Annuities are contracts that convert a lump sum into a predictable, lifetime income stream backed by the financial strength of an insurance company. For Baby Boomers approaching retirement, this single feature solves the most pressing financial problem you face: the risk of outliving your money. Social Security replaces only a fraction of pre-retirement income, and traditional pensions have largely disappeared. Annuities fill that gap by transferring longevity risk to insurers who pool assets across thousands of contract holders to guarantee payments no matter how long you live.

Why annuities provide guaranteed income: the core mechanism

The guarantee behind an annuity payment is not magic. It is math combined with the financial strength of large insurance companies. When you purchase an annuity, your premium joins a pool of assets from thousands of other contract holders. The insurer invests that pool and uses actuarial science to calculate how long, on average, the group will live. Some members die early; others live past 95. The pool absorbs both outcomes, which is why annuities eliminate longevity risk in a way that bonds and stock portfolios simply cannot.

Bonds carry market risk. If interest rates rise after you buy a bond, its value drops. If the issuer defaults, payments stop. An annuity from a financially strong carrier keeps paying regardless of market conditions. That is the structural advantage.

The reliability of those payments depends entirely on the insurer's claims-paying ability. Independent rating agencies including A.M. Best, Moody's, and S&P evaluate each carrier's financial strength. Guardian Life, for example, has paid obligations continuously since 1860, surviving every recession, depression, and market crash in that span. That track record is the kind of evidence worth examining before you sign any contract.

Key factors that support an annuity's income guarantee:

- Pooled longevity risk: Payments are funded by a large group, not your individual account balance alone.

- Insurer financial ratings: A.M. Best, Moody's, and S&P ratings signal the carrier's ability to pay claims decades from now.

- Actuarial pricing: Insurers price contracts to remain solvent across a wide range of life expectancy outcomes.

- State guaranty associations: Most states provide a backstop (typically up to $250,000) if an insurer fails, adding a secondary layer of protection.

Pro Tip: Before purchasing any annuity, look up the carrier's A.M. Best rating. Stick with carriers rated A or better. A slightly lower payout rate from a stronger carrier is almost always the smarter trade.

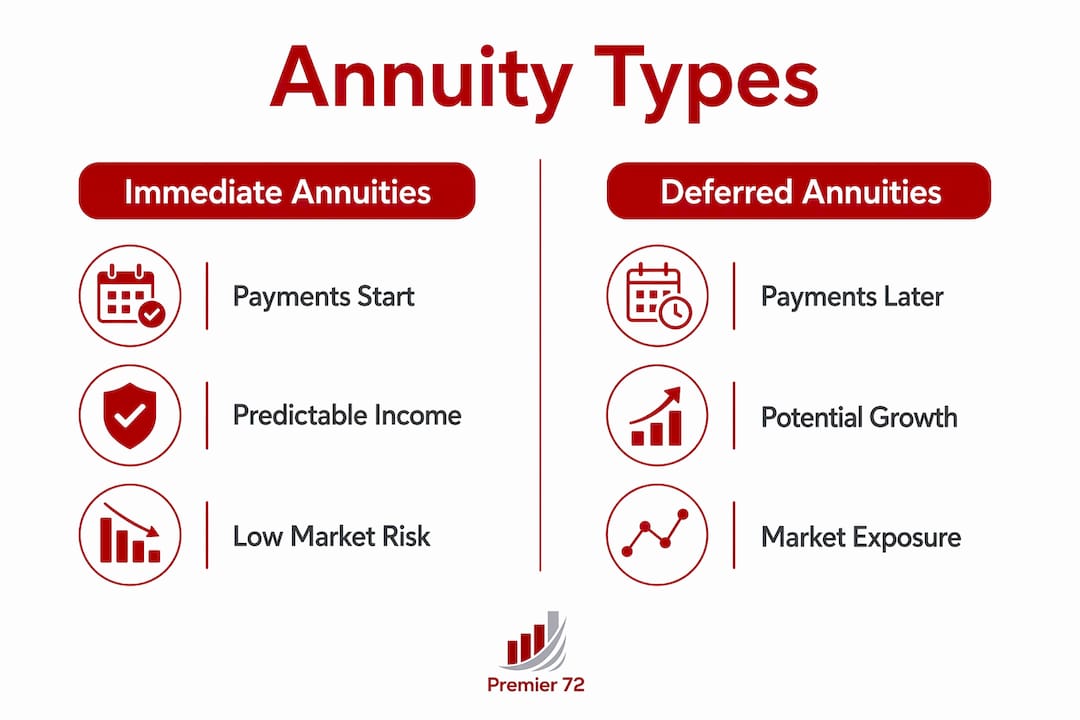

What are the different types of annuities?

