A personal financial protection plan is a structured strategy that shields your income, assets, and financial future from catastrophic risks like premature death, disability, and unexpected emergencies. For business owners and professionals nearing retirement, this kind of plan goes far beyond a single insurance policy. It combines emergency funds, insurance, and legal protections into a layered defense that keeps decades of wealth-building intact. Industry standards recommend maintaining 3–6 months of living expenses in liquid reserves, pairing that with income replacement insurance, and backing both with legal structures like trusts or LLCs. Without all three layers working together, a single event can unravel a retirement you spent 30 years building.

What is a personal financial protection plan made of?

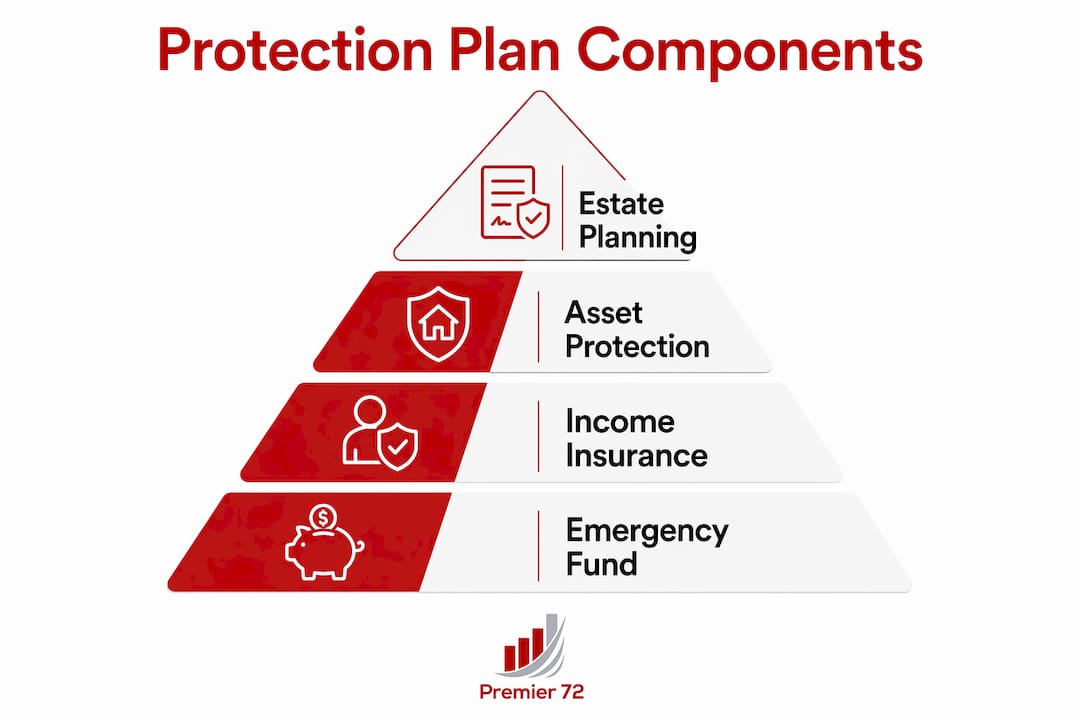

A personal financial protection plan, known in the industry as a personal risk management plan, rests on four core components. Each one addresses a different category of financial exposure. Together, they create a safety net that holds even when multiple risks hit at once.

Emergency fund

An emergency fund is liquid cash set aside to cover short-term disruptions without touching investments or triggering insurance claims. Emergency funds act as the first defense against small, predictable losses, preserving capital and reducing unnecessary insurance costs. The standard target is 3–6 months of living expenses, though business owners often need closer to 6 months because their income is less predictable than a salaried employee's. Keeping this money in a high-yield savings account or money market fund keeps it accessible without sacrificing all growth.

Income replacement insurance

Disability insurance and life insurance both serve income replacement functions, but they protect against different triggers. Disability insurance is undervalued despite the fact that over 25% of 20-year-olds experience a long-term disability before age 67. That statistic means the odds of needing disability coverage are far higher than most owners realize. Life insurance steps in when death removes the primary income source, protecting dependents and business partners from immediate financial collapse.

Asset protection structures

Legal structures like LLCs and irrevocable trusts add a layer of protection that insurance alone cannot provide. LLCs protect personal assets from business liabilities, while trusts can guard inherited wealth from creditors and estate taxes. These structures require legal advice and often involve trade-offs in control, but they are non-negotiable for owners with significant net worth. Without them, a lawsuit or business failure can reach personal savings, real estate, and retirement accounts directly.

