A group life insurance plan is a single insurance contract that covers multiple people under one master policy, typically offered by employers to provide basic life protection for their workforce. Unlike individual policies, group coverage requires no medical exam for basic amounts and often costs employees nothing out of pocket. For business owners, it serves as both a protection tool and a retention asset. For employees, it can be the only life insurance they have access to, especially those with pre-existing health conditions.

What is a group life insurance plan and how does coverage work?

A group life insurance plan is defined as a master contract held by an employer or organization that extends coverage to eligible members, typically employees, without requiring individual underwriting for basic amounts. Basic coverage ranges from $10,000 to $50,000, with supplemental options reaching up to $500,000. That range reflects the plan's dual purpose: provide a guaranteed floor of protection while allowing employees to buy more if they need it.

The most common form is group term life insurance. It pays a death benefit to the employee's named beneficiary if the employee dies while covered under the plan. Coverage is temporary and tied directly to employment status.

Here is how the coverage mechanics work in practice:

- The employer holds the master policy. The insurer issues one contract to the employer, not to each employee individually. The employer acts as the policyholder and administrator.

- Eligibility triggers coverage. Most employees become eligible immediately upon hire or after a short waiting period, often 30 to 90 days. No action is required for basic coverage.

- Coverage amounts follow a formula. Employers typically set coverage at one or two times the employee's annual salary, or at a flat dollar amount like $25,000 or $50,000.

- Supplemental coverage is available by payroll deduction. Employees who want more than the basic amount can elect additional coverage, paid through automatic payroll deductions at discounted group rates.

- Higher supplemental amounts may require health information. Simplified underwriting applies when employees request coverage above guaranteed issue limits, meaning they answer health questions but typically skip a full medical exam.

- Coverage ends when employment ends. Employees who leave the company lose their group coverage. A conversion window of approximately 30 days exists to convert to an individual policy.

Pro Tip: If you leave a job, request conversion to an individual policy within 30 days. Missing that window means losing your guaranteed issue status, and reapplying on the open market may require full medical underwriting.

What are the benefits and limitations of group life insurance?

Group life insurance delivers real value, but it comes with structural limits every employee and business owner should understand before relying on it as a complete solution.

Key benefits

- No cost for basic coverage. Basic group life insurance is often fully funded by the employer, meaning employees receive a meaningful death benefit at zero personal cost.

- Guaranteed issue access. Employees receive basic coverage regardless of their health history. This makes group plans a critical lifeline for people with pre-existing conditions who might not qualify for individual coverage.

- Lower premiums for supplemental coverage. Group rates pool risk across many people, which keeps per-person costs lower than comparable individual policies.

- Simple enrollment. There is no lengthy application process for basic coverage. Employees are automatically enrolled when they become eligible.

- Payroll deduction convenience. Supplemental premiums come out of each paycheck automatically, removing the risk of a lapsed policy due to a missed payment.

Key limitations

- Coverage amounts are often insufficient alone. A benefit equal to one or two times salary rarely covers a family's full financial needs, especially with a mortgage, dependents, or significant debt. Group life insurance is best viewed as a foundational safety net, not a complete solution.

- Coverage is not portable. When an employee leaves the company, coverage ends. The policy belongs to the employer, not the employee.

- Conversion is costly. Converted policies typically carry higher premiums than standard individual market rates, making them a less attractive long-term option for most people.

- Supplemental coverage may require health disclosure. Employees who want more than the guaranteed issue amount may face health questionnaires that could limit their eligibility.

Pro Tip: Treat your group life coverage as a starting point, not a finish line. Run a quick needs analysis using your income, debts, and dependents to see how much additional individual coverage makes sense for your situation.

