Annuity income is defined as a guaranteed stream of payments an insurer delivers to you for life, in exchange for a lump sum or series of premiums. For Baby Boomer business owners and retirees, this annuity income retirement planning guide addresses the single biggest financial risk you face: outliving your money. Annuities convert assets into lifelong payments, protecting against longevity risk regardless of how markets perform. The industry term for this protection is "longevity risk transfer," and it sits at the center of every serious retirement income strategy. Premier72 works with business owners who have spent decades building wealth and now need a plan to make that wealth last.

What are the main types of annuities and how do they work?

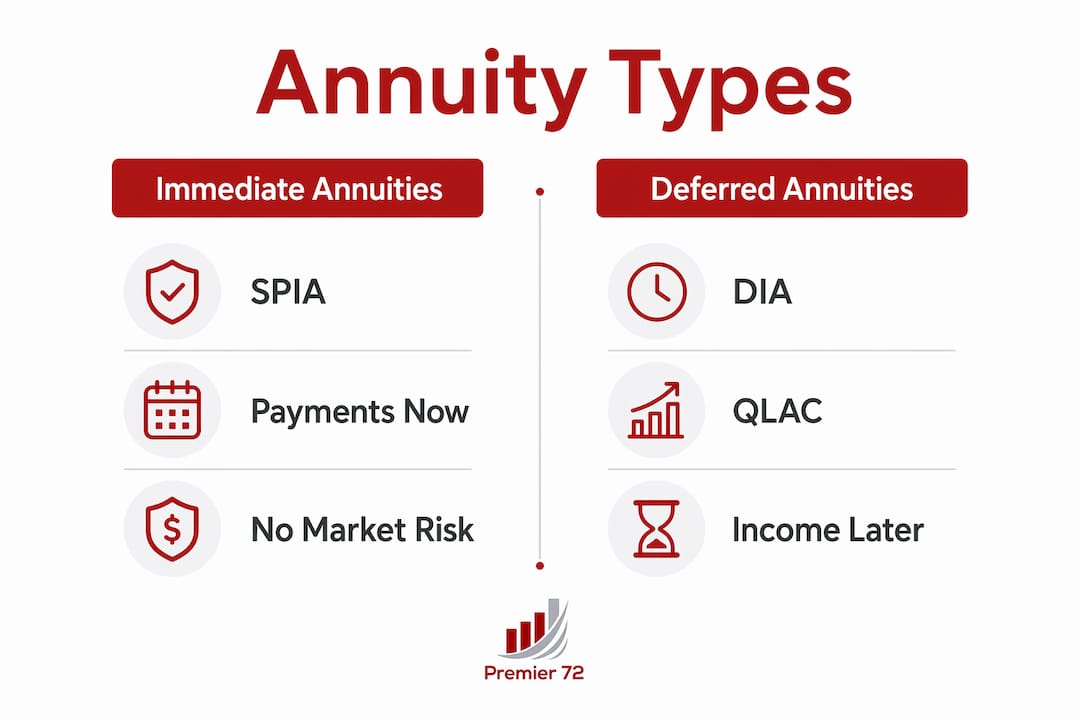

The four core annuity types are immediate, deferred, fixed, and variable. Each serves a different income timeline and risk tolerance. Knowing which fits your situation is the first decision in any retirement income strategy.

Single Premium Immediate Annuities (SPIAs)

A SPIA starts paying within 30 days of purchase. You hand over a lump sum, and the insurer begins monthly, quarterly, or annual payments almost immediately. SPIAs require a minimum deposit of around $10,000, making them accessible for retirees who want income to start now. This structure suits anyone who has already retired and needs to replace a paycheck.

Deferred Income Annuities and QLACs

Deferred Income Annuities (DIAs) and Qualified Longevity Annuity Contracts (QLACs) are the right tools when income starts beyond one year from purchase. You buy them today, income begins at a future date you choose, often age 75 or 80. QLACs are funded from qualified retirement accounts like IRAs and carry IRS contribution limits. DIAs, by contrast, can be funded with nonqualified money.

Fixed vs. variable annuities

Fixed annuities credit a set interest rate and carry no market risk. Variable annuities tie your account value to investment subaccounts, so returns fluctuate with the market. Fixed products deliver predictability. Variable products offer growth potential but expose you to loss, which defeats the purpose of guaranteed income for many retirees.

