Annuities are defined as insurance contracts that provide tax-deferred growth, direct beneficiary transfers, and flexible income streams, making them one of the most practical tools in legacy planning for business owners. The role of annuities in legacy planning goes beyond simple retirement income. For Baby Boomer business owners with estates approaching the 2026 federal exemption of $13.99 million, annuities offer a structured way to move wealth to heirs while reducing probate exposure and managing tax liability. This guide covers the core mechanics, compares annuity types, addresses trust ownership rules, and gives you a practical framework for integrating annuities into a broader estate strategy.

What is the role of annuities in legacy planning?

Annuities serve three core functions in a legacy plan: tax-deferred accumulation, probate avoidance through beneficiary designations, and guaranteed income that can be structured to protect heirs. Each function addresses a specific gap that brokerage accounts, real estate, and business equity alone cannot fill.

Tax-deferred growth vs. taxable accounts

A taxable brokerage account generates capital gains and dividend income every year, whether you need the cash or not. An annuity defers all gains until withdrawal. That deferral compounds over time, leaving more capital inside the contract to pass to heirs or fund income riders.

The trade-off is real, though. Annuities bypass probate via direct beneficiary designations, but they do not receive a stepped-up cost basis at death. Heirs pay ordinary income tax on every dollar of deferred gain. That tax rate is typically higher than the capital gains rate your estate would face on appreciated stock. Understanding this distinction before you buy is not optional. It is the difference between a smart legacy tool and an expensive surprise for your children.

Probate avoidance and beneficiary designations

Probate avoidance is one of the clearest benefits of annuities for estate planning. The contract passes directly to named beneficiaries outside the probate process, which saves time, legal fees, and public disclosure of your estate details.

That efficiency only works if your designations are current. An outdated beneficiary form can send assets to an ex-spouse, a deceased sibling, or your estate itself, which triggers probate anyway. Periodic review of beneficiary designations is the single most overlooked step in annuity-based legacy planning.

Pro Tip: Review every annuity beneficiary designation after a major life event: marriage, divorce, death of a named beneficiary, or a change in your estate plan. Set a calendar reminder to do a full review every two years regardless.

How do different annuity types compare for legacy goals?

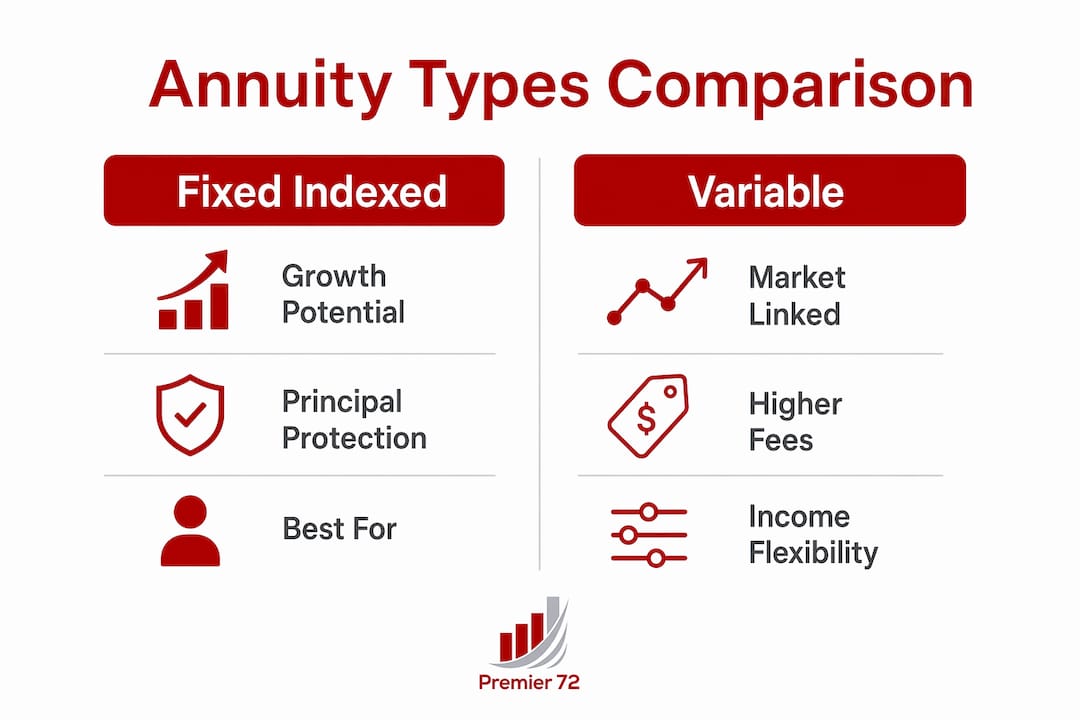

Not every annuity serves legacy planning equally. The structure you choose determines how much growth reaches your heirs, how much risk they absorb, and how much flexibility you retain.

| Annuity Type | Growth Potential | Principal Protection | Legacy Feature | Best For |

|---|---|---|---|---|

| Fixed Indexed (FIA) | Moderate, market-linked | Yes | ROP rider available | Balanced growth and protection |

| Variable | Higher, market-dependent | No (without rider) | Enhanced death benefit riders | Growth-focused, risk-tolerant owners |

| Private Annuity | Negotiated rate | Depends on structure | Estate tax removal | Transferring appreciated business assets |

| Fixed | Low, guaranteed rate | Yes | Predictable inheritance amount | Conservative legacy preservation |

Fixed indexed annuities offer principal protection with market-linked growth and lower fees than variable products. That combination makes them the most commonly used annuity in high-net-worth legacy strategies in 2026. Variable annuities can now be structured with enhanced death benefits that help heirs manage downside market risk when coordinated with an estate plan.

