Most people spend less than an hour choosing a life insurance policy — one of the most consequential financial decisions they will ever make. The confusion is understandable. Whole life vs term life explained properly can feel like learning a foreign language, especially when agents and brochures lean heavily on jargon. This article cuts through that noise. You will walk away understanding exactly how these two types of policies work, what they cost, when each one makes sense, and how to avoid the most common mistakes people make when comparing them.

Table of Contents

- Key takeaways

- Whole life vs term life explained: the basics

- Weighing the pros and cons

- When each type of policy fits your life

- How to make the right choice

- What you need to know about cash value and conversion

- My honest take after years in this space

- How Premier72 can help you decide

- FAQ

Key takeaways

| Point | Details |

|---|---|

| Term life is affordable protection | A $500K term policy at 35 costs roughly $25–35/month versus $300–400/month for whole life. |

| Whole life builds cash value | Whole life grows tax-deferred cash value you can borrow against, but it is not a substitute for investing. |

| Term fits most people's core needs | Most financial planners recommend term for income replacement and temporary financial obligations. |

| Whole life suits legacy planning | Permanent coverage makes sense for estate planning, lifelong dependents, or tax-advantaged wealth transfer. |

| Blended strategies often win | Combining a term policy with a smaller whole life policy addresses both short-term and permanent needs. |

Whole life vs term life explained: the basics

Before comparing them, you need to understand what each policy actually is.

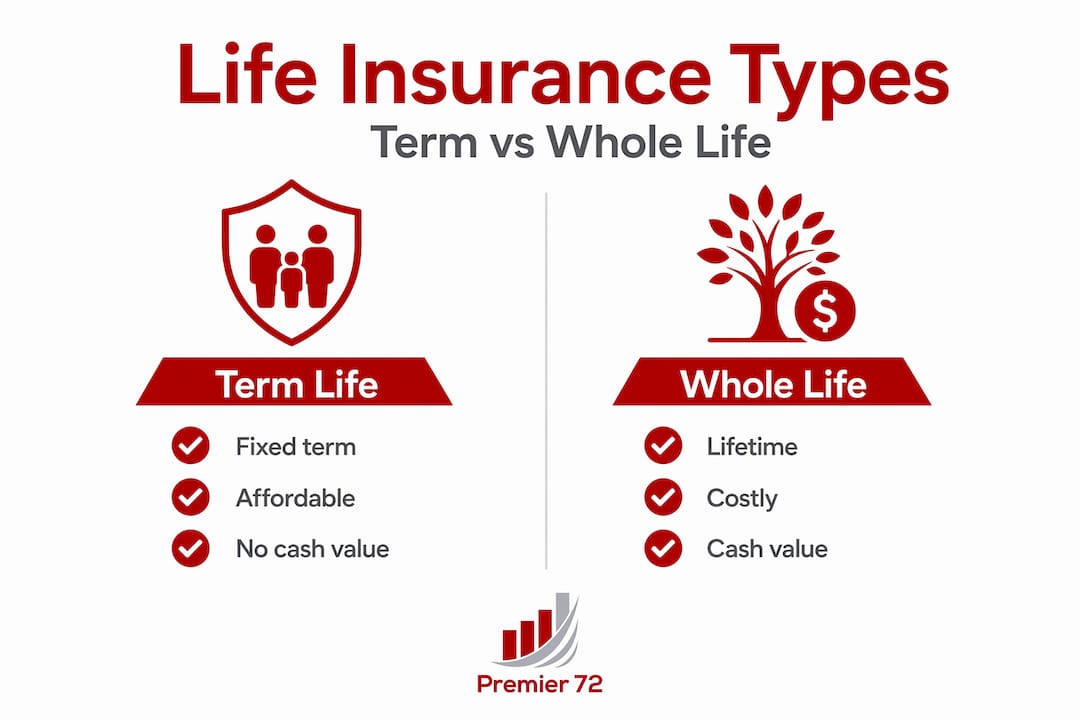

Term life insurance is exactly what it sounds like. You pay premiums for a set period, typically 10, 20, or 30 years. If you die during that term, your beneficiaries receive the death benefit. If you outlive the policy, coverage ends and you get nothing back. There is no cash value, no investment component. It is pure protection.

Whole life insurance is permanent coverage. As long as you pay premiums, the policy stays in force for your entire life. Premiums are fixed and higher than term from day one. Part of each premium funds a cash value account that grows tax-deferred at 2–4% and can be borrowed against or surrendered.

