Long-term care insurance is a policy designed to cover extended custodial care costs when aging, chronic illness, or disability prevents you from performing everyday activities on your own. Standard health insurance and Medicare do not pay for this type of ongoing personal assistance, which creates a significant financial gap for most families. About 70% of people age 65+ will need some form of long-term care, and the national median cost for a private nursing home room runs close to $130,000 per year. That number alone explains why long-term care coverage belongs in any serious retirement plan.

What is long-term care insurance and what does it cover?

Long-term care insurance, often called LTC insurance in the industry, covers custodial care across multiple settings including your home, assisted living facilities, nursing homes, and adult day care centers. Custodial care is personal assistance with activities of daily living, known as ADLs. These are the basic physical tasks most people take for granted until they can no longer do them independently.

The six ADLs that most policies recognize are bathing, dressing, toileting, transferring (moving from bed to chair), continence, and eating. Policies typically require that you be unable to perform at least two of these six activities before benefits begin. Cognitive impairment from conditions like Alzheimer's disease also triggers benefits under most contracts, though the exact criteria vary by policy.

What LTC insurance does not cover is equally worth knowing. It does not pay for skilled medical care like surgery, hospital stays, or physician visits. Those costs fall under Medicare and standard health insurance. Medicare does not cover ongoing custodial care after a short-term skilled nursing stay, which is the gap LTC insurance fills.

Here is what a typical long-term care policy covers:

- Home care: Personal care aides, homemaker services, and informal supervision in your own residence

- Assisted living: Room, board, and personal care in a licensed residential facility

- Nursing home care: Full-time skilled and custodial care in a licensed nursing facility

- Adult day care: Supervised daytime programs for people who need assistance but live at home

- Memory care units: Specialized facilities for individuals with dementia or Alzheimer's disease

Pro Tip: Ask any insurer to show you the exact benefit trigger language in writing before you buy. The difference between "unable to perform 2 of 6 ADLs" and "unable to perform 3 of 6 ADLs" can determine whether your claim gets approved.

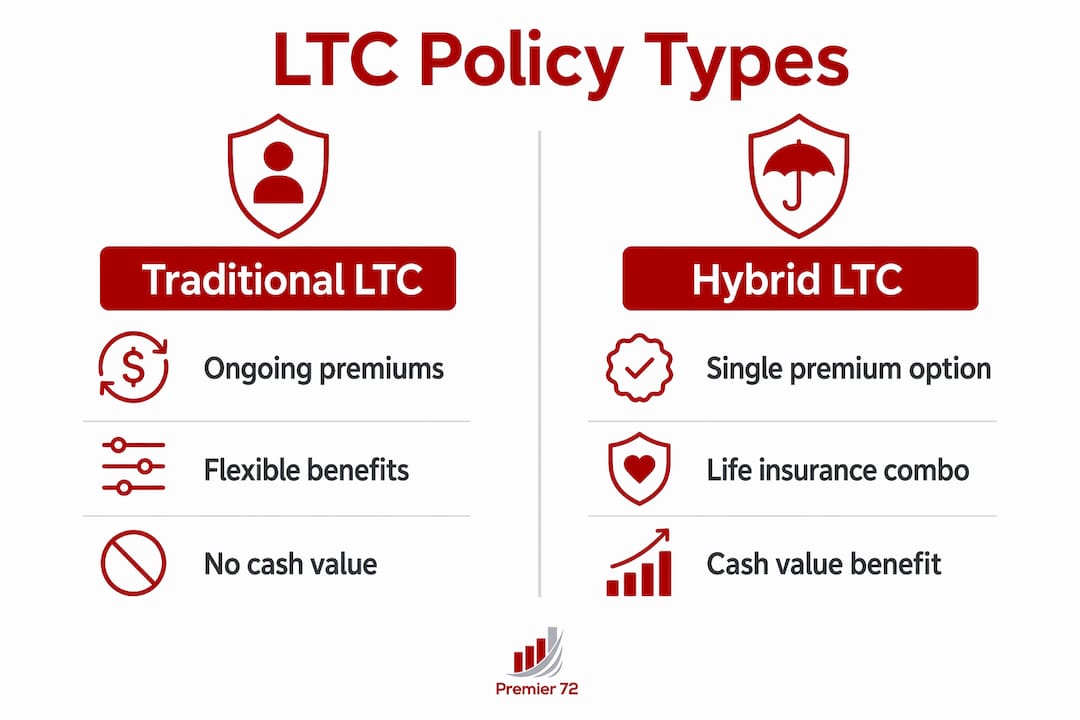

What are the main types of long-term care policies?

