policy's cash value can serve as your personal retirement income while the business is still operating.

Annuities and life insurance serve complementary roles in a complete retirement plan. Annuities prioritize income longevity; life insurance prioritizes legacy and tax-free access. If your business sells and you no longer need the death benefit, a 1035 exchange can convert the policy's cash value into a guaranteed income annuity without a taxable event. That flexibility is unique to this asset class.

| Income source | Tax treatment | Legacy value | Business use |

|---|---|---|---|

| 401(k) / IRA | Taxable on withdrawal | Taxable to heirs | No direct business use |

| Roth IRA | Tax-free | Tax-free to heirs | No direct business use |

| Life insurance (LIRP) | Tax-free via loans | Income-tax-free death benefit | Buy-sell, key person funding |

| Annuity | Taxable (gains portion) | Reduced or none | No direct business use |

Private banking strategies used by high-net-worth clients often incorporate life insurance as a collateral asset, borrowing against cash value at favorable rates to fund business operations or acquisitions without liquidating the policy. This technique, sometimes called infinite banking, adds another layer of utility for owners who need capital flexibility before retirement.

Premier72's Retirement Bank Method™ is built around this exact integration: turning a business owner's financial assets, including life insurance, into a coordinated retirement and succession system. You can explore why life insurance qualifies as a retirement asset for owners in more depth on the Premier72 blog.

Key takeaways

A properly structured LIRP delivers tax-free retirement income, legacy protection, and business succession funding inside a single permanent life insurance policy, making it the most versatile financial tool available to Baby Boomer business owners.

| Point | Details |

|---|---|

| Policy type determines outcome | Whole life and IUL build cash value; term life does not and cannot generate retirement income. |

| MEC compliance is non-negotiable | Overfunding beyond IRS limits in year one through seven eliminates the tax-free loan advantage permanently. |

| Sequence withdrawals before loans | Draw from cost basis first, then switch to policy loans to keep all income tax-free throughout retirement. |

| Coordinate with succession planning | Life insurance funds buy-sell agreements and provides liquidity for estate taxes while simultaneously building your income base. |

| Professional oversight is required | Annual policy reviews with a qualified advisor prevent lapse, optimize loan management, and keep the strategy aligned with your tax situation. |

What I have learned from working with business owners on this strategy

Most business owners I work with come to this conversation having heard about LIRPs from a neighbor or a podcast, half-convinced it is either a miracle or a scam. The truth is more specific than either. A LIRP is a precision instrument. Used correctly, it solves real problems that no other financial vehicle addresses as cleanly: tax-free income that does not trigger Medicare surcharges, a death benefit that transfers wealth income-tax-free, and a funding vehicle for your buy-sell agreement that doubles as your personal retirement account.

What I have seen go wrong is almost always a design problem, not a concept problem. Policies sold with high death benefits and low premiums look affordable but build almost no cash value. Owners who buy those policies and expect retirement income in 20 years are going to be disappointed. The policy has to be engineered from day one for accumulation, not just protection.

The other pattern I see is owners who treat this as a set-and-forget decision. They fund the policy for three years, business gets busy, premiums get skipped, and the policy underperforms or lapses. A LIRP requires the same discipline you apply to your business: consistent investment, regular review, and professional accountability. When those conditions are met, I have seen owners generate $8,000 to $15,000 per month in tax-free income from policies they started funding in their late 40s. That is not a sales pitch. That is what the math produces when the strategy is executed correctly.

My honest recommendation: do not evaluate this strategy based on a single illustration from a single carrier. Get a second opinion, compare policy designs, and make sure your tax advisor is in the room when you make the decision.

— Asa

How Premier72 helps you build this strategy the right way

Premier72 works with Baby Boomer business owners to design life insurance retirement income strategies that connect directly to their succession plans, tax situations, and income goals. This is not off-the-shelf insurance sales. Premier72 coordinates with your CPA and attorney to make sure the policy design, funding schedule, and loan strategy are aligned with your broader financial picture from day one.

If you are a business owner within 10 years of retirement and you have not yet built a tax-free income bucket, the window to fund one effectively is narrowing. The earlier a LIRP is funded, the more cash value it builds. Premier72 offers a comprehensive review of your current insurance holdings and retirement income plan. Visit Premier72 to schedule a consultation and find out exactly what a properly designed strategy could generate for you.

FAQ

What is a life insurance retirement income strategy?

A life insurance retirement income strategy, formally called a Life Insurance Retirement Plan (LIRP), uses a permanent life insurance policy structured under IRS Section 7702 to build tax-deferred cash value that can be accessed as tax-free income in retirement through policy loans and withdrawals up to cost basis.

Which policy type is best for retirement income?

Indexed universal life (IUL) and whole life insurance are the two policy types suited for retirement income strategies. Term life insurance builds no cash value and cannot generate retirement income.

Are policy loans really tax-free?

Policy loans are generally not taxable income as long as the policy remains in force. If the policy lapses with outstanding loans, the loan balance becomes taxable income in the year of lapse.

Can I use existing life insurance for this strategy?

Yes. A 1035 exchange allows you to transfer cash value from an existing policy to a better-designed policy or an annuity without triggering a taxable event, making it possible to reposition underperforming policies.

How does this strategy fit with my business succession plan?

The same permanent life insurance policy that builds your retirement income can fund a buy-sell agreement, provide key person coverage, and deliver a tax-free death benefit to your heirs or business partners. That dual function makes it uniquely suited to business owners who need both personal income and business continuity protection in a single structure.