Income replacement planning for business owners is defined as the coordinated set of strategies that sustain your personal income and business cash flow when you retire, become disabled, or lose a key revenue driver. Most owners discover too late that their current financial trajectory covers only 40–50% of their lifestyle needs in retirement. That gap is not a rounding error. It is the difference between a comfortable exit and a forced one. The Allianz Risk Barometer ranks business interruption as the top risk for 31% of businesses, which means income loss is not just a retirement problem. It is an operational threat that can arrive any day. Premier72 works with established business owners to close both gaps through The Retirement Bank Method™, combining insurance, tax-advantaged retirement funding, and succession planning into one coordinated plan.

What are the core components of income replacement planning for business owners?

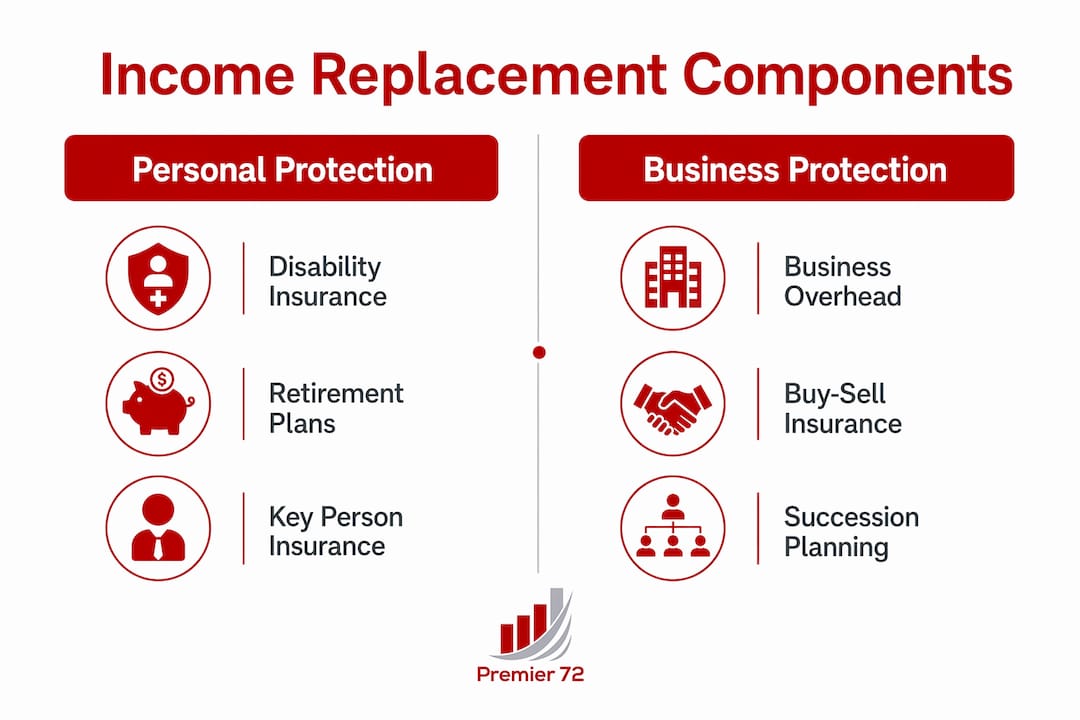

Business owners income protection requires two parallel strategies, not one. The first protects your personal income. The second protects the business itself. Treating them as a single policy is the most common structural mistake owners make, and it leaves critical gaps in both areas.

Personal income protection

Personal income protection insurance replaces a portion of your earned income if illness or injury stops you from working. Unlike employees, business owners receive no sick pay, no employer-funded disability coverage, and no automatic safety net. Your personal earning capacity is your most valuable asset, and it needs coverage that reflects what you actually earn, not a generic group benefit. Disability insurance policies designed for owners typically cover 60–70% of pre-disability income and are owned personally to preserve tax advantages on benefits received.