Two primary structures exist: traditional standalone LTC insurance and hybrid policies that combine LTC coverage with life insurance or annuities. Each serves a different financial profile, and neither is universally better.

Traditional LTC policies let you choose a daily or monthly benefit amount, a benefit period, and an elimination period (the waiting period before benefits begin). A common structure might be $6,000 per month for three years, with a 90-day elimination period. Premiums are paid monthly or annually, often for life or over a shortened payment window of 10 to 20 years. The main criticism of traditional policies is the "use-it-or-lose-it" nature. If you never need care, you receive nothing back.

Hybrid policies combine LTC coverage with a life insurance or annuity chassis. If you use the LTC benefit, the policy pays for your care. If you never need care, a death benefit passes to your heirs. Some hybrid products also accumulate cash value. The tradeoff is a higher upfront cost, often funded with a single lump-sum premium rather than ongoing payments.

| Feature | Traditional LTC | Hybrid LTC |

|---|---|---|

| Premium structure | Ongoing monthly or annual payments | Often single lump-sum or limited pay |

| If care is never needed | No return of premium | Death benefit paid to heirs |

| Cash value | None | Builds in some products |

| Premium stability | Subject to rate increases | Generally locked in at issue |

| Flexibility | High customization of benefits | Less flexible but more predictable |

One misconception worth correcting: LTC insurance is not just nursing home insurance. Most modern policies cover home care first, which is where the majority of people prefer to receive assistance. Framing it as "nursing home coverage" causes many families to underestimate its value.

Pro Tip: If premium stability matters to you, hybrid policies funded with a single premium eliminate the risk of future rate increases that have historically affected traditional LTC policyholders.

When is the best time to buy long-term care insurance?

The optimal purchase window is your mid-50s to mid-60s. Buying in this range gives you the best combination of affordable premiums and medical eligibility. Policies are typically unavailable past age 75, and health conditions that develop in your 60s and 70s can disqualify you entirely.

Delaying purchase risks higher premiums and potential disqualification due to health changes. A diagnosis of diabetes, heart disease, or early cognitive decline can make you uninsurable for traditional LTC coverage. This is not a theoretical risk. It is the most common reason families find themselves without coverage when they need it most.

Several factors drive the cost of long-term care insurance:

- Age at purchase: Younger buyers pay significantly lower premiums for the same coverage

- Health status: Insurers underwrite based on your medical history and current conditions

- Benefit amount: Higher daily or monthly maximums increase premiums proportionally

- Benefit period: A lifetime benefit period costs more than a two or three-year period

- Elimination period: A 90-day waiting period lowers premiums compared to a 30-day period

- Inflation protection: A 3% compound inflation rider increases premiums but protects against rising care costs over decades

- Geographic location: Care costs vary widely by state, and some policies adjust benefits accordingly

Premiums depend on age, health, and coverage levels, which means two people buying the same policy at age 55 versus age 65 can pay dramatically different amounts for identical benefits. Fidelity actuary Tom Ewanich has noted that buying earlier results in lower premiums and fewer qualification hurdles, a point that applies regardless of which policy type you choose.

How long-term care insurance fits into retirement planning

LTC insurance functions as a risk-management tool within a broader retirement income plan, not as a standalone product. The financial risk it addresses is specific: a prolonged care event that depletes retirement savings faster than any market downturn could.

Consider how the funding sources for long-term care actually stack up:

- Personal savings and investments: Fully flexible but exposed to depletion risk if care extends for multiple years

- Medicare: Covers short-term skilled nursing care only, up to 100 days under specific conditions, with significant cost-sharing after day 20

- Medicaid: Available only after spending down most assets to poverty-level thresholds, which eliminates the legacy most families want to leave

- Long-term care insurance: Transfers the financial risk to an insurer, preserving retirement assets and giving families more care options

- Hybrid life and LTC policies: Combine wealth transfer with care protection, as explored in detail in this life insurance as a retirement asset guide

LTC insurance protects retirement assets and reduces the financial and emotional burden on family caregivers. That second point matters more than most financial plans acknowledge. When a spouse or adult child becomes the primary caregiver, the cost is not just financial. It affects careers, relationships, and health. A policy that funds professional care preserves family relationships in ways that no spreadsheet captures.