Not all annuities work the same way. The type you choose determines when payments start, how much market exposure you carry, and how much flexibility you retain. Understanding these differences is the foundation of a sound decision. The Premier72 blog covers annuity types in detail for 2026, but here is the core breakdown.

| Annuity Type | When Payments Start | Market Exposure | Best For |

|---|---|---|---|

| Immediate (SPIA) | Within 30 days of purchase | None | Retirees needing income now |

| Deferred Income | Future date you choose | None | Pre-retirees locking in future income |

| Fixed (MYGA) | At maturity or annuitization | None | Predictable, guaranteed growth |

| Variable | At annuitization | High | Growth-focused, higher risk tolerance |

| Fixed Indexed | At annuitization | Partial (capped upside) | Balance of protection and growth |

Immediate annuities, also called Single Premium Immediate Annuities (SPIAs), convert your lump sum into income within a month. They are the purest form of guaranteed income and carry no market exposure. Deferred annuities let your money grow before payments begin, which is useful if you are 58 and want income starting at 67.

Fixed annuities, including Multi-Year Guaranteed Annuities (MYGAs), offer a set interest rate for a defined period. As of early 2026, MYGAs from A-rated carriers are paying between 4.75% and 5.25%. That is a competitive rate compared to most CDs and Treasury bonds at similar maturities.

Variable annuities tie your income to investment sub-accounts. They offer growth potential but introduce the same market volatility you were trying to escape. Fixed indexed annuities split the difference: your principal is protected, but growth is linked to an index like the S&P 500, subject to a cap or participation rate.

Pro Tip: If your primary goal is income security rather than growth, start with a SPIA or MYGA. Variable annuities make sense only if you have already covered your essential expenses with guaranteed sources and want additional upside on discretionary funds.

How do you evaluate and select the right annuity?

Choosing an annuity requires more than comparing payout rates. The process starts with understanding how much guaranteed income you actually need, then selecting the carrier and product that delivers it reliably.

-

Calculate your income gap. Add up your essential monthly expenses: housing, food, healthcare, utilities. Subtract your guaranteed income from Social Security and any pension. The remaining amount is your income gap. That is the number an annuity needs to cover.

-

Determine your allocation. Financial planners recommend allocating 25%–50% of investable assets to annuities to cover the income gap. Annuitizing more than 50% often sacrifices too much liquidity. Annuitizing less than 25% may leave the gap uncovered.

-

Vet the carrier's financial strength. Review ratings from A.M. Best, Moody's, and S&P before comparing payout rates. Carrier claims-paying ability, not government backing, determines whether your income arrives 30 years from now. Federal deposit insurance does not cover annuities.

-

Compare current rates. SPIA and MYGA rates in 2026 are among the most competitive seen in over a decade. Request quotes from at least three A-rated carriers before committing.

-

Understand the contract terms. Surrender charges, inflation adjustment riders, death benefit options, and joint-life provisions all affect the real value of the contract. Read every term before signing.

-

Limit annuitization to essential expenses. Annuity contracts are irrevocable. Once your principal converts to an income stream, you cannot reverse the decision. Keep the remainder of your portfolio invested for growth, liquidity, and inflation protection.

A well-structured retirement income plan treats annuities as the foundation, not the entire building. Cover your non-discretionary expenses with guaranteed income. Let your investment portfolio handle everything else.

Annuities vs. other retirement income options: pros and cons

Annuities are not the right tool for every dollar in your retirement account. They solve a specific problem extremely well and create real trade-offs in other areas. Here is an honest look at both sides.

The case for annuities:

- Lifetime income: Payments continue regardless of how long you live. Approximately half of 65-year-olds live past age 85, and many reach 90 or beyond. An annuity is the only product that guarantees income for that entire span.

- Market independence: Your income does not drop when the S&P 500 falls 30%. That stability has real psychological and financial value in volatile markets.

- Longevity protection: No other retail financial product transfers longevity risk as directly or as efficiently as an annuity.

The limitations you need to know:

- Fees: Variable annuities carry mortality and expense charges, administrative fees, and rider costs that can total 2%–3% annually. Those fees compound over decades and reduce net returns significantly.

