Income protection insurance is a long-term policy that replaces a portion of your income when illness or injury prevents you from working. Specifically, it replaces 50% to 70% of your gross pre-disability income through regular monthly payments, not a one-time lump sum. Unlike life insurance, which pays out on death, or critical illness cover, which triggers only for listed conditions, income protection activates for any medical reason that stops you from doing your job. For self-employed professionals and business owners without employer sick pay, this distinction is not academic. It is the difference between keeping your business alive and watching it collapse while you recover.

What is income protection insurance and how does it work?

Monthly benefit payments begin after a waiting period called the deferred period, which you select when you take out the policy. Common deferred periods run 4, 8, 13, 26, or 52 weeks. The longer you wait before payments start, the lower your premium. Once payments begin, they continue until you recover and return to work, reach retirement age, or the policy term ends. Coverage typically extends to ages 65 or 70 under full-term policies, though shorter limited-term options exist.

The definition of incapacity written into your policy determines whether you can actually make a claim. Two definitions dominate the market:

- Own occupation: The policy pays if you cannot perform your specific job, even if you could theoretically do a different one. A surgeon who loses fine motor control qualifies, even if she could work as a consultant.

- Any occupation: The policy pays only if you cannot do any work at all. This definition is far more restrictive and significantly harder to claim against.

Own occupation coverage is the industry gold standard. It costs more, but it delivers the protection most people actually need when they buy the policy.

One common misconception is that income protection pays your full salary. Insurers cap payouts at 50% to 70% deliberately, to preserve your financial incentive to return to work. This is called the moral hazard cap, and it applies across virtually every provider in the market.

Pro Tip: Benefits paid from an income protection policy are generally tax-free to the recipient because premiums are paid from post-tax income. That means a 60% income replacement often feels closer to your full take-home pay in practice.

Key features and benefits of income protection plans

The core benefit is straightforward: your living expenses do not stop because your paycheck does. Mortgage payments, utilities, groceries, and business overhead continue regardless of whether you are healthy. An income insurance policy fills that gap with predictable monthly payments rather than forcing you to drain savings or take on debt.

Several features make income protection plans worth examining closely:

- Benefit duration: Full-term policies pay until retirement age, giving you decades of potential coverage from a single policy.

- Index-linking: Many policies increase your benefit in line with inflation, so the payment retains real purchasing power over a 10 or 20-year claim.

- Guaranteed renewability: Once issued, the insurer cannot cancel your policy due to health changes or prior claims, as long as you keep paying premiums. This is a significant structural advantage over annual renewable policies.

- Flexible deferred periods: You control the waiting period, which directly controls your premium cost.

The flexibility on deferred periods deserves special attention. If your employer provides six months of full sick pay, selecting a 26-week deferred period eliminates redundant coverage and cuts your premium meaningfully. The deferred period directly influences premium costs, and aligning it with your existing financial buffers is one of the most practical ways to make coverage affordable without sacrificing protection.

For business owners, the peace-of-mind argument goes beyond personal finances. Owner-dependent businesses often generate revenue only when the owner is present and working. An income protection benefit keeps the owner financially solvent during recovery, which buys time to stabilize operations rather than forcing a rushed sale or closure.

Pro Tip: If you are self-employed with no sick pay buffer, consider a 13-week deferred period rather than the shortest available option. It meaningfully reduces your premium while still covering the period when most savings would be exhausted.

