Business partner life insurance is defined as a structured arrangement in which life insurance policies are used within legal frameworks like buy-sell agreements and key person insurance to protect a company's financial stability when a co-owner dies. Without this protection, the death of a partner can trigger ownership disputes, liquidity crises, and forced business sales that destroy decades of built equity. The two primary tools are the buy-sell agreement, which governs who buys the deceased partner's shares and at what price, and key person insurance, which pays the business directly to offset operational losses. Firms like Guardian Life, Mutual of Omaha, and advisors like Premier72 treat these not as separate products but as integrated systems that must align legally, financially, and operationally.

What is a buy-sell agreement and how does it use life insurance to protect partners?

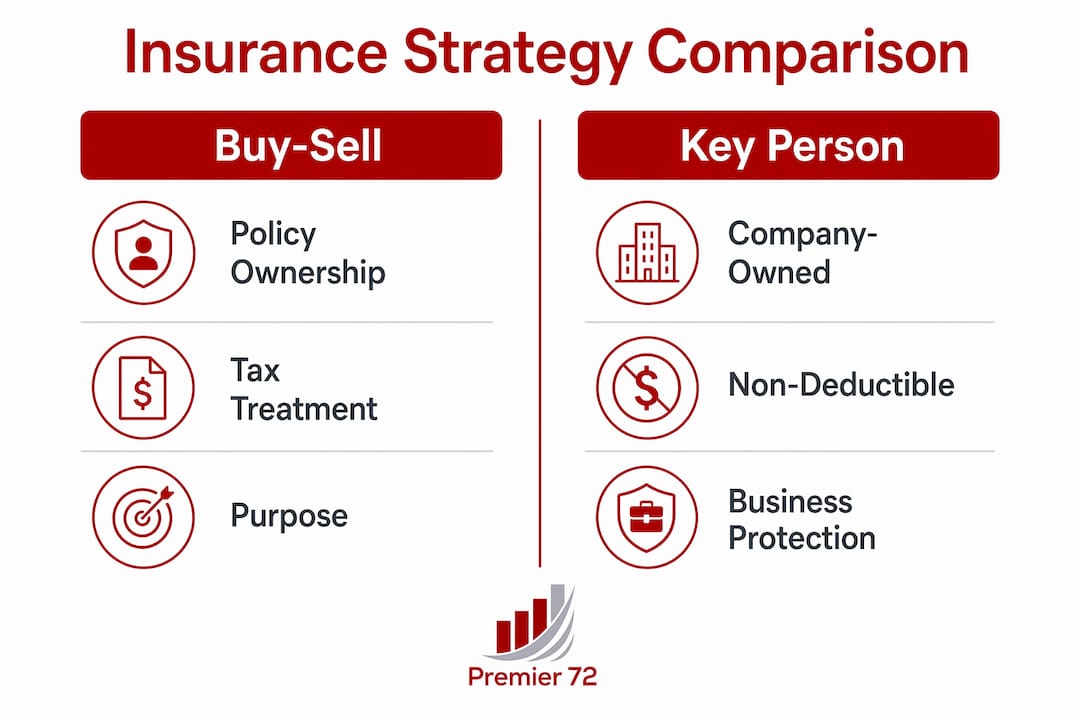

A buy-sell agreement is a legally binding contract that determines what happens to a partner's ownership interest when they die, become disabled, or exit the business. Life insurance is the most common funding mechanism because it creates an immediate, tax-advantaged pool of cash precisely when it is needed most. Buy-sell agreements funded by life insurance create the liquidity required to buy out a deceased partner's shares without forcing the surviving owners to liquidate assets or take on debt.

There are two primary structures for funding a buy-sell agreement with life insurance:

- Cross-purchase agreement: Each partner owns a policy on every other partner. When one partner dies, the surviving partners receive the death benefit and use it to purchase the deceased partner's shares from their estate.

- Corporate redemption (entity purchase): The business itself owns policies on each partner. When a partner dies, the company receives the death benefit and redeems the deceased partner's ownership interest directly.

The administrative complexity of cross-purchase agreements scales sharply with the number of owners. With 5 owners, 20 policies are required under a cross-purchase structure, since each owner must hold a separate policy on every other owner. That number makes administration burdensome and increases the risk of a policy lapsing unnoticed.

On the tax side, life insurance premiums are not deductible for business owners using buy-sell funding, but the death benefit is generally received tax-free by the policy owner. This means the after-tax value of the benefit is preserved, which is a significant advantage over other buyout funding methods like installment notes or bank loans.

| Factor | Cross-purchase | Corporate redemption |

|---|---|---|

| Policy ownership | Individual partners | The business entity |

| Policies needed (5 owners) | 20 | 5 |

| Tax basis step-up | Yes, for surviving partners | No step-up benefit |

| Administrative complexity | High with multiple owners | Lower, centralized |

Pro Tip: Review your buy-sell agreement and the corresponding insurance coverage every two to three years, or immediately after any significant change in business valuation, partner count, or ownership structure.

