Permanent life insurance is a policy that covers you for your entire lifetime and builds a cash value account you can access while you are still alive. Unlike term life insurance, which expires after 10, 20, or 30 years, a permanent policy never lapses as long as you keep paying premiums. Insurers like Guardian Life and Mutual of Omaha have built entire product lines around this structure because it solves two problems at once: it protects your family and grows a financial asset simultaneously. The cash value inside the policy grows tax-deferred, meaning you pay no annual taxes on the gains while they remain inside the policy.

What is permanent life insurance and how does it work?

Every premium payment you make does two jobs at once. Each premium funds both the cost of your death benefit and a separate cash value account that accumulates over time. Think of it as paying your insurance bill and making a deposit into a savings account in the same transaction.

Here is how the mechanics unfold over the life of a policy:

- You pay a premium. The insurer deducts the cost of insurance, which covers the death benefit, and credits the remainder to your cash value account.

- Cash value grows tax-deferred. The account earns interest or investment returns depending on the policy type, and you owe no income tax on those gains while they stay inside the policy.

- You can borrow against the cash value. Policy loans use cash value as collateral. The insurer charges interest on the loan, and if you never repay it, the outstanding balance is deducted from your death benefit when you die.

- Withdrawals are also possible. Unlike loans, withdrawals permanently reduce your cash value and death benefit, so they require careful planning.

- The death benefit pays out tax-free. When you die, your beneficiaries receive the face amount of the policy, minus any unpaid loans.

Pro Tip: Never treat a policy loan as free money. Interest accrues whether you pay it or not, and a large unpaid balance can cause your policy to lapse entirely, leaving your family without coverage.

Policy performance differences mean two permanent policies in the same category can produce very different outcomes depending on the crediting method, premium structure, and loan mechanics. Reading the policy illustration carefully before you sign is not optional.

What are the main types of permanent life insurance?

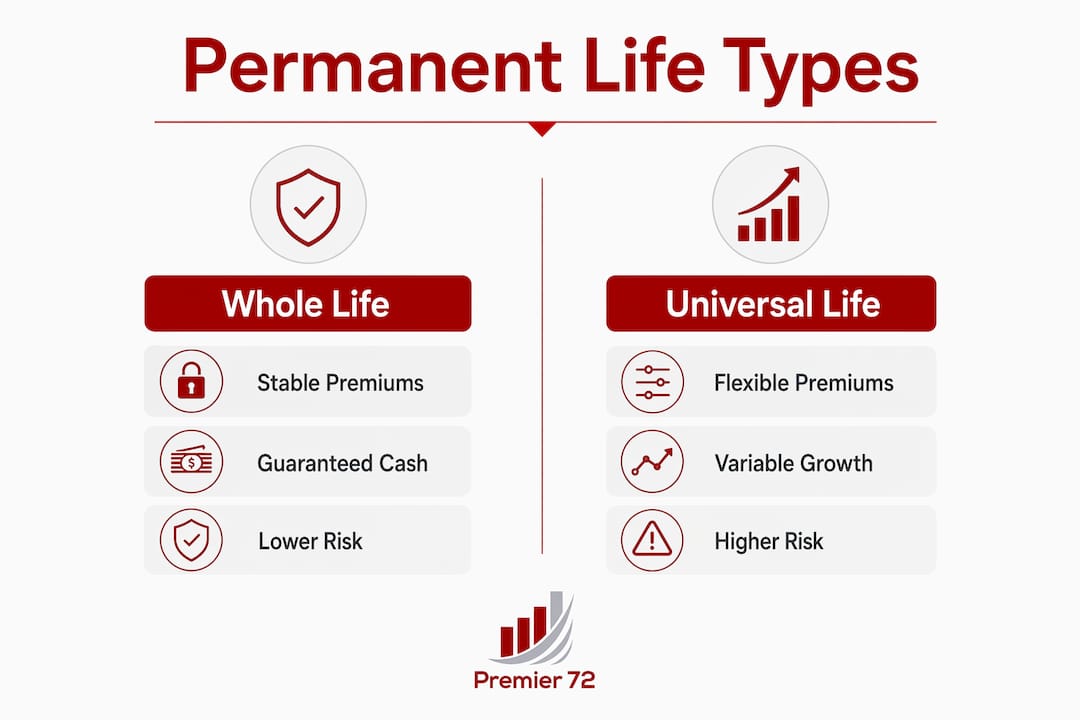

Guardian Life identifies whole and universal life as the two primary categories under permanent life insurance, but the family of products is broader than that. Each type trades off predictability, flexibility, and growth potential differently.