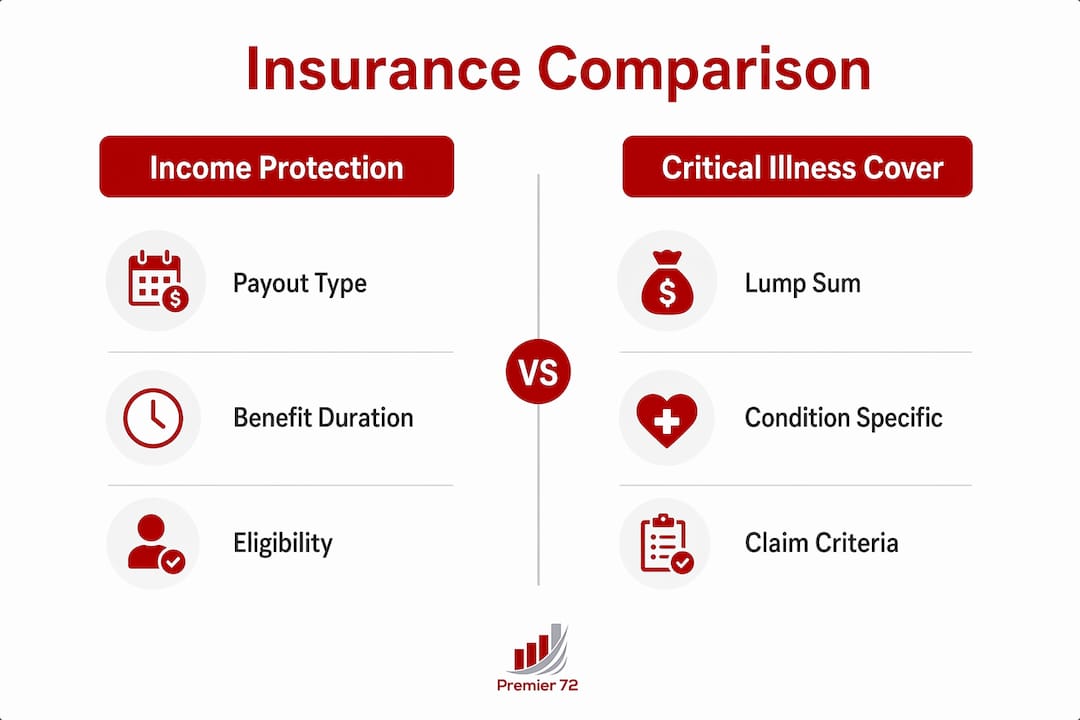

How income protection compares with disability and critical illness insurance

These three products are frequently confused, and the confusion leads to real coverage gaps. The table below clarifies the key differences.

| Feature | Income protection | Critical illness cover | Disability insurance |

|---|---|---|---|

| Payout type | Monthly income | Lump sum | Monthly income or lump sum |

| Trigger | Any illness or injury preventing work | Specific listed conditions only | Disability meeting policy definition |

| Duration | Until recovery or retirement | One-time payment | Varies by policy |

| Covers mental health | Yes, in most policies | Rarely | Varies |

| Best for | Replacing ongoing income | Large one-off expenses | Income replacement, often employer-linked |

Critical illness cover pays a lump sum only for conditions named in the policy, such as cancer, heart attack, or stroke. Income protection covers any disabling illness or injury, including mental health conditions, musculoskeletal problems, and chronic fatigue. That broader trigger is why financial advisors consistently recommend holding both products rather than treating them as substitutes.

Disability insurance overlaps with income protection in purpose but often differs in definition and structure. Many employer-sponsored disability plans use an "any occupation" definition after 24 months, which narrows your claim eligibility over time. Understanding the differences between disability and income protection is particularly important for business owners who may have both types of coverage and assume they are fully protected when gaps exist.

The practical recommendation from most advisors is this: use income protection as your income replacement foundation, use critical illness cover to handle large one-time costs like paying off a mortgage or funding a business transition, and review your critical illness coverage options separately to understand what conditions your policy actually covers.

Who needs income protection, and why business owners cannot afford to skip it

Fewer than 10% of workers carry income protection insurance despite roughly a 20% probability of experiencing long-term work incapacity before retirement. That gap between risk and coverage is one of the most striking mismatches in personal finance.

For employees with generous sick pay and group disability benefits, the case for income protection is strong but not always urgent. For self-employed individuals and business owners, it is non-negotiable. Self-employed individuals have zero entitlement to statutory sick pay, meaning day one of an illness is day one without income.

Business owners face a compounded risk that employees do not:

- Personal income stops immediately when the owner cannot work.

- Business revenue often drops simultaneously because the owner drives sales, client relationships, or production.

- Fixed business costs, including rent, payroll, and loan repayments, continue regardless.

- Without income, the owner may be forced to sell the business under distress conditions rather than on favorable terms.

Income protection coverage addresses the personal income side of this equation. For the business side, key person insurance covers the financial loss a business suffers when a critical individual is unable to work. These two products work together as a coordinated risk management strategy rather than as alternatives.