How does key person insurance differ and protect your business when a partner dies?

Key person insurance is a company-owned life insurance policy that pays the business upon the death of a critical owner or employee. Key person life insurance pays the business to help offset financial harm and support continuity, not to fund a formal ownership transfer. This distinction matters enormously in planning.

The objective of key person coverage is to protect the company's financial position, not to provide a death benefit to the partner's family. Key person insurance offsets business financial loss, covering costs like recruiting a replacement, servicing debt that depended on the key person's relationships, or stabilizing revenue while the business adjusts. It does not replace the legal buyout mechanism that a buy-sell agreement provides.

Key person policies come in two forms:

- Term life insurance: Lower premiums, straightforward coverage for a defined period. Best suited for businesses with a finite planning horizon or tighter budgets.

- Permanent life insurance: Higher premiums but builds cash value over time. Permanent key person insurance builds cash value that can be transferred to an employee at retirement as a compensation perk, adding a retention dimension to the coverage.

Like buy-sell premiums, key person insurance premiums are not deductible as business expenses when the company owns the policy. The business pays with after-tax dollars, but the death benefit is received tax-free. Ownership and beneficiary designations must be set correctly from the start. Tax planning for business life insurance requires considering policy ownership at the outset, not after purchase.

Pro Tip: Coordinate key person insurance with your buy-sell agreement rather than treating them as substitutes. Key person coverage funds operational continuity; the buy-sell agreement funds the ownership transfer. Both are needed for complete protection.

How to choose, implement, and maintain the right life insurance strategy for your business partners

Selecting the right partnership life insurance strategy requires more than picking a policy. It requires aligning legal agreements, insurance structures, and financial planning into one coherent system. Integrated legal and insurance planning protects partnerships far more effectively than relying on either tool alone.

Follow these steps to build a plan that holds up when it matters most:

- Get a current business valuation. Your coverage amount must match your buyout obligation. A valuation done five years ago is not reliable. Work with a certified business appraiser or your CPA to establish a defensible current value.

- Review or draft your buy-sell agreement. No insurance policy replaces a written legal agreement. Work with a business attorney to confirm the agreement specifies the trigger events, valuation method, and funding mechanism.

- Choose your ownership structure. Decide between cross-purchase and corporate redemption based on the number of partners, your tax situation, and your administrative capacity. Involve both a CPA and an insurance advisor in this decision.

- Select the right policy type. Term life is cost-effective for defined timelines. Permanent life adds cash value and flexibility. Review whole life vs. term life options with an advisor who understands business applications.

- Verify beneficiary designations. Incorrect or outdated beneficiary designations are one of the most common reasons a well-designed plan fails at execution. Confirm that policy ownership and beneficiary assignments match the buy-sell agreement exactly.

- Schedule recurring reviews. Business value changes. Partner circumstances change. Set a calendar reminder to review coverage annually or after any major business event such as a new partner joining, a revenue milestone, or a significant asset acquisition.

Pro Tip: Ask your insurance advisor to run a side-by-side comparison of the death benefit against your most recent business valuation. If the gap is more than 20%, your plan has a coverage shortfall that needs immediate attention.

Comparing buy-sell insurance strategies: cross-purchase vs. corporate redemption

Choosing between cross-purchase and corporate redemption is not purely a preference decision. It carries real tax, legal, and administrative consequences that compound over time as your business grows.

The 2024 U.S. Supreme Court ruling in Connelly v. United States clarified that corporate stock should be valued before redemption, meaning the life insurance proceeds held by the company increase the estate's taxable value. This ruling directly affects corporate redemption structures and may result in a higher estate tax burden for the deceased partner's estate compared to a cross-purchase arrangement.

Cross-purchase agreements give surviving partners a stepped-up tax basis in the shares they acquire, which reduces capital gains taxes if they later sell the business. Corporate redemption does not provide this step-up. For business owners planning an eventual exit or sale, this difference can translate into a significant tax liability.

The tradeoff is administrative complexity. Cross-purchase models increase exponentially in policies as partners increase, requiring robust administration and early planning. A business with two partners needs two policies. A business with four partners needs twelve. At five partners, the number reaches twenty. Many businesses with more than three partners use a trusteed cross-purchase arrangement or switch to corporate redemption specifically to reduce this burden.

Key considerations when choosing your structure:

- Number of current and anticipated future partners

- Whether estate tax exposure is a concern for any partner

- The business entity type (C-corp, S-corp, LLC, or partnership)

- Whether the business has sufficient cash flow to pay premiums at the entity level

Common pitfalls in insuring business partners to ensure your plan won't fail

The most dangerous assumption in partner insurance planning is that a policy purchased years ago still does the job today. Policies bought at a $4M business valuation may be completely inadequate when the business has grown to $16M. The coverage gap becomes a liquidity crisis the moment a partner dies.

The most frequent mistakes business owners make include:

- Failing to update coverage as business value grows. Insurance coverage must track business valuation. A plan that was adequate at founding can be dangerously underfunded within a decade.