Estate planning documents

Wills, powers of attorney, and healthcare directives complete the plan by ensuring your wishes are legally enforceable. Estate planning protects your family from probate delays and ensures assets transfer to the right people at the right time. Without updated documents, courts decide who gets what, and that process can take years.

| Component | Purpose | Priority level |

|---|---|---|

| Emergency fund | Covers short-term disruptions without liquidating investments | High |

| Disability insurance | Replaces income if illness or injury prevents work | High |

| Life insurance | Protects dependents and business partners from income loss | High |

| Legal structures (LLC, trust) | Shields personal assets from business liabilities and lawsuits | Medium-High |

| Estate planning documents | Ensures assets transfer correctly and efficiently | Medium |

How do protection strategies differ for business owners near retirement?

Business owners face risks that salaried professionals do not. A solo practitioner or small business owner has no employer-sponsored disability plan, no group life insurance, and no HR department managing benefits. Every layer of protection must be built and maintained personally.

Umbrella liability policies provide additional protection for high-net-worth owners against lawsuits that exceed standard home or auto coverage. Professionals like doctors, landlords, and consultants often carry $1 million or more in umbrella coverage because their exposure to liability claims is higher than average. Key person insurance is equally critical for owners whose businesses depend on their continued involvement. If you are the primary revenue driver, your business needs a policy that funds continuity or buyout if you become unable to work.

Balancing insurance costs with retirement income goals requires discipline. American households pay nearly $10,000 annually in insurance premiums across all policies combined. That figure means every coverage decision affects how much capital is available to fund retirement. The goal is not to buy every policy available. The goal is to transfer risks you cannot afford to absorb and self-insure the ones you can.

- Carry umbrella liability coverage of at least $1 million if you own a business or professional practice

- Evaluate key person insurance if your departure would materially harm business revenue

- Use LLCs or S-corps to separate personal and business liability exposure

- Review buy-sell agreements annually to confirm funding aligns with current business value

- Work with a fee-only advisor to align insurance products with your actual risk profile, not a commission-driven product menu

Pro Tip: Fee-only advisors are compensated by you, not by product commissions. That distinction matters enormously when selecting disability or life insurance products, because commission-driven recommendations often favor higher-cost permanent policies over lower-cost term coverage.

What common mistakes should owners avoid in protection planning?

The most expensive mistake is underinsuring disability risk. Income replacement via disability insurance is critical but underutilized, and employer-sponsored plans are often insufficient for business owners who draw income from multiple sources. Most group disability plans cap benefits at 60% of base salary and exclude business distributions entirely. That gap can be devastating if a disability lasts two or more years.

The second common mistake is overpaying for permanent life insurance when term coverage is more appropriate. Term life insurance is often more cost effective than permanent life insurance because of lower premiums and the ability to invest the savings separately. A healthy 30-year-old can secure $500,000 in 20-year term coverage for $25–$35 per month. Permanent policies can cost ten times that amount for the same death benefit.

- Underinsuring disability risk by relying solely on employer group plans

- Choosing permanent life insurance when term coverage meets the actual need

- Neglecting the emergency fund and forcing insurance to cover predictable small losses

- Waiting until after liabilities arise to set up legal protection structures

- Failing to review the plan annually as income, assets, and family circumstances change

Protection planning must be done well before any liabilities arise to be effective. Late planning after a lawsuit is filed or a health diagnosis is made often fails entirely. The time to build the structure is when everything is going well, not when a crisis is already unfolding.

Pro Tip: Schedule a full plan review every year in january or february, before tax season consumes your attention. Use that review to update coverage amounts, confirm beneficiary designations, and verify that legal structures still reflect your current asset picture.

How do you implement and maintain a financial protection plan?

Building a personal risk management plan is a sequential process. Each step builds on the one before it, and skipping steps creates gaps that compound over time.

- Build your emergency fund first. Establish 3–6 months of liquid reserves before purchasing any insurance. This prevents you from filing small claims that raise premiums and keeps your coverage focused on catastrophic losses.

- Assess your income replacement needs. Calculate how much monthly income your household requires if you cannot work. Then purchase disability income insurance that covers at least 60–70% of your gross income, including business distributions.

- Purchase life insurance aligned with your obligations. Identify your dependents, outstanding debts, and business obligations. Select term or permanent coverage based on the duration of those obligations, not on what a product brochure recommends.