Private annuities for business owners

A private annuity is a contract between you and a family member or trust, not an insurance company. You transfer an appreciated asset, such as business equity or commercial real estate, in exchange for lifetime income payments. The asset leaves your taxable estate immediately. A private annuity sale allows a business owner to remove appreciated assets from the taxable estate under the 2026 federal exemption of $13.99 million, which is a critical planning window before potential exemption reductions after 2025 sunset provisions.

Return of Purchase Price features

The Return of Purchase Price (ROP) feature guarantees that if you die before receiving your full principal back in income payments, the remaining balance goes to your heirs. ROP features return the original investment on the owner's death but slightly reduce monthly payouts. That trade-off is worth evaluating carefully. If your primary goal is maximizing income, ROP costs you. If your primary goal is protecting principal for heirs, ROP delivers.

Pro Tip: Many business owners confuse an annuity's cash surrender value with the benefit base used for income rider calculations. The benefit base is often higher and determines your income guarantee. Always ask your advisor to show you both numbers before signing.

What are the tax and trust rules for annuities in estate plans?

Placing an annuity inside a trust is a common estate planning move, but the tax rules are strict and counterintuitive. Getting this wrong eliminates the tax deferral that makes annuities valuable in the first place.

IRS Section 72(u) is the governing rule. It states that when a non-natural person, such as a corporation or irrevocable trust, owns an annuity, the contract loses its tax-deferred status. Non-natural person ownership triggers annual taxation on all gains inside the contract. That annual tax bill can significantly erode the legacy value of the annuity over a 10 or 20 year holding period.

The solution most estate attorneys use is the grantor trust. A grantor trust is treated as the owner's alter ego for income tax purposes. Grantor trust ownership allows continuation of annuity tax deferral because the IRS still considers the grantor a natural person for this purpose. The asset can sit inside the trust structure for estate planning purposes while retaining its tax-deferred growth.

Key distinctions to know before placing an annuity in any trust:

- Revocable living trusts generally preserve tax deferral because the grantor retains control and is treated as the owner.

- Irrevocable trusts remove the asset from your taxable estate, which helps with estate tax. They also trigger Section 72(u) unless structured as a grantor trust.

- Charitable remainder trusts (CRTs) can hold annuities but require careful coordination to avoid accelerating income recognition.

- Irrevocable life insurance trusts (ILITs) are not typically used to hold annuities but are frequently paired with them in legacy plans.

The trade-off with irrevocable trusts is real. You lose tax deferral under Section 72(u), but you remove the asset from your taxable estate. For business owners with estates above $10 million, that estate tax savings can outweigh the annual income tax cost. Run the numbers with a CPA and an estate attorney before making this decision.

How do you balance income needs and legacy goals with annuities?

The biggest mistake Baby Boomer business owners make with annuities is over-annuitizing. Excessive annuitization limits legacy asset size and reduces your options for funding trusts, charitable gifts, or business succession costs. Once you annuitize a contract, that capital is locked into an income stream. You cannot redirect it to a trust, a grandchild's education fund, or a buy-sell agreement if your circumstances change.

Over-annuitization traps capital in inflexible income streams and reduces your ability to fund trusts or charitable legacy goals. The fix is partial annuitization. Annuitize enough to cover your fixed living expenses. Keep the rest in fixed indexed annuities or other vehicles that retain liquidity and legacy value.

Steps to avoid the most common annuity pitfalls in legacy planning:

- Calculate your income floor first. Add up Social Security, pension income, and any other guaranteed sources. Only annuitize the gap between that floor and your actual spending needs.

- Keep at least 30–40% of retirement assets outside annuities. That pool funds trusts, gifts, and unexpected costs without triggering surrender charges.

- Add a long-term care rider if you qualify. Long-term care costs surged 22%–50% since 2019, and a single nursing home stay can consume assets you planned to leave to heirs. An LTC rider on an annuity protects the legacy pool without requiring a separate policy. Learn more about long-term care planning options before your health situation changes.

- Review fees on variable annuities annually. Mortality and expense charges, sub-account fees, and rider costs can total 2%–3.5% per year, which compounds against your heirs over time.

- Coordinate annuity income timing with your estate plan. Distributions from inherited annuities are taxable. Structuring payouts to minimize your heirs' tax bracket exposure is a planning opportunity most families miss.

Pro Tip: Pair an annuity with a life insurance policy inside an ILIT. The annuity provides your income. The life insurance replaces the estate value lost to income taxes on inherited annuity gains. This combination is one of the most tax-efficient legacy structures available to business owners.