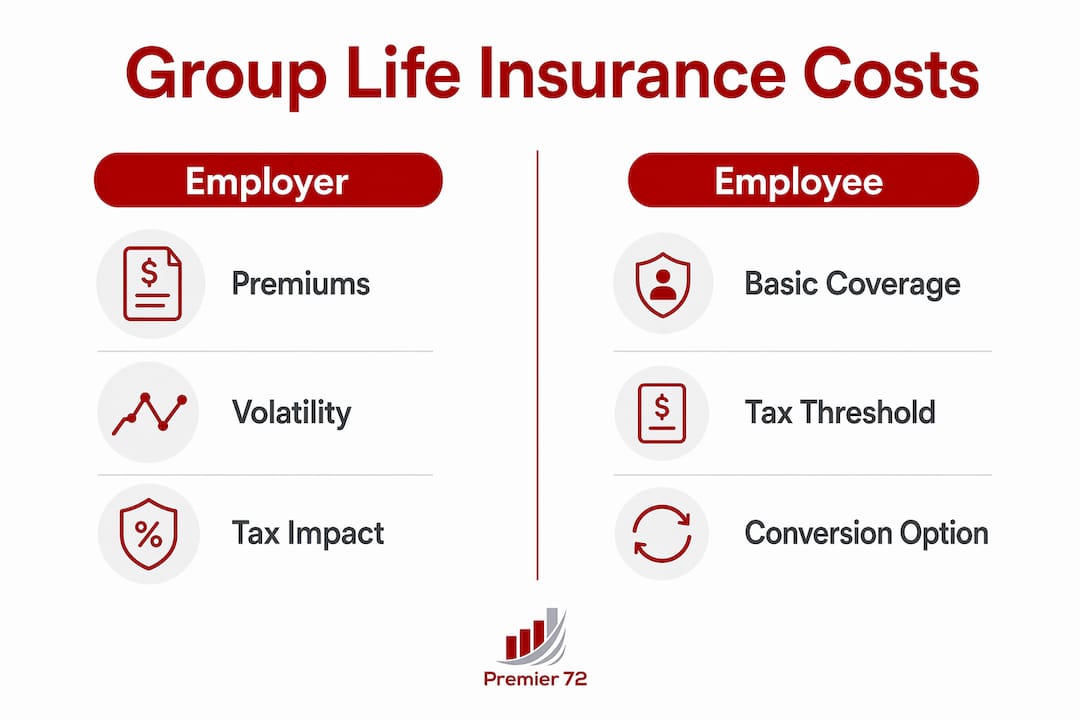

How much does group life insurance cost for employers and employees?

Cost structure in group life insurance differs significantly depending on whether you are the employer or the employee.

| Cost Element | Employer Perspective | Employee Perspective |

|---|---|---|

| Basic coverage premiums | Typically fully funded by the employer | Usually free to the employee |

| Supplemental coverage | May subsidize or pass cost to employee | Paid via payroll deduction at group rates |

| Tax treatment | Premiums are generally a deductible business expense | First $50,000 of coverage is tax-free |

| Coverage above $50,000 | No direct tax impact on employer | Imputed income tax may apply to employee |

| Premium stability | Premiums can increase with claims or aging workforce | Rates may rise at renewal |

The tax rule on the $50,000 threshold is one most employees overlook. The IRS treats employer-paid premiums for coverage above $50,000 as imputed income, meaning the employee owes income tax on the value of that excess coverage. For most employees with modest coverage levels, this is a minor issue. For higher earners with salary-based coverage, it can add up.

For employers, the bigger cost risk is premium volatility. Group policy premiums are not fixed indefinitely. As the workforce ages or claims increase, the insurer can adjust rates at renewal. A company that hired mostly young employees a decade ago may face meaningfully higher premiums today. Business owners need to budget for this variability and review their plan annually.

For tax-related questions about how group life premiums affect your business filings, a resource like SmileTax can help clarify the employer-side implications without the anxiety of sorting through IRS publications alone.

What should you consider before choosing a group life insurance plan?

Choosing or offering a group life insurance plan requires more than picking a coverage amount. Both individuals and business owners need to think through several practical factors before committing.

- Assess whether the coverage amount actually fits your needs. A flat $25,000 benefit or one times salary rarely replaces income for a family with a mortgage and young children. Use a life insurance needs calculator to find your real number, then decide how much supplemental coverage to add.

- Understand the conversion and portability rules before you need them. Employees who rely solely on group coverage and then change jobs or get laid off can find themselves uninsured. Knowing the 30-day conversion window ahead of time prevents a costly gap.

- Factor in your health status when evaluating supplemental options. If you have a pre-existing condition, the guaranteed issue portion of your group plan may be the most affordable coverage you can access. Maximize it before looking elsewhere.

