Overfunded life insurance is defined as a permanent life insurance policy funded with premiums above the minimum required, directing the surplus toward cash value growth rather than death benefit size. The industry term for the core mechanism is the paid-up additions (PUA) rider, which converts extra premium dollars directly into additional paid-up coverage and cash value. Why overfunded life insurance works comes down to one structural fact: 80–90% of premiums flow to cash value in the first seven years when a policy is designed correctly. That ratio is the opposite of a standard whole life policy, where early premiums cover agent commissions and insurance costs first. The result is a tax-deferred, liquid financial asset that grows independently of stock market cycles.

Why overfunded life insurance works: the mechanics

The foundation of this strategy is the premium split. Every whole life policy has a base premium, which covers the core death benefit and insurance costs. An overfunded policy shrinks that base premium and redirects the difference to the PUA rider. Maximizing PUA rider premiums shifts the allocation sharply toward cash value and away from early insurance costs, which is why cash value builds so much faster than in a conventionally funded policy.

The table below shows how premium allocation differs between a standard policy and an overfunded design.

| Policy type | Base premium allocation | PUA allocation | Cash value focus |

|---|---|---|---|

| Standard whole life | High (covers costs first) | Minimal or none | Slow early growth |

| Overfunded whole life | Reduced intentionally | 80–90% of total premium | Rapid early growth |

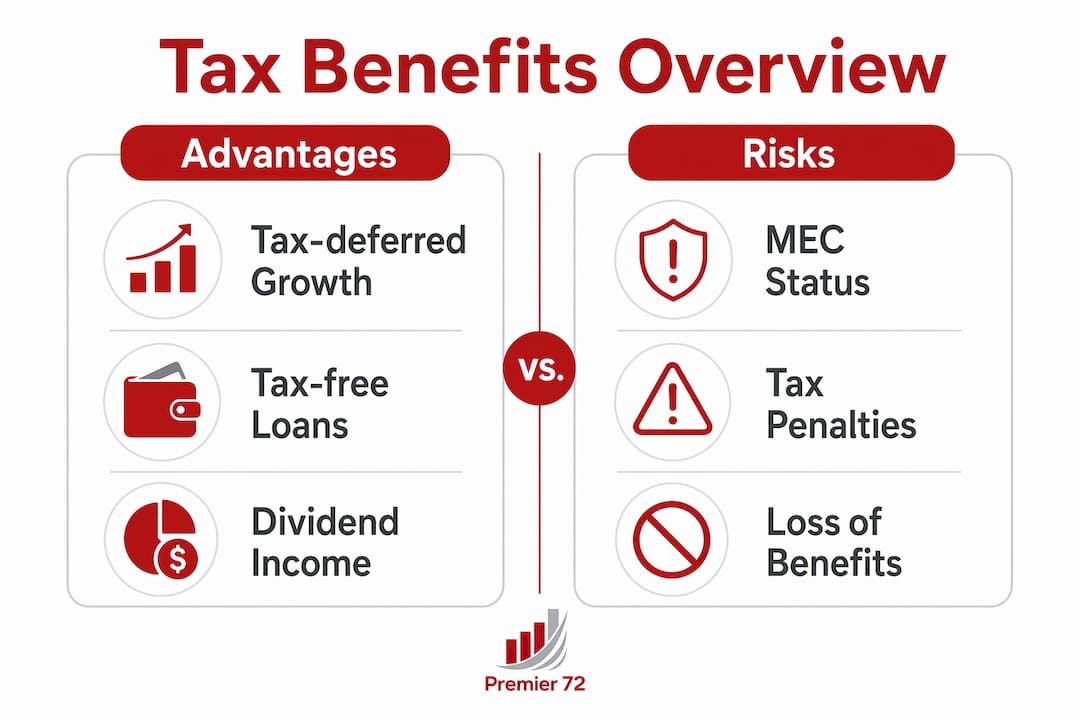

One regulatory constraint governs how far you can push this: the seven-pay test under IRC Section 7702A. If cumulative premiums in the first seven years exceed the IRS-defined limit for that policy, the contract becomes a Modified Endowment Contract (MEC). MEC status strips away the tax-free loan access that makes overfunded policies so useful. Staying below the seven-pay threshold is the single most important design constraint.

Pro Tip: Review premium payments manually each year rather than relying on automated payments. Policy costs and dividend credits shift annually, and an automated payment that was safe last year can push you over the MEC limit this year.