- Inflation exposure: Most annuities do not adjust for inflation. A fixed payment of $3,000 per month today buys less in 15 years. Inflation adjustment riders exist but reduce the initial payout.

- Irrevocability: Once you annuitize, the principal is gone. You cannot access it for emergencies, home repairs, or medical costs.

- Opportunity cost: Money locked in a fixed annuity cannot benefit from a strong equity market. That trade-off is acceptable for essential expenses but costly for discretionary funds.

The right frame is this: annuities are not an investment. They are income insurance. Evaluate them the way you evaluate any insurance product: by the risk they cover and the cost of that coverage, not by comparing their returns to the stock market.

Key takeaways

Annuities provide guaranteed retirement income by transferring longevity risk to financially strong insurance companies that pool assets and pay lifetime income regardless of market conditions.

| Point | Details |

|---|---|

| Core guarantee mechanism | Insurers pool assets from many contract holders to fund lifetime payments regardless of individual longevity. |

| Carrier vetting is non-negotiable | Check A.M. Best, Moody's, and S&P ratings before comparing payout rates from any carrier. |

| Allocate 25%–50% of assets | Cover only your essential income gap with annuities; keep the rest invested for growth and liquidity. |

| Type selection matters | SPIAs and MYGAs suit income-focused retirees; variable annuities add risk that most Baby Boomers do not need. |

| Irrevocability demands caution | Annuity contracts cannot be reversed, so limit annuitization to non-discretionary expenses only. |

The uncomfortable truth about annuity timing

Most of the retirees I work with come in asking the same question: "Should I wait for rates to go higher before buying?" My honest answer is almost always no, and here is why.

Waiting to purchase an annuity while spending down other assets is one of the most common and costly mistakes I see. By the time someone decides rates are "good enough," they have depleted the very capital they planned to annuitize. The income floor they needed at 67 gets established at 74, and the years in between were funded by drawing down a portfolio that was supposed to last 30 years.

The second mistake is over-annuitizing. I have seen people put 80% or 90% of their savings into annuities because the guaranteed income felt so reassuring. Then a major home repair or medical event hits, and they have no liquid assets to cover it. The income floor strategy works precisely because it is a floor, not a ceiling.

My recommendation for 2026 specifically: MYGA rates between 4.75% and 5.25% from A-rated carriers are genuinely attractive. If you have an income gap and a lump sum sitting in a low-yield savings account, the math strongly favors acting now rather than speculating on future rate movements. Buy for security. Buy for the income gap. Do not buy to beat the market.

— Asa

How Premier72 helps you build a guaranteed income plan

Knowing why annuities provide guaranteed income is the first step. Knowing exactly how much to allocate, which carrier to use, and how to integrate an annuity into a complete retirement income plan is where most people need a guide.

Premier72 works with Baby Boomers and business owners to build personalized retirement income strategies that go beyond a single product. Through The Retirement Bank Method™ and insurance-based planning, Premier72 helps you identify your income gap, evaluate A-rated carriers, and structure an allocation that covers your essential expenses without sacrificing liquidity or growth. If you are ready to stop guessing and start planning, visit Premier72 to connect with an advisor who specializes in guaranteed income solutions built for your stage of life.

FAQ

What makes annuity income guaranteed?

Annuity income is guaranteed by the insurance company's claims-paying ability, not government backing. Carriers pool premiums from thousands of contract holders and use actuarial pricing to fund lifetime payments regardless of individual longevity.

How much of my retirement savings should go into an annuity?

Financial planners recommend allocating 25%–50% of investable assets to annuities, targeting only the income gap between your essential expenses and fixed sources like Social Security. Annuitizing more than that typically sacrifices too much liquidity.

Are fixed annuities a good option in 2026?

Fixed annuities, particularly MYGAs from A-rated carriers, are offering rates between 4.75% and 5.25% as of early 2026. Those rates are competitive with CDs and Treasury bonds, making fixed annuities a strong option for retirees prioritizing predictable, guaranteed growth.

What happens to my annuity if the insurance company fails?

State guaranty associations provide a backstop for annuity contracts if an insurer becomes insolvent, typically up to $250,000 per contract holder. This is a secondary protection; the primary defense is selecting a carrier with strong A.M. Best, Moody's, or S&P ratings before purchase.

Can i lose money with an annuity?

With a fixed or immediate annuity, your principal is protected and income is guaranteed. Variable annuities carry market risk and can lose value. The key distinction is that fixed products transfer risk to the insurer, while variable products retain market exposure with the contract holder.