Business overhead protection

Business overhead expense (BOE) insurance covers fixed business costs, including rent, payroll, and utilities, while you are unable to work. This is a business-owned policy with a distinct purpose from personal disability coverage. Without it, a six-month disability can drain reserves and force layoffs before you recover. Proper ownership alignment of insurance policies, matching who owns the policy to who benefits from it, directly determines tax outcomes and claim success.

Key person and buy-sell insurance

Key person life insurance protects the business against the financial loss caused by the death or disability of a critical contributor, including you. Buy-sell agreements funded by life insurance give co-owners a legal and financial mechanism to transfer ownership without a fire sale. Both policies are business-owned and serve the business, not the individual's household.

Tax-advantaged retirement vehicles

Defined benefit and cash balance plans are the most powerful late-stage retirement tools available to business owners. Funded in the final 3–5 years before retirement, these plans can shelter $100,000 to $300,000 annually for owners aged 50 and older. That level of tax-deferred accumulation is not available through a standard 401(k). Corporate Owned Life Insurance (COLI) adds another layer by funding deferred compensation agreements and retaining key leadership while building tax-advantaged cash value.

Pro Tip: Match every policy's ownership, premium payer, and beneficiary to the specific job that policy performs. A personal disability policy owned by your business can trigger a taxable benefit at the worst possible time.

| Tool | Purpose | Ownership | Tax impact | Primary beneficiary |

|---|---|---|---|---|

| Personal disability insurance | Replaces owner's earned income | Personal | Premiums not deductible; benefits tax-free | Owner/household |

| Business overhead expense insurance | Covers fixed business costs | Business | Premiums deductible; benefits taxable | Business operations |

| Key person life insurance | Offsets loss of critical contributor | Business | Premiums not deductible; proceeds tax-free | Business |

| Buy-sell life insurance | Funds ownership transfer | Business or trust | Varies by structure | Surviving owners |

| Defined benefit/cash balance plan | Accelerates retirement savings | Business/owner | Contributions tax-deductible | Owner at retirement |

| Corporate Owned Life Insurance (COLI) | Funds deferred compensation | Business | Tax-deferred growth | Business/key employees |

How do you calculate your income replacement needs?

Calculating your income replacement target starts with your current lifestyle, not your business revenue. Many owners confuse gross business income with personal financial need, which leads to both over-insuring business risks and under-funding personal retirement.

The calculation follows a reverse-engineering approach. Start with the annual income your household needs to maintain its current standard of living in retirement. Add inflation assumptions, healthcare costs, and any debt obligations that will persist past your exit date. Then subtract guaranteed income sources such as Social Security, rental income, or a business sale proceeds annuity. The remaining number is your replacement gap.

- List all current personal living expenses, including mortgage, insurance, travel, and discretionary spending.

- Estimate annual healthcare costs in retirement, which typically rise significantly after employer coverage ends.

- Project Social Security benefits using your SSA statement or the SSA online estimator.

- Identify any non-business income sources: rental properties, investment portfolios, or a spouse's income.

- Calculate the annual gap between projected income and projected expenses.

- Determine the lump sum needed to fund that gap for 20–30 years using a conservative withdrawal rate.

- Identify how much of that lump sum your current retirement accounts, business sale, and insurance will provide.

- Close the remaining gap with defined benefit contributions, additional insurance, or accelerated savings in your final working years.

The IRS allows owners aged 50 and older to make catch-up contributions across multiple qualified plans simultaneously. Coordinating tax planning with compensation structure and entity decisions annually is the mechanism that turns those allowances into real retirement liquidity.

Pro Tip: Run this calculation with your CPA and a financial advisor every year, not just at exit. Business value, tax law, and personal expenses all shift, and a plan built on three-year-old numbers will miss the target.

How do you integrate insurance, retirement planning, and succession into one plan?

An integrated income replacement plan has four working parts: personal protection, business protection, retirement