What tax advantages apply to overfunded policies?

Tax-deferred cash value accumulation is the first advantage. Interest, dividends, and gains inside a whole life policy compound without triggering annual income tax. That compounding effect over 10 to 20 years produces a meaningfully larger balance than an equivalent taxable account earning the same rate.

The second advantage is tax-free access. Policyholders can borrow against cash value without triggering income tax, provided the policy is not a MEC. The loan is not a withdrawal. It is a debt against the policy's collateral, so the IRS does not treat it as taxable income. This is the mechanism that makes overfunded policies attractive as a retirement income supplement.

Crossing the MEC line changes everything. Exceeding the seven-pay limit under IRC Section 7702A triggers loss of tax-free loan access and a 10% penalty on withdrawals taken before age 59.5. That penalty mirrors the early-distribution penalty on IRAs and 401(k)s, eliminating one of the strategy's core advantages.

The IRS also enforces a corridor rule on death benefits. The death benefit must equal at least 250% of cash value for insured individuals under age 40, with the required ratio declining at older ages. This rule prevents policies from becoming pure investment vehicles disguised as life insurance.

The benefits and pitfalls of the tax structure break down as follows:

- Tax-deferred growth: Cash value compounds without annual tax drag.

- Tax-free loans: Policy loans are not taxable income if the policy is not a MEC.

- Death benefit: Passes to beneficiaries income-tax-free under IRC Section 101(a).

- MEC penalty: Early withdrawals from a MEC face ordinary income tax plus a 10% penalty.

- Loan interest: Unpaid loan interest capitalizes and can reduce the death benefit if not managed.

Pro Tip: If you accidentally overfund and trigger MEC status, act quickly. Insurers can often reverse MEC classification by refunding the excess premium within approximately 60 days of payment, before IRS filings finalize the status. Contact your insurer immediately, not at year-end.

Is overfunded life insurance a good investment for retirement?

Overfunded life insurance is best used as a complement to qualified retirement plans, not a replacement. Once 401(k) and IRA contribution limits are reached, overfunded policies provide a tax-advantaged channel for additional savings that qualified plans cannot absorb. High-income earners hit those limits earlier in the year and need somewhere else for tax-efficient capital to go.

The liquidity argument is equally strong. Overfunded policies provide non-market-correlated liquidity, meaning cash value does not drop when equity markets fall. A business owner who needs capital during a recession does not have to sell stocks at a loss or take a taxable IRA distribution. The policy loan is available regardless of market conditions, credit scores, or lender approval.

Consider a practical example. A 52-year-old professional maxes out her 401(k) and Roth IRA each year. She funds an overfunded whole life policy with an additional $30,000 annually. By age 65, her cash value has grown tax-deferred and is accessible through policy loans to supplement Social Security and retirement account distributions. She controls the timing and size of those loans, which gives her flexibility to manage taxable income in retirement. That kind of income flexibility is difficult to replicate with market-based accounts.

The core benefits of this strategy for retirement and wealth preservation include:

- Market independence: Cash value grows on a guaranteed schedule, unaffected by equity or bond market swings.

- Flexible income timing: Policy loans can be taken in any amount at any time, with no required minimum distributions.

- Legacy transfer: The death benefit transfers income-tax-free to heirs, making it a wealth transfer tool as well as a retirement asset.

- Creditor protection: In many states, life insurance cash value carries statutory protection from creditors.

- Supplemental capacity: Policies absorb savings beyond qualified plan limits without triggering additional tax exposure.

For a deeper look at how permanent life insurance fits into a retirement income plan, the cash value guide for ages 50–70 covers structuring premiums to maximize early accumulation.

Common risks and how to avoid them

The most common mistake is accidental MEC status. Automated premium payments can inadvertently exceed IRS seven-pay limits when policy costs shift or dividends change. Most policyholders do not realize the problem until tax documents arrive. By then, the cure window may have closed.

A second risk is poor policy design from the start. An overfunded policy requires intentional construction. A policy sold primarily for its death benefit, then later "overfunded" by the owner, will not produce the same cash value efficiency as one designed with a maximized PUA rider from day one. The difference in cash value at year 10 can be substantial.

A third misconception is that overfunding replaces traditional retirement planning. It does not. Overfunded life insurance works best as a layer on top of a funded 401(k), IRA, or pension. Treating it as a primary retirement vehicle ignores its insurance costs and the time required for cash value to outpace those costs.