- Mismatched beneficiary designations. If the buy-sell agreement names the surviving partners as buyers but the policy names the deceased partner's spouse as beneficiary, the plan collapses. Designations must mirror the legal agreement.

- Confusing key person insurance with buy-sell funding. Key person insurance does not replace the legal buyout agreement. Using it as a substitute leaves the ownership transfer legally unresolved.

- Underestimating policy administration in cross-purchase structures. With multiple partners, tracking premium payments, ownership records, and policy renewals across many policies creates real operational risk.

- Ignoring tax planning at setup. Ownership and beneficiary decisions made at purchase determine tax outcomes at death. Changing them later is often costly or impossible.

"Regular review and alignment of insurance coverage with business valuation is critical to avoid liquidity gaps at partner death." — Garza Law

Pro Tip: Conduct a seasonal audit of your insurance arrangements every fall. Confirm that all policies are active, premiums are current, beneficiary designations are accurate, and coverage amounts reflect your current business valuation.

Key takeaways

Insuring a business partner with life insurance requires a coordinated system of legal agreements, correctly structured policies, and regularly updated valuations to prevent a partner's death from becoming a financial crisis.

| Point | Details |

|---|---|

| Buy-sell agreements need life insurance | Life insurance creates the liquidity to fund partner buyouts without liquidating business assets. |

| Cross-purchase vs. redemption matters | Your choice affects policy count, tax basis, estate tax exposure, and administrative complexity. |

| Key person insurance is not a substitute | It offsets operational losses but does not legally transfer ownership. Both tools serve different roles. |

| Coverage must track business value | A policy sized to a $4M valuation fails when the business is worth $16M. Review coverage regularly. |

| Tax planning starts at setup | Policy ownership and beneficiary designations determine tax outcomes and must be set correctly from day one. |

Why most partner insurance plans fail before they're ever tested

I have seen business owners spend real money on life insurance policies and still end up in a crisis when a partner dies. The policies existed. The premiums were paid. But the buy-sell agreement was never updated after a new partner joined, or the beneficiary designation still named an ex-spouse, or the coverage amount reflected a business valuation from 2014. The plan looked complete on paper and failed completely in practice.

The uncomfortable truth is that insuring a business partner is not a one-time transaction. It is an ongoing system. Legal agreements, insurance ownership, policy terms, and beneficiary choices must all align for a buyout to execute cleanly. Any one of those elements drifting out of sync can unravel the entire arrangement at the worst possible moment.

What I tell every business owner I work with is this: test your plan before you need it. Walk through the exact sequence of events that would occur if your partner died tomorrow. Who receives the death benefit? Does that match who is obligated to buy the shares under the agreement? Is the coverage amount sufficient to fund the buyout at today's valuation? If you cannot answer all three questions with confidence, the plan needs work.

The other mistake I see regularly is treating key person insurance and buy-sell funding as interchangeable. They solve different problems. Key person coverage stabilizes the business operationally. The buy-sell agreement resolves ownership legally. You need both, and they need to be coordinated. Explore key person insurance basics if you are unclear on where one ends and the other begins.

Balancing cost, coverage, and complexity is real work. But the cost of getting it wrong is far higher than the cost of getting it right.

— Asa

How Premier72 helps you protect your business partners

Premier72 works with established business owners to build partner protection strategies that hold up under real-world conditions, not just on paper. Whether you need to structure a buy-sell agreement funded by life insurance, evaluate key person coverage for a critical partner, or audit an existing plan for coverage gaps, Premier72 brings together insurance expertise and business advisory experience in one place. The goal is a plan where the legal agreements, policy ownership, beneficiary designations, and coverage amounts all align with your current business value and succession goals. If you are ready to protect what you have built, start with Premier72 and get a clear picture of where your plan stands today.

FAQ

What is the difference between buy-sell insurance and key person insurance?

Buy-sell insurance funds the legal transfer of a deceased partner's ownership interest to surviving partners or the business entity. Key person insurance pays the business to offset operational and financial losses caused by the partner's death, without resolving ownership.

How many life insurance policies does a cross-purchase agreement require?

The number of policies scales with the number of partners. With five owners, a cross-purchase agreement requires twenty separate life insurance policies, since each partner must own a policy on every other partner.

Are life insurance premiums for buy-sell agreements tax-deductible?

No. Life insurance premiums used to fund buy-sell agreements are not tax-deductible. However, the death benefit is generally received tax-free by the policy owner, preserving the full buyout amount.

How often should business partner life insurance coverage be reviewed?

Coverage should be reviewed every two to three years at minimum, and immediately after any significant change in business valuation, partner count, or ownership structure. A policy sized to an outdated valuation creates a dangerous funding gap.

Can a sole proprietor use key person insurance?

Key person insurance is designed for businesses with critical owners or employees whose loss would cause measurable financial harm. Sole proprietors can use it, but the primary application is in partnerships and closely held companies where one person's death directly threatens business continuity.