Only about 3% of adults over age 50 carry long-term care insurance despite the high probability of needing care. That gap between need and preparation is where most retirement plans quietly fail.

Key takeaways

Long-term care insurance is the most direct tool for protecting retirement assets from the predictable, high-cost risk of extended custodial care that Medicare and standard health insurance do not cover.

| Point | Details |

|---|---|

| Coverage scope | LTC insurance pays for custodial care at home, in assisted living, and in nursing facilities. |

| Medicare gap | Medicare does not cover ongoing personal care after short-term skilled nursing stays. |

| Policy types | Traditional policies offer flexibility; hybrid policies add a death benefit and premium stability. |

| Best purchase timing | Mid-50s to mid-60s gives the lowest premiums and the best chance of medical qualification. |

| Retirement role | LTC coverage protects savings, preserves legacy, and reduces burden on family caregivers. |

Why the fine print matters more than the premium

Most people shopping for long-term care insurance focus on the monthly premium. That is the wrong starting point. After working with families navigating retirement and legacy planning, the single most consequential factor I have seen is whether the family understood the benefit triggers before a claim was filed.

Benefit trigger language in LTC contracts determines whether claims are approved. A dementia diagnosis alone does not automatically qualify someone for benefits. The policy must define cognitive impairment as a qualifying trigger, and the impairment must meet the contract's specific standard. Families who discover this at claim time, after years of premium payments, face one of the most avoidable financial surprises in retirement planning.

My advice is to model at least three coverage scenarios before buying: a short care event of one to two years, a moderate event of three to five years, and an extended event of seven or more years. Run each against your retirement income plan to see which scenario creates real financial stress. That exercise tells you how much coverage you actually need, which is almost always different from what a standard illustration shows.

I also caution against over-insuring. A policy with a lifetime benefit period and 5% compound inflation protection sounds ideal on paper, but if the premium crowds out retirement savings contributions in your 50s, you have traded one risk for another. The goal is coverage that fits your financial reality, not the most comprehensive policy available.

View LTC insurance as both a financial and emotional decision. The peace of mind it provides, knowing that a care event will not force your family to choose between your comfort and their financial security, is a real and measurable benefit.

— Asa

How Premier72 can help you plan for long-term care

Planning for long-term care costs is one of the most personal financial decisions a family makes, and the stakes are high enough that generic advice rarely serves anyone well.

Premier72 works with business owners, professionals, and families to build insurance and retirement strategies that account for real-world risks, including the cost of extended care. Whether you are evaluating a traditional LTC policy, exploring a hybrid life and LTC solution, or integrating care coverage into a broader legacy plan, Premier72 brings the advisory depth to help you make a confident decision. Visit Premier72 to connect with an advisor and start building a retirement plan that protects what you have worked to build.

FAQ

What does long-term care insurance cover?

Long-term care insurance covers custodial care services including home care, assisted living, adult day care, and nursing home care. Benefits apply when you cannot perform at least two of six activities of daily living or when cognitive impairment meets the policy's defined standard.

How does long-term care insurance work when you file a claim?

Most policies require you to satisfy an elimination period, typically 30 to 90 days of qualifying care costs, before benefits begin. After that, the insurer reimburses or pays directly for covered care up to your policy's daily or monthly maximum.

Is long-term care insurance worth it if you are healthy?

Good health is actually the best time to buy, not a reason to delay. Younger, healthier applicants qualify for lower premiums and face fewer underwriting restrictions, while waiting increases both cost and the risk of disqualification.

What is the difference between traditional and hybrid LTC policies?

Traditional policies offer flexible benefit design with ongoing premiums but no return if care is never needed. Hybrid policies combine LTC coverage with a life insurance or annuity component, providing a death benefit if long-term care is never used.

Who needs long-term care insurance most?

Anyone between ages 50 and 65 with retirement assets worth protecting and a family history of chronic illness or longevity should evaluate LTC coverage seriously. The combination of high care costs and Medicare's limited custodial coverage makes it a relevant consideration for most middle-income and affluent families planning for retirement.