The cost difference is where most people feel the shock. A healthy 35-year-old buying a $500,000 policy will pay roughly $25–35 per month for term life versus $300–400 per month for whole life with the same death benefit. That is a factor of ten. For a family on a working budget, this gap alone often decides the question.

| Feature | Term Life | Whole Life |

|---|---|---|

| Coverage duration | Fixed term (10–30 years) | Lifetime |

| Premiums | Low, fixed during term | Higher, fixed permanently |

| Cash value | None | Grows tax-deferred |

| Death benefit | Paid only if death during term | Guaranteed whenever you die |

| Policy loans | Not available | Available against cash value |

| Dividends | None | Possible, not guaranteed |

One detail worth understanding early: whole life dividends are bonuses tied to insurer performance. They are not guaranteed and are legally treated as a return of premium, which makes them non-taxable. Do not buy a policy banking on dividends as income.

Weighing the pros and cons

Understanding the trade-offs on both sides is where most buyers get clarity.

The case for term life

- Affordability. The same premium dollars buy far more coverage. A 35-year-old can get $1 million in term life coverage for under $60/month.

- Simplicity. No cash value calculations, no loan provisions, no surrender charges. You pay, you are covered.

- Flexibility. Lock in a 20-year term during your peak earning and debt years, then reassess when the kids are grown and the mortgage is paid off.

- Recommended for most. Term life is recommended for 80–90% of insurance seekers because it delivers maximum coverage at the lowest cost for common financial milestones.

The case for whole life

- Permanent protection. No expiration date. Your family is covered whether you die at 55 or 95.

- Guaranteed death benefit. Unlike term, there is no risk of outliving coverage.

- Cash value access. The policy accumulates value you can use for emergencies, retirement income supplements, or business needs.

- Estate and legacy planning. Whole life is a legitimate tool for funding buy-sell agreements, covering estate taxes, or leaving a guaranteed inheritance.

Pro Tip: Do not let the cash value argument sell you a policy you cannot afford to keep. A lapsed whole life policy delivers no death benefit and potentially heavy tax consequences. Affordability is the foundation of any sound insurance plan.

The biggest mistake buyers make is treating whole life as a primary investment vehicle. Whole life should not replace diversified investments. Its conservative returns serve permanent protection and legacy goals, not wealth accumulation.

When each type of policy fits your life

Neither product is universally better. The right answer depends on where you are in life, what you owe, and who depends on you.

Situations where term life wins

- You have young children and a mortgage. Your family needs maximum income replacement for the next 20 years. Term provides it at a fraction of whole life's cost.

- You are carrying business debt or a personal loan. You need coverage tied to the debt's lifespan, not a lifelong policy.

- Your budget is tight. A $1 million term policy beats a $250,000 whole life policy you struggle to maintain. More coverage matters more than policy features.

- You plan to self-insure over time. If your investment strategy will build enough wealth to make insurance unnecessary by retirement, temporary coverage is all you need.

Situations where whole life earns its higher premium

- You have a lifelong dependent. A child with a disability or a spouse who will never be financially independent needs coverage that does not expire.

- You are planning your estate. Whole life is a clean way to fund legacy planning and offset estate taxes with a guaranteed, tax-free death benefit.

- You own a business. Whole life commonly funds buy-sell agreements and key person coverage, where the certainty of the death benefit and cash value are both valuable.

- You want tax-advantaged savings alongside protection. For high earners who have maxed out retirement accounts, whole life offers a tax-deferred accumulation option within a guaranteed protection structure.

Pro Tip: A blended approach works well for many families. Carry a larger term policy through your peak income years and a smaller whole life policy to cover permanent legacy needs. You get the affordability of term where you need volume and the permanence of whole life where it counts.

Age also matters for access. Many insurers stop accepting new term applications around ages 75–80, while whole life is available up to 85–90 at higher premiums. If you are older and still have dependents or estate needs, whole life may be your only viable path to new coverage.

How to make the right choice

Choosing between these two products comes down to asking the right questions about your own situation.

- How long do you need coverage? If the answer is tied to a specific debt, career phase, or family milestone, term is almost certainly the right answer. If the answer is "for my entire life," whole life earns consideration.

- What can you realistically afford? A policy you can maintain is worth infinitely more than a policy you drop in year seven. Run your household budget before deciding.

- Do you have other investments? If you have a 401(k), IRA, and a diversified portfolio, whole life's cash value adds modest incremental value. If you have no other savings, whole life's conservative returns are not a substitute.