Practical steps to incorporate annuities into your legacy plan

Integrating annuities into a legacy plan is not a one-time transaction. It requires coordination across your estate documents, beneficiary forms, tax strategy, and business succession plan.

- Assess your estate size relative to the 2026 exemption. The federal estate tax exemption is $13.99 million per individual. If your combined estate, including business equity, real estate, and retirement accounts, approaches that threshold, annuity-based strategies like private annuity sales become urgent, not optional.

- Align beneficiary designations with your will and trust documents. A beneficiary designation overrides your will. If your will leaves everything to a trust but your annuity names your children directly, the trust never receives those assets. An estate planning attorney can audit your designations and close that gap.

- Integrate annuities with life insurance for tax efficiency. A life insurance retirement income strategy can offset the ordinary income tax your heirs will owe on inherited annuity gains. This pairing is especially effective for business owners with large deferred gain balances.

- Review your plan annually through 2026 and beyond. Federal tax law is in flux. The 2017 Tax Cuts and Jobs Act provisions are set to sunset, which could cut the estate tax exemption roughly in half. Any annuity-based legacy strategy built around today's exemption needs a contingency plan.

- Work with a team, not a single advisor. Annuity-based legacy planning touches insurance, tax law, estate law, and business valuation. A financial advisor, CPA, and estate attorney working from the same plan produce better outcomes than any one of them working alone. Explore annuity types for retirement income to understand your product options before those conversations.

Key takeaways

Annuities protect and transfer wealth most effectively when they are integrated with trusts, life insurance, and a current beneficiary designation strategy rather than used as a standalone income tool.

| Point | Details |

|---|---|

| Tax deferral has limits | Heirs pay ordinary income tax on inherited annuity gains with no stepped-up basis. |

| Grantor trusts preserve deferral | Use a grantor trust structure to keep annuity tax deferral intact inside an estate plan. |

| Partial annuitization protects flexibility | Annuitize only your income gap to keep assets available for trusts and legacy gifts. |

| ROP features protect principal | Return of Purchase Price riders preserve original investment for heirs at the cost of slightly lower income. |

| Beneficiary reviews are non-negotiable | Outdated designations can send annuity assets to unintended heirs or directly into probate. |

Why I think most business owners underuse annuities as legacy tools

Most of the business owners I work with think of annuities as income products. They buy them to replace a paycheck in retirement, and they stop there. That framing leaves a significant amount of legacy value on the table.

The most underused application I see is the private annuity sale for transferring appreciated business equity. A business owner with $3 million in appreciated real estate or company stock can transfer that asset to a family trust, receive lifetime income, and remove the entire value from the taxable estate. That is a legitimate estate tax strategy that most owners never hear about until it is too late to act before exemption changes.

The other thing I push back on is the idea that annuities and life insurance compete with each other. They do not. They solve different problems. The annuity funds your income. The life insurance replaces the estate value your heirs lose to income taxes on inherited gains. Used together, they are more powerful than either product alone.

My honest advice: do not let complexity be the reason you avoid this conversation. The rules around Section 72(u), grantor trusts, and ROP features sound technical, but the underlying logic is straightforward. Get the right advisors in the room, map your estate against the 2026 exemption, and build a plan that uses annuities for what they are genuinely good at.

— Asa

How Premier72 helps business owners build legacy-ready annuity strategies

If you have spent decades building a business, your legacy plan needs to reflect that complexity. A generic annuity purchase does not account for your business equity, your estate tax exposure, or the income tax your heirs will face on inherited gains.

Premier72 works directly with Baby Boomer business owners to build legacy strategies that coordinate annuities, life insurance, and trust structures into a single, tax-aware plan. Through The Retirement Bank Method™, Premier72 helps you turn business equity into transferable retirement assets while protecting what you pass on. Whether you are evaluating a private annuity sale, structuring beneficiary designations, or planning around the 2026 exemption, the team at Premier72 builds strategies that fit your actual situation, not a template. You can also explore how to include life settlements in your wealth transfer plan as a complementary strategy alongside annuities.

FAQ

What is the main benefit of annuities in legacy planning?

Annuities provide tax-deferred growth and bypass probate through direct beneficiary designations, making them efficient tools for transferring wealth to heirs outside the court system.

Do heirs pay taxes on inherited annuities?

Yes. Inherited annuities do not receive a stepped-up cost basis, so heirs pay ordinary income tax on all accumulated gains, which is typically a higher rate than capital gains tax.

Can you put an annuity inside a trust?

You can, but IRS Section 72(u) eliminates tax deferral when a non-natural person like an irrevocable trust owns the contract. Grantor trusts are the preferred structure because they preserve tax deferral.

What is a private annuity and how does it help with estate taxes?

A private annuity transfers an appreciated asset to a family member or trust in exchange for lifetime income payments, removing the asset from your taxable estate under the 2026 federal exemption of $13.99 million.

How much of your retirement assets should go into annuities?

There is no universal rule, but over-annuitizing reduces legacy flexibility. Most advisors recommend annuitizing only the gap between guaranteed income sources and actual spending needs, keeping at least 30–40% of assets outside annuity contracts.