How mortality credits make annuity payments larger

Mortality credits are the mechanism that lets annuities pay more than a comparable bond or CD. Insurers pool premiums from all policyholders. When some annuitants die earlier than expected, their unused premiums flow to those who live longer. This redistribution is why a lifetime annuity can pay a 70-year-old more per month than they could safely withdraw from a savings account.

| Annuity type | Income start | Market risk | Best for |

|---|---|---|---|

| SPIA | Immediate (30 days) | None | Retirees needing income now |

| DIA | 1+ years deferred | None | Planning future income gaps |

| QLAC | Age 75–85 | None | IRA holders managing RMDs |

| Fixed | Flexible | None | Predictable, low-risk growth |

| Variable | Flexible | Yes | Growth-oriented retirees |

Pro Tip: If you are unsure whether to start income now or defer it, map your essential monthly expenses against your current guaranteed income sources first. The gap tells you exactly how much annuity income you need and when.

How to determine if an annuity fits your retirement income plan

The right time to buy an annuity is when your guaranteed income sources, Social Security, pensions, and other fixed payments, fall short of covering your essential monthly expenses. That gap is your annuity target. Every dollar of essential expense covered by guaranteed income is a dollar you never have to worry about.

Here is a practical framework for assessing fit:

- List your essential monthly expenses. Include housing, food, utilities, healthcare premiums, and insurance. These are non-negotiable costs that must be covered regardless of market conditions.

- Add up your guaranteed income. Total your Social Security benefit, any pension, and any existing annuity payments. Subtract this from your essential expenses.

- Identify the gap. If guaranteed income falls short, that shortfall is the amount an annuity should cover.

- Assess your timeline. If you need income now, a SPIA fits. If income is needed in five or ten years, a DIA or QLAC gives you more flexibility and a higher payout.

- Evaluate your liquidity position. Annuities are illiquid; once annuitized, you lose access to that principal. Before committing, confirm you hold at least six to twelve months of living expenses in accessible accounts.

Liquidity is the most underestimated constraint. Surrender charges on deferred annuities can run for seven to ten years, and the permanent loss of principal access after annuitization is real. You cannot undo it.

One funding advantage many business owners overlook: nonqualified money carries no IRS contribution limits when used to fund an annuity. If you have after-tax capital sitting in a business account or savings, you can move it into an annuity without the restrictions that apply to IRAs or 401(k)s.

Pro Tip: Never put all liquid assets into an annuity. A common rule among income planners is to keep at least 20% of your total retirement assets in accessible, liquid accounts before annuitizing any portion.

How do you purchase the right annuity?

Buying an annuity is a contract decision, not an investment decision. The process requires more due diligence than buying a mutual fund because you are locking in a relationship with an insurer for decades.

- Check the insurer's financial strength rating. Ratings from agencies like A.M. Best, Moody's, and Standard & Poor's reflect an insurer's ability to pay claims over time. Carrier financial strength matters more than the highest initial payout rate. A slightly lower monthly payment from a financially strong insurer is a better deal than a higher payment from a weaker one.

- Focus on contractual guarantees, not sales projections. Variable and indexed annuity illustrations often show optimistic scenarios. The only number that matters is the guaranteed minimum. Ask for the guaranteed floor in writing before signing.

- Review payout options carefully. Life-only pays the highest monthly amount but stops at death. Joint-and-survivor continues payments to a spouse. Period-certain guarantees payments for a set number of years. Each option changes the monthly amount significantly.

- Understand rider costs. Income riders, death benefit riders, and long-term care riders add features but also add annual fees, often 0.5% to 1.5% of account value per year. Confirm whether each rider delivers value for your specific situation.

- Get quotes from multiple carriers. Payout rates vary by insurer, age, gender, and interest rate environment. Comparing at least three to five quotes is standard practice.

Pro Tip: Ask every carrier for the "contractual guarantee page" of the illustration, not the projected page. That single document tells you the worst-case scenario, which is the only scenario you should plan around.

A checklist before you sign: confirm the insurer's rating is A or better, verify the surrender charge schedule, confirm the payout option in writing, and review the free-look period, typically 10 to 30 days, during which you can cancel without penalty.

How do annuities integrate with other retirement income sources?

Annuities work best as the foundation of a retirement income floor, not as a standalone solution. Annuities complement Social Security and pensions by filling the gap between fixed government benefits and total essential expenses. That combination creates a base of guaranteed income that covers your needs no matter what markets do.