- Establish or update estate planning documents. Work with an estate attorney to create or revise your will, trust, power of attorney, and healthcare directive. Confirm that beneficiary designations on all accounts match your estate plan.

- Set up legal protection structures. Consult a business attorney about whether an LLC, S-corp, or irrevocable trust makes sense for your asset profile. These structures take time to establish and must be in place before any liability event occurs.

Maintaining the plan requires the same discipline as building it. Life changes, including business growth, marriage, divorce, and health shifts, all affect your coverage needs. A plan that was right three years ago may leave significant gaps today. Reviewing your plan annually with both a financial advisor and an estate attorney keeps all layers current and coordinated.

- Confirm beneficiary designations on retirement accounts, life insurance, and bank accounts every year

- Adjust disability coverage when your income increases significantly

- Revisit umbrella liability limits after major asset acquisitions

- Update buy-sell agreements when business value changes materially

Key takeaways

A personal financial protection plan works because it layers emergency reserves, income replacement insurance, legal structures, and estate planning into a single coordinated defense against the risks most likely to derail retirement.

| Point | Details |

|---|---|

| Emergency fund is the foundation | Build 3–6 months of liquid reserves before purchasing any insurance coverage. |

| Disability insurance is underused | Over 25% of workers experience long-term disability; most employer plans cover too little. |

| Term life often beats permanent | Lower premiums free up capital to invest separately toward retirement goals. |

| Legal structures protect assets | LLCs and trusts shield personal wealth from business liabilities and creditor claims. |

| Timing is non-negotiable | Protection structures must be in place before any liability or health event arises. |

What I've learned from watching protection plans succeed and fail

I've worked with enough business owners nearing retirement to recognize a pattern. The ones who feel genuinely confident about retirement are not necessarily the wealthiest. They are the ones who built their protection plan early and reviewed it consistently. The ones who struggle are often surprised by how exposed they were, not because they didn't care, but because they assumed the plan they set up ten years ago still fit.

The emotional dimension of this is real. A comprehensive protection plan provides emotional relief that changes how owners make decisions. When you know your income is protected, your assets are shielded, and your family is covered, you stop making fear-based choices. You can sell the business at the right time instead of holding on too long out of anxiety. You can retire when you are ready instead of when you are forced to.

The biggest misconception I encounter is that insurance alone constitutes a protection plan. Insurance is one tool. Without the emergency fund to absorb small losses, the legal structures to block liability exposure, and the estate documents to direct asset transfer, insurance is just a partial answer. The plan only works when all four layers are in place and coordinated with each other.

My honest recommendation: treat your protection plan the same way you treat your business financials. Review it every year. Adjust it when circumstances change. And build it before you need it, because by the time you need it, it is too late to build it right.

— Asa

How Premier72 helps you build a protection plan that lasts

Protecting your income and assets as you approach retirement requires more than a single policy or a one-time conversation. It requires a coordinated plan built around your specific business structure, income sources, and retirement timeline.

Premier72 works with business owners and professionals to design protection strategies that combine life insurance, disability coverage, annuities, and legal planning into a single, coordinated approach. Whether you need to evaluate key person coverage, fund a buy-sell agreement, or build a retirement income strategy that holds up under real-world pressure, Premier72 brings the expertise to get it right. Visit premier72.com to schedule a consultation and start building a plan that protects everything you have worked to create.

FAQ

What is a personal financial protection plan?

A personal financial protection plan is a coordinated strategy that combines emergency reserves, income replacement insurance, legal asset protection structures, and estate planning documents to shield your income and wealth from catastrophic risks.

How much should I keep in an emergency fund?

Financial experts recommend 3–6 months of living expenses in liquid reserves. Business owners with variable income should target the higher end of that range.

Is disability insurance really necessary for business owners?

Disability insurance is critical for business owners because employer-sponsored group plans rarely cover business distributions, and over 25% of workers experience a long-term disability before retirement age.

What is the difference between term and permanent life insurance?

Term life insurance provides coverage for a fixed period at lower premiums, while permanent life insurance builds cash value at a significantly higher cost. For most business owners, term coverage is more cost effective unless there is a specific estate planning need for permanent coverage.

When should I set up legal asset protection structures?

Legal structures like LLCs and trusts must be established before any liability event arises. Setting them up after a lawsuit is filed or a creditor claim is made provides little to no protection.