- Whole life insurance offers guaranteed premiums that never change, a guaranteed death benefit, and a cash value that grows at a fixed rate set by the insurer. It is the most predictable option and the most expensive per dollar of coverage.

- Universal life insurance gives you flexible premiums and a death benefit you can adjust within limits. Cash value growth is tied to current interest rates, which means it can rise or fall with the market environment.

- Indexed universal life (IUL) links cash value growth to a stock market index like the S&P 500, with a floor that protects you from losses and a cap that limits your upside. It offers more growth potential than traditional universal life without direct market exposure.

- Variable universal life (VUL) lets you invest the cash value in sub-accounts similar to mutual funds. Returns are not guaranteed, so this option carries the most risk and requires the most active management.

| Policy type | Premium flexibility | Cash value growth | Risk level | Best for |

|---|---|---|---|---|

| Whole life | Fixed | Guaranteed, slow | Low | Predictability seekers |

| Universal life | Flexible | Interest-rate based | Low to moderate | Budget flexibility |

| Indexed universal life | Flexible | Index-linked, floored | Moderate | Growth with protection |

| Variable universal life | Flexible | Market-based | High | Experienced investors |

Choosing between these types comes down to your financial goals and your tolerance for variability. If you want certainty above all else, whole life insurance explained simply is this: you pay a fixed amount, you get a guaranteed return, and the policy never surprises you. If you want more growth potential and can handle some variability, an IUL or VUL may serve you better. For a side-by-side breakdown of cost and structure, the whole life vs term life comparison at Premier72 is worth reading before you decide.

What are the benefits and drawbacks of permanent life insurance?

Permanent life insurance benefits are real and substantial, but they come with trade-offs that every buyer needs to understand before committing.

The core advantages:

- Lifelong coverage. The death benefit is guaranteed as long as premiums are paid. Your family does not face a coverage gap because a term policy expired.

- Tax-deferred cash value growth. The account inside your policy compounds without annual tax drag, which is a meaningful advantage over a taxable savings account over decades.

- Access to funds during your lifetime. You can borrow or withdraw from cash value for retirement income, emergencies, or major expenses without triggering a taxable event in most cases.

- Estate planning utility. The death benefit passes to beneficiaries income-tax-free, making permanent policies a practical tool for transferring wealth across generations.

The real drawbacks:

- Higher premiums. Permanent life insurance costs more than term life because it includes lifelong coverage and a cash value component. A 40-year-old in good health might pay three to five times more for a permanent policy than for a comparable term policy.

- Complexity. Universal life, IUL, and VUL policies require ongoing attention. Underfunding premiums or letting loan balances grow unchecked can cause the policy to lapse.

- Slow early growth. Cash value builds slowly in the early years because a larger share of each premium goes toward the cost of insurance. The financial benefit of the cash value component becomes meaningful only after a decade or more.

Pro Tip: If you are comparing permanent vs term life insurance purely on cost, term will always win in the short run. The question is whether the lifelong coverage and cash value justify the higher premium for your specific situation.

Unmanaged loan balances increase lapse risk and can terminate coverage at exactly the wrong time. Reviewing your policy annually with an advisor is not excessive caution. It is standard practice for anyone holding a permanent policy.

How permanent life insurance fits into long-term financial planning

Permanent life insurance is not just a death benefit. For families and business owners with a long time horizon, it functions as a financial asset that can be deployed strategically. Here are the most practical applications:

- Supplementing retirement income. Cash value accumulated over 20 or 30 years can be accessed through loans or withdrawals to supplement Social Security or other retirement income. Because cash value serves as a dual-purpose tool, it provides both protection and a tax-advantaged savings vehicle in a single product.

- Covering emergencies without disrupting investments. A policy loan lets you access liquidity without selling stocks or tapping a 401(k), which avoids triggering taxes and preserving your investment portfolio during market downturns.

- Funding a buy-sell agreement. Business owners often use permanent policies to fund buy-sell agreements, ensuring a partner's share can be purchased if one owner dies. This keeps the business intact and the family financially whole.