Key integration principles:

- Cover essentials first. Use guaranteed income sources, Social Security, pensions, and annuities, to cover every non-negotiable expense. Discretionary spending can come from investment accounts.

- Sequence withdrawals strategically. Draw from taxable accounts first, then tax-deferred accounts like IRAs, and let Roth accounts grow longest. Annuities inside IRAs affect required minimum distributions, so coordinate timing with a tax advisor.

- Protect against market volatility. When your essential expenses are fully covered by guaranteed income, you can afford to hold equities in your investment portfolio through downturns without panic-selling.

- Consider tax deferral. Nonqualified deferred annuities grow tax-deferred until withdrawal. This can be useful for business owners who have maxed out qualified plan contributions.

- Plan for legacy. Some annuity contracts include death benefit riders or return-of-premium features. These reduce monthly income but preserve capital for heirs. Weigh the cost against your legacy goals.

Retirees who also own a home have an additional option worth knowing: a reverse mortgage for homeowners 62+ can supplement annuity income by converting home equity into tax-free cash flow without a monthly payment obligation. This strategy works particularly well when a retiree wants guaranteed income from an annuity but also needs liquidity from another source.

Retirement income planning best practices consistently show that retirees with multiple guaranteed income streams report higher financial confidence and spend more freely than those relying solely on portfolio withdrawals.

Key Takeaways

Annuities deliver guaranteed lifetime income that no market downturn can eliminate, making them the most reliable tool for covering essential retirement expenses.

| Point | Details |

|---|---|

| Match annuity type to timeline | SPIAs work for immediate income; DIAs and QLACs work for future income gaps. |

| Prioritize insurer strength | Choose a carrier rated A or better over one offering a higher payout from a weaker balance sheet. |

| Protect liquidity first | Keep at least six to twelve months of expenses in accessible accounts before annuitizing. |

| Fill the income gap | Calculate essential expenses minus guaranteed income to determine the exact annuity amount needed. |

| Integrate with other sources | Pair annuity income with Social Security, pensions, and investment accounts for a complete income floor. |

What I've learned from watching retirees get annuities wrong

The most common mistake I see is retirees treating an annuity purchase like a product transaction rather than a long-term income decision. They focus on the monthly payment number and ignore the insurer's financial rating, the surrender charge schedule, and the payout option structure. Those three details determine whether the contract actually serves them for 20 or 30 years.

Business owners face a specific version of this problem. After spending decades with capital working inside a business, the idea of locking money into an illiquid contract feels unnatural. That discomfort is valid. The answer is not to avoid annuities. The answer is to size the annuity correctly so it covers your income gap without straining your liquidity.

Building a retirement income plan that incorporates annuities requires understanding your full financial picture first. No single annuity type is right for everyone. The right product depends on your age, income gap, tax situation, and how much flexibility you need. Work with an advisor who will show you the contractual guarantee page, not just the optimistic projection.

— Asa

How Premier72 approaches retirement income planning

Premier72 works with Baby Boomer business owners who have spent their careers building companies and now need a clear plan to convert that success into lasting retirement income.

Through The Retirement Bank Method™, Premier72 helps owners reduce dependence on their business, improve transferable value, and build income strategies that work whether they sell, transition, or retire in place. Annuities are one tool in that plan, selected and sized based on your specific income gap, tax situation, and timeline. If you are ready to build a retirement income plan that covers your essential expenses for life, visit Premier72 to learn how the firm approaches income planning for business owners and retirees.

FAQ

What is annuity income in retirement planning?

Annuity income is a guaranteed stream of payments an insurer provides in exchange for a lump sum premium. It covers essential retirement expenses for life, regardless of market performance.

What are the best annuities for guaranteed lifetime income?

SPIAs deliver the highest guaranteed income for retirees who need payments now. DIAs and QLACs are better for retirees who want to lock in future income at a higher payout rate.

How do I know if an annuity fits my retirement plan?

Calculate your essential monthly expenses, subtract your guaranteed income sources, and identify the gap. If a gap exists, an annuity sized to cover that shortfall is worth evaluating.

Are annuities liquid investments?

Annuities are not liquid. Once annuitized, the principal is inaccessible, and deferred annuities carry surrender charges for seven to ten years. Maintain a separate liquid emergency fund before purchasing.

How do annuities work with Social Security and pensions?

Annuities fill the income gap between Social Security and pension payments and your total essential expenses. Together, these guaranteed sources form a retirement income floor that protects against market downturns.