- What riders matter to you? Many term policies include a convertibility option allowing you to convert to whole life later without new health underwriting. Accelerated death benefit riders on either policy type allow early access to funds during a terminal illness. These features add real flexibility worth asking about.

- Are you protecting a business? Key person coverage, buy-sell funding, and business succession often require the permanent nature and cash value access of whole life.

A common misconception is that whole life is always a bad deal. That is simply not true for the right buyer. It is a poor fit for someone seeking investment returns. It is an excellent fit for someone who needs permanent coverage and has the budget to maintain it.

Check out how cash value grows over time in permanent policies to understand the long-term mechanics before committing.

What you need to know about cash value and conversion

The cash value component of whole life is genuinely useful, but it comes with rules most buyers do not read carefully enough.

When you take a loan against cash value, you are not withdrawing your money. You are borrowing against it. The loan accrues interest. If you do not repay it, the balance reduces your death benefit dollar for dollar. Over-borrow and the policy can lapse entirely, triggering a taxable event on any gains. This is not a theoretical risk. It happens regularly when policyholders treat their whole life policy like a checking account.

| Cash value action | What actually happens |

|---|---|

| Policy loan taken | Death benefit reduced by loan balance |

| Loan left unpaid | Interest compounds, accelerating benefit reduction |

| Policy lapses with loan | Taxable income event on outstanding gains |

| Dividends received | Non-taxable return of premium, not guaranteed |

| Surrender before death | Cash value minus surrender charges paid out; coverage ends |

On the term side, one underutilized feature is the conversion rider. Many term policies let you convert to whole life before the term ends without a new medical exam. This is particularly valuable if your health declines during the term period. You lock in insurability now, even if you do not immediately need permanent coverage.

Renewal after term expiration is almost always prohibitively expensive. A 65-year-old renewing a term policy pays rates based on current age and health, which can multiply the premium by five or more. Planning for what comes after your term period ends is part of choosing life insurance wisely.

My honest take after years in this space

I have sat with a lot of clients who came in convinced they needed whole life because an advisor made the cash value sound irresistible. And I have sat with others who carried nothing but a small term policy and were severely underinsured when life took an unexpected turn.

What I have learned is this: most people need more coverage than they think, and the biggest threat to that coverage is a premium they cannot sustain for decades. A $1.5 million term policy that gets renewed and maintained is a far better legacy than a $400,000 whole life policy that gets surrendered at 58 when money gets tight.

That said, I have seen whole life do exactly what it promises for the right client. Business owners funding a buy-sell agreement. Families protecting a child who will need financial support forever. High-earning professionals building a tax-advantaged supplement to their retirement plan. In those situations, whole life is not just worth it. It is the right tool.

The trap is letting the conversation get hijacked by cash value projections and dividend illustrations. Those are secondary benefits of a protection product. Ask yourself what you need protected and for how long. The answer to that question points you to the right policy faster than any rate-of-return chart ever will.

— Asa

How Premier72 can help you decide

Choosing between whole and term life is rarely just an insurance question. For business owners, it intersects with succession planning, key person protection, buy-sell funding, and retirement income strategy. That is exactly where Premier72 specializes. Premier72 works with established business owners, professionals, and families to build protection strategies that align with long-term financial goals, not just a coverage checkbox. Whether you are weighing a blended policy approach, exploring how life insurance fits into your family's financial future, or planning for business continuity, Premier72 can help you think through the right structure for your situation.

FAQ

What is the main difference between whole and term life?

Term life provides coverage for a fixed period with no cash value, while whole life is permanent coverage that builds tax-deferred cash value. Term costs significantly less for the same death benefit.

Is whole life insurance worth it?

Whole life is worth it for specific situations: lifelong dependents, estate planning, business buy-sell agreements, or tax-advantaged wealth transfer. For most people needing income replacement, term life is a better fit.

Can I convert my term life policy to whole life?

Yes. Many term policies include a conversion option that lets you switch to whole life without new medical underwriting, which is especially valuable if your health changes during the term period.

How does cash value in whole life actually work?

Cash value grows tax-deferred inside a whole life policy and can be accessed through loans. However, unpaid policy loans reduce the death benefit and can cause the policy to lapse if the balance grows too large.

How do I choose between whole life and term life?

Start with how long you need coverage, what you can afford to pay for decades, and whether you have permanent financial obligations. Most buyers under 60 with standard income replacement needs are best served by term life.