Cash value life insurance is defined as permanent life insurance that combines a death benefit with a tax-deferred savings component you can access during your lifetime. Unlike term policies that expire after a set period, cash value coverage lasts your entire life as long as premiums are paid. Sources including NerdWallet, Investopedia, and Northwestern Mutual consistently describe it as a long-term financial tool built around protection first and savings second. Premiums run 5 to 15 times higher than comparable term coverage, which is the trade-off for lifetime coverage and a growing cash reserve. Understanding what you are paying for, and why, is the starting point for deciding whether this type of policy fits your retirement and wealth preservation goals.

What is cash value life insurance and how does it work?

Every premium payment you make splits into three buckets: the cost of insurance, administrative fees, and the cash value account. The insurance cost covers the death benefit your beneficiaries would receive. The remainder funds the cash value, which grows on a tax-deferred basis inside the policy. This structure is what separates permanent life insurance from term coverage, which collects premiums purely for protection with no savings element.

The cash value grows at a rate that depends on the policy type. Whole life policies typically guarantee 1 to 4% annually, with potential dividends from mutual insurers like Northwestern Mutual. Indexed universal life ties growth to a market index such as the S&P 500, with a floor that protects against losses. Variable life allows you to invest in subaccounts similar to mutual funds, which creates higher growth potential alongside real market risk.

Once your cash value builds, you can access it three ways:

- Policy loans: Borrow against the cash value without a credit check. The loan accrues interest, and if total loans exceed cash value, the policy lapses and triggers a taxable event.

- Withdrawals: Take money directly from the cash value. Withdrawals reduce the death benefit dollar for dollar and may create a tax liability if they exceed your total premium payments.

- Premium offsets: Use accumulated cash value to cover future premium payments, which can reduce out-of-pocket costs in retirement.

Pro Tip: Cash value accumulation is slow in the first three to five years because most early premiums go toward commissions, fees, and surrender charges. Surrendering a policy early almost always results in a financial loss.

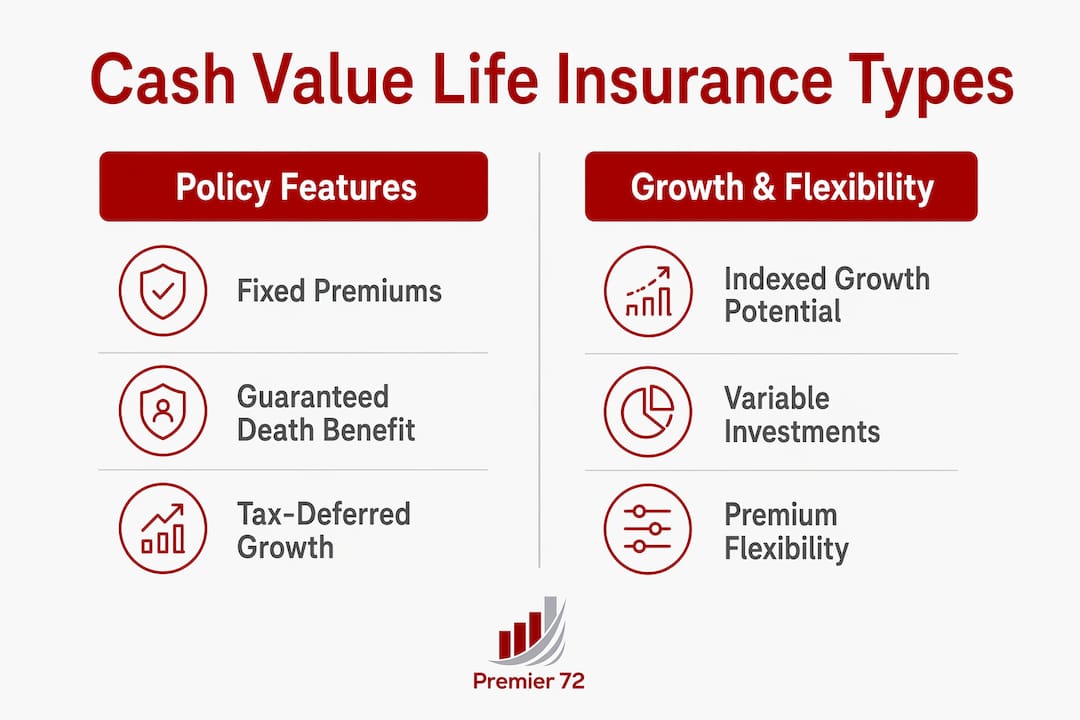

What are the main types of cash value life insurance?