Follow these steps to manage risk effectively:

- Work with an advisor who specializes in policy design, not just policy sales.

- Review premium payments manually each year and compare them against the current seven-pay limit.

- Add a term life rider to raise the MEC threshold by increasing the death benefit without adding substantial cost, creating more room for PUA contributions.

- Request an in-force illustration annually to confirm cash value trajectory and MEC status.

- If MEC status is triggered accidentally, contact the insurer within 60 days to request a premium refund and status reversal.

Understanding why life insurance functions as a retirement asset helps clarify where overfunded policies fit within a broader financial plan.

Key Takeaways

Overfunded life insurance works because it redirects premium dollars to cash value via PUA riders, producing tax-deferred, liquid wealth that grows independent of market cycles.

| Point | Details |

|---|---|

| Premium split is the core mechanism | Shrinking the base premium and maximizing PUAs directs 80–90% of dollars to cash value in early years. |

| MEC limits define the ceiling | IRC Section 7702A's seven-pay test sets the maximum you can fund without losing tax-free loan access. |

| Tax-free loans are the key benefit | Policy loans are not taxable income, making cash value a flexible, tax-efficient retirement income source. |

| Best used alongside qualified plans | Overfunded policies absorb savings beyond 401(k) and IRA limits, not instead of them. |

| Annual review prevents costly mistakes | Manual premium reviews and in-force illustrations protect MEC status and keep the policy on track. |

What I've learned from watching these policies perform

I've reviewed enough overfunded policies to say with confidence that design quality separates the ones that perform from the ones that disappoint. The policies that underperform almost always share one trait: they were built around a large base premium with a small PUA rider added as an afterthought. The policies that genuinely build wealth flip that ratio from the start.

What surprises most people is how the liquidity works in practice. A client who funded a well-designed policy for 12 years had access to a six-figure cash value balance during a period when their business needed capital. They borrowed against the policy, kept the cash value compounding, and repaid the loan on their own schedule. No bank approval. No market timing. That kind of financial control is rare, and it only exists because the policy was designed correctly from day one.

The other thing I'd emphasize: this strategy rewards patience and penalizes impatience. The first few years of an overfunded policy look modest. The compounding effect becomes visible around years 7 to 10. Clients who exit early because the early numbers look slow miss the point entirely. The whole life insurance benefits that matter most for retirement accumulate over time, not overnight.

My honest recommendation is to treat overfunded life insurance as a precision tool. Used correctly, with the right design and consistent funding, it is one of the most tax-efficient wealth preservation vehicles available to high-income earners. Used carelessly, it is an expensive insurance policy with mediocre returns.

— Asa

How Premier72 structures overfunded policies for lasting results

Premier72 works with business owners, professionals, and families who want to build tax-efficient wealth outside of market-dependent accounts. Designing an overfunded policy correctly requires more than selecting a carrier. It requires structuring the base premium, sizing the PUA rider, and monitoring the seven-pay limit year after year.

Premier72 handles the full design process, from initial premium structuring to annual in-force reviews that keep policies below MEC thresholds. For high-income earners who have maxed out qualified plans and want a stable, tax-advantaged place to build capital, overfunded life insurance is a proven option. Premier72 also connects clients with private banking strategies that complement policy-based wealth building. Schedule a consultation at premier72.com to see how a properly designed policy fits your financial picture.

FAQ

What is overfunded life insurance?

Overfunded life insurance is a permanent life insurance policy funded with premiums above the minimum required, with the surplus directed to a paid-up additions rider to accelerate cash value growth.

How does overfunding a life insurance policy work?

Overfunding works by shrinking the base premium and maximizing contributions to the PUA rider, which directs 80–90% of total premiums to cash value in the first seven years of the policy.

What is a Modified Endowment Contract (MEC)?

A MEC is a life insurance policy that has exceeded the IRS seven-pay test limit under IRC Section 7702A, resulting in loss of tax-free loan access and a 10% penalty on withdrawals before age 59.5.

Can you fix a policy that accidentally becomes a MEC?

Yes. Insurers can often reverse MEC status by refunding the excess premium within approximately 60 days of payment, before the IRS finalizes the classification. Acting quickly is critical.

Who benefits most from overfunded life insurance strategies?

High-income earners who have maxed out 401(k) and IRA contributions benefit most, using overfunded policies to build additional tax-deferred, market-independent capital for retirement income flexibility.