When selecting an income insurance policy, business owners should evaluate four variables: the benefit amount relative to personal living costs, the deferred period relative to cash reserves, the incapacity definition (own occupation is strongly preferred), and whether the policy is indexed to inflation. Affordable income protection insurance is achievable by extending the deferred period rather than reducing the benefit amount, which preserves the coverage that actually matters.

Key takeaways

Income protection insurance is the most direct financial tool for replacing lost earnings during illness or injury, and its value is highest for those without employer sick pay.

| Point | Details |

|---|---|

| Coverage replaces 50% to 70% of income | Insurers cap payouts deliberately to maintain return-to-work incentives. |

| Own occupation definition is critical | Policies using this definition pay if you cannot do your specific job, not just any job. |

| Deferred period controls premium cost | Align your waiting period with sick pay or savings to avoid paying for redundant coverage. |

| Self-employed face the highest exposure | No statutory sick pay means income stops immediately, making coverage a risk management necessity. |

| Income protection and critical illness are complementary | Each product covers different scenarios; holding both closes the gaps neither covers alone. |

Why I think most people buy income protection too late, or not at all

Most people treat income protection as something to think about later. They have savings, a working spouse, or a vague sense that serious illness happens to other people. I have seen this reasoning fail in practice more times than I can count.

The right time to buy income protection is when you are healthy and your income is growing, not after a diagnosis or a close call. Premiums are priced on your health at the time of application. A 35-year-old in good health pays a fraction of what a 48-year-old with a prior back injury pays for the same benefit. Waiting does not save money. It costs money.

The own occupation versus any occupation distinction is where I see the most painful surprises. People buy the cheaper "any occupation" policy, assume they are covered, and then discover at claim time that because they could theoretically do a desk job, their claim is denied. For specialists, tradespeople, and business owners whose income depends on specific skills, this is not a minor technicality. It is the entire point of the policy.

My honest view is that business owners should treat income protection the same way they treat business insurance or key person coverage: as a non-negotiable operating cost, not a personal luxury. Your ability to generate income is your most valuable asset. Protecting it with an income replacement strategy is not pessimism. It is the same logic you apply to insuring your building, your equipment, and your vehicles.

Start early. Choose own occupation. Match your deferred period to your actual financial runway. Then stop thinking about it and get back to building your business.

— Asa

Protect your income with Premier72's tailored coverage solutions

Premier72 works with business owners, professionals, and families to build insurance strategies that protect income, preserve wealth, and support long-term financial continuity. Whether you are self-employed with no sick pay safety net or a business owner whose personal and company finances are tightly linked, the right income protection plan requires more than an online quote.

Premier72's advisors assess your full financial picture, including existing coverage, business structure, and retirement timeline, to recommend income protection coverage that fits your actual situation. From individual income insurance policies to business continuity planning, Premier72 provides the guidance that turns a complex decision into a clear, confident one. Reach out to Premier72 today to review your options.

FAQ

What does income protection insurance cover?

Income protection insurance covers any illness or injury that prevents you from working, including mental health conditions, musculoskeletal problems, and chronic disease. It pays a monthly benefit of typically 50% to 70% of your pre-disability income until you recover, reach retirement age, or the policy term ends.

Is income protection the same as disability insurance?

Income protection and disability insurance both replace lost income, but they differ in definitions, payout structures, and eligibility triggers. Disability insurance is often employer-linked and may shift to an "any occupation" definition after two years, while income protection policies with own occupation definitions maintain stronger claim eligibility throughout the policy term.

How much does income protection insurance cost?

Premium costs depend on your age, health, occupation, benefit amount, and deferred period. Choosing a longer deferred period, such as 13 or 26 weeks instead of 4 weeks, significantly reduces premiums without reducing the benefit amount you receive once payments begin.

Is income protection insurance worth it for self-employed people?

Self-employed individuals have no access to statutory sick pay, meaning income stops immediately when they cannot work. Income protection is the primary tool for replacing that income, making it one of the most financially justified insurance purchases available to self-employed professionals and business owners.

Can an insurer cancel my income protection policy?

Once issued, an income protection policy cannot be cancelled by the insurer due to changes in your health or claims history, provided you continue paying premiums. This guaranteed renewability gives policyholders long-term security that annual renewable products do not offer.