The three primary forms of cash value coverage differ in how the savings component grows, how much flexibility you have with premiums, and how much risk you carry.

| Policy type | Premium flexibility | Cash value growth | Risk level |

|---|---|---|---|

| Whole life | Fixed | Guaranteed 1 to 4% plus possible dividends | Low |

| Indexed universal life | Flexible | Linked to a market index with a floor | Moderate |

| Variable life | Fixed or flexible | Investment subaccounts, market-driven | High |

Whole life insurance is the most straightforward option. Premiums are fixed for life, the death benefit is guaranteed, and the cash value grows at a contractually guaranteed rate. Mutual insurers can also pay non-guaranteed dividends, which policyholders can use to buy additional coverage or increase cash value. The predictability makes whole life a common choice for estate planning and legacy transfer.

Indexed universal life (IUL) links cash value growth to an index like the S&P 500 but caps your upside and floors your downside, typically at 0%. You will not lose cash value in a down market, but you also will not capture the full index return in a strong year. IUL policies also allow flexible premium payments, which suits business owners whose income fluctuates.

Variable life insurance gives you direct control over how the cash value is invested through subaccounts. Returns can significantly outpace whole life or IUL in a bull market, but losses are real and can erode the policy's foundation. Variable policies carry the most complexity and require the most active management of the three types.

How does cash value life insurance compare to term life?

Term life insurance is temporary coverage purchased for a defined period, typically 10, 20, or 30 years, with no savings component. It is the lower-cost option for pure income replacement. A healthy 40-year-old might pay $30 to $50 per month for a $500,000 20-year term policy. The equivalent permanent policy could cost $300 to $500 per month or more.

The core differences come down to purpose and time horizon:

- Term life covers a specific financial obligation, such as a mortgage or income replacement during working years.

- Cash value policies provide lifelong coverage and savings that can serve estate planning, retirement income, and legacy transfer goals.

- Term has no residual value when it expires. Cash value policies build an asset you can access or pass on.

- Cash value coverage is better suited to individuals who need permanent protection and have already maximized 401(k) and IRA contributions.

Pro Tip: Before comparing premiums, calculate the total lifetime cost of each option against your specific financial goals. A 30-year term policy may cost far less overall, but it leaves no asset behind and expires before most people die.

The right choice depends on what you need the policy to do. If you need affordable coverage for a defined period, term is the practical answer. If you need permanent protection, tax-advantaged savings, or a vehicle for wealth transfer, a cash value policy earns its higher cost.

What are the benefits and drawbacks of cash value life insurance?

Cash value life insurance delivers real advantages for the right buyer, and real costs for the wrong one. Understanding both sides prevents expensive mistakes.

Benefits:

- Lifetime coverage. The death benefit never expires, which makes it a reliable estate planning tool regardless of when you die.

- Tax-deferred growth. Cash value grows without annual tax liability, and policy loans are generally tax-free as long as the policy stays in force.

- Retirement income flexibility. You can draw on cash value to supplement retirement income, fund a business transition, or cover unexpected expenses without liquidating other assets.

- Estate planning utility. Death benefits pass to beneficiaries income-tax-free, making permanent life insurance a practical tool for wealth transfer across generations.

Drawbacks:

- High premiums. The cost is significantly higher than term coverage, which strains cash flow if your income is inconsistent or your other financial priorities are not yet funded.

- Slow early accumulation. Cash value builds slowly in the first several years due to fees and commissions. Early surrender almost always means a loss.

- Policy lapse risk. As you age, the cost of insurance rises. If loans or poor returns deplete the cash value, premiums can spike or the policy can lapse entirely.