- Review the plan periodically, not just at open enrollment. Life changes, including marriage, a new child, a home purchase, or a salary increase, can make your current coverage level outdated within a year.

- Business owners should treat group life as part of a broader benefits strategy. Employers who keep plans competitive and regularly review benefit levels retain employees more effectively. An outdated plan signals to employees that the company is not invested in their wellbeing.

- Individuals should pair group coverage with an individual policy. Group life insurance and individual life insurance policy types serve different purposes. Individual policies travel with you regardless of employment and can be structured to meet long-term financial goals.

Business owners specifically should also think about how group life fits within their larger continuity and legacy planning. A well-structured benefits package, including group life, key person coverage, and buy-sell funding, protects both the business and the people who depend on it. Premier72 works with business owners to build that kind of integrated protection strategy.

Key Takeaways

Group life insurance is a foundational employee benefit that provides guaranteed, low-cost coverage under one master contract, but it rarely replaces the need for individual life insurance.

| Point | Details |

|---|---|

| Core definition | A single master contract covers multiple employees, often with no medical exam required for basic amounts. |

| Coverage limits | Basic coverage typically equals 1–2 times salary; supplemental options can extend protection significantly. |

| Portability gap | Coverage ends when employment ends; conversion to individual coverage must happen within about 30 days. |

| Tax threshold | Employer-paid coverage above $50,000 creates taxable imputed income for the employee. |

| Business owner role | Employers should review plan competitiveness annually to maintain retention value and manage premium volatility. |

Group life insurance is a floor, not a ceiling

I have worked with enough business owners and families to know that group life insurance is one of the most misunderstood benefits in the American workplace. Employees assume it is enough. Business owners assume it is a checkbox. Neither is quite right.

The guaranteed issue feature is genuinely valuable, especially for employees who have been declined for individual coverage due to health history. For those people, a group plan is not just convenient. It may be the only life insurance they can realistically access. That matters enormously.

But I have also seen families left in a difficult position when an employee dies with only one times salary in coverage and a mortgage that dwarfs that amount. Group life insurance was never designed to be a complete financial plan. It was designed to be a starting point.

For business owners, the real opportunity is using group life as part of a business legacy and continuity strategy that includes key person coverage, buy-sell agreements, and individual policies for owners themselves. Group life covers your employees. The rest of the structure protects your business. Both matter, and they work best when planned together.

The employees who come out ahead are the ones who understand what their group plan covers, fill the gaps with individual coverage, and revisit both every time their life changes. That is not complicated. It just requires knowing where to start.

— Asa

How Premier72 helps business owners build stronger benefit plans

Business owners who want to offer group life insurance as part of a competitive benefit package often face the same challenge: knowing whether the plan they have is actually working for their employees and their bottom line.

Premier72 works with established business owners to evaluate, structure, and maintain employee benefit strategies that support retention, protect key people, and align with long-term exit and succession goals. That includes reviewing group life insurance coverage levels, identifying gaps, and connecting the right protection tools to the right business objectives. If you are building a benefits package that actually retains talent and protects your business, Premier72's advisory team can help you get there with a plan that fits your company's size, budget, and goals.

FAQ

What is the group life insurance definition in simple terms?

A group life insurance plan is a single insurance contract that covers multiple people, typically employees, under one master policy held by an employer. Basic coverage is usually guaranteed without a medical exam.

How does group life insurance work when an employee leaves a job?

Coverage ends when employment ends. Employees have approximately 30 days to convert their group coverage to an individual policy, though converted policies typically carry higher premiums.

Is group life insurance worth it for employees?

Group life insurance is worth having because basic coverage is usually free and guaranteed regardless of health status. It works best as a supplement to, not a replacement for, an individual life insurance policy.

What are the tax implications of group life insurance coverage?

The first $50,000 of employer-paid group life insurance is tax-free for the employee. Coverage above that threshold creates imputed income, which is subject to federal income tax.

Should business owners offer group life insurance to employees?

Group life insurance is a cost-effective employee benefit that supports retention and demonstrates investment in employee wellbeing. Business owners should review plan competitiveness annually to keep benefit levels relevant and premiums manageable.