- Building generational wealth. The income-tax-free death benefit transfers wealth to the next generation without the friction of probate or capital gains taxes. Families with estate planning goals often hold permanent policies specifically for this purpose.

- Key person coverage for businesses. A permanent policy on a key employee or owner protects the company from financial disruption if that person dies, while the cash value builds as a business asset on the balance sheet.

For adults in their 50s and 60s, the cash value mechanics of permanent policies become especially relevant as retirement approaches. The ability to draw on a policy without triggering taxable income can make a meaningful difference in retirement cash flow planning. Permanent life insurance also integrates naturally with other assets when you treat it as a retirement income asset rather than just a protection product.

Key takeaways

Permanent life insurance is the only life insurance structure that provides both guaranteed lifelong coverage and a tax-deferred cash value account you can access during your lifetime.

| Point | Details |

|---|---|

| Lifelong coverage guaranteed | The death benefit never expires as long as premiums are paid, unlike term policies. |

| Cash value grows tax-deferred | Gains inside the policy compound without annual taxation, improving long-term accumulation. |

| Loan risk requires management | Unpaid policy loans reduce the death benefit and can cause the policy to lapse if ignored. |

| Multiple policy types exist | Whole life, universal life, IUL, and VUL each offer different trade-offs in cost and growth. |

| Fits retirement and legacy planning | Cash value and death benefits serve as financial tools beyond simple family protection. |

Why I think most families underestimate what they are buying

Most people who buy permanent life insurance think of it as expensive term insurance with a savings account attached. That framing undersells it and sets up disappointment when the cash value does not perform like a brokerage account in year three.

What I have seen working with business owners and families is that permanent life insurance rewards patience and punishes impatience. The families who get the most from these policies are the ones who bought them with a 20-year horizon in mind, reviewed them annually, and never treated a policy loan as a windfall. The ones who struggled bought the policy for the wrong reason, stopped paying attention, and discovered a lapse notice when they could least afford one.

Lapse risk and performance sensitivity vary significantly by policy type and the assumptions baked into the original illustration. An illustration showing strong performance at a 6% crediting rate looks very different if the actual rate averages 4%. That gap compounds over decades. The honest conversation to have with any advisor is: what does this policy look like under conservative assumptions, not optimistic ones?

My advice is simple. If you cannot commit to the premium for at least 10 to 15 years, a permanent policy is not the right tool right now. If you can, and if you have a genuine need for lifelong coverage, estate planning, or tax-advantaged accumulation, permanent life insurance is one of the few financial products that genuinely does multiple jobs well. The key is going in with clear eyes about cost, complexity, and the ongoing attention these policies require.

— Asa

How Premier72 helps you plan with permanent life insurance

Premier72 works with business owners, professionals, and families who need more than a policy. They need a strategy. Whether you are looking at permanent life insurance for family protection, retirement income, key person coverage, or buy-sell funding, Premier72 integrates life insurance into a broader financial plan that accounts for your business, your goals, and your timeline. The team at Premier72 brings the same rigor to insurance planning that they apply to business exit readiness and succession strategy. If you want to understand how a permanent policy fits your specific situation, a conversation with Premier72 is the right starting point.

FAQ

What does permanent life insurance cover?

Permanent life insurance covers your entire lifetime as long as premiums are paid, providing a tax-free death benefit to your beneficiaries plus a cash value account you can access during your lifetime.

How is permanent life insurance different from term life?

Term life insurance covers a fixed period, such as 20 or 30 years, and has no cash value. Permanent life insurance lasts your entire life and builds cash value that you can borrow against or withdraw from while alive.

Can I borrow from my permanent life insurance policy?

Yes. Policy loans use your cash value as collateral, but unpaid loans accrue interest and reduce your death benefit. If the loan balance grows too large relative to the cash value, the policy can lapse.

Is permanent life insurance worth the higher cost?

For families with long-term coverage needs, estate planning goals, or a desire for tax-deferred accumulation, the higher premium is often justified. For someone who only needs coverage for a specific period, term life is the more cost-effective choice.

What is the best type of permanent life insurance for families?

Whole life insurance is the most straightforward option for families who want guaranteed premiums and predictable cash value growth. Indexed universal life suits families who want more growth potential and can accept some variability in returns.