- Lower returns than equities. Internal rates of return on cash value policies tend to trail equity market benchmarks over long periods.

Cash value coverage best suits high-income earners who have already maxed out their 401(k) and IRA contributions and need permanent protection, estate planning, or a tax-advantaged savings vehicle beyond standard retirement accounts. It is not the right primary savings vehicle for most people.

Pro Tip: Before purchasing any cash value policy, consult a fee-only financial advisor who does not earn commissions on insurance sales. The structure of the policy, including loan provisions, cap rates, and surrender schedules, varies widely between carriers and directly affects long-term performance.

Key takeaways

Cash value life insurance works best as a permanent protection and tax-deferred savings tool for high-income earners with long-term estate or retirement planning needs, not as a primary investment vehicle.

| Point | Details |

|---|---|

| Definition | Permanent life insurance combining a death benefit with a tax-deferred savings account. |

| Premium cost | Premiums run 5 to 15 times higher than term life due to savings and administrative costs. |

| Access methods | Cash value can be accessed via loans, withdrawals, or premium offsets, each with different tax implications. |

| Best suited for | High-income earners who have maxed retirement accounts and need permanent coverage or estate planning tools. |

| Key risk | Policy lapse from depleted cash value triggers a taxable event and eliminates the death benefit. |

Why I think most people misread cash value life insurance

Most people who dismiss cash value life insurance do so because they compare it to a brokerage account. That is the wrong comparison. Most people who buy it without understanding it do so because an agent compared it to a savings account. That is also the wrong comparison.

What I have seen working with business owners and families at Premier72 is that cash value life insurance performs exactly as designed when the buyer understands what it is: a permanent protection contract with a liquidity feature attached. The cash value is not the product. The guaranteed death benefit, the tax-free loan access, and the estate transfer mechanism are the product. The cash value is the flexibility layer on top.

Where policies fail is when buyers expect equity-like returns or treat the policy like a checking account. Loans accrue interest. Withdrawals shrink the death benefit. Cash value is not a liquid bank account and treating it like one is how policies lapse at the worst possible time.

The business owners I work with who get the most from these policies are the ones who integrate them into a broader retirement income strategy, not the ones who buy them in isolation. When a cash value policy sits alongside a funded retirement account, a clear exit plan, and a legacy strategy, it does exactly what it promises. That is the context where it earns its premium cost.

— Asa

How Premier72 helps you build a plan around life insurance

If you are a business owner or professional weighing whether a cash value policy belongs in your financial plan, the answer depends on your full picture, not just the policy itself.

Premier72 works with established business owners and families to integrate life insurance into retirement and legacy strategies that actually hold together under pressure. That means looking at your income, your exit timeline, your estate goals, and your existing coverage before recommending anything. Premier72's approach through The Retirement Bank Method™ treats life insurance as one component of a transferable, fundable retirement plan. If you want clarity on whether cash value coverage fits your situation, start with Premier72 and build from a complete picture.

FAQ

What is the difference between cash value and death benefit?

The death benefit is the amount paid to your beneficiaries when you die. The cash value is a separate savings account inside the policy that grows over time and can be accessed while you are alive.

How long does it take for cash value to build up?

Most policies take three to five years before meaningful cash value accumulates because early premiums go primarily toward fees, commissions, and insurance costs. Surrendering a policy in the first few years almost always results in a loss.

Can I lose my cash value life insurance policy?

Yes. If policy loans plus accrued interest exceed the available cash value, the policy lapses. A lapsed policy triggers a taxable event on any gains and eliminates the death benefit entirely.

Is cash value life insurance worth it for retirement planning?

It is worth it for high-income earners who have already maxed out 401(k) and IRA contributions and need permanent coverage, tax-advantaged liquidity, or an estate planning vehicle. For most people focused on basic income replacement, term life combined with dedicated retirement accounts is more cost-effective.

What happens to cash value when you die?

In most policies, the insurer pays the death benefit to your beneficiaries and retains the accumulated cash value. Some policies offer a rider that pays both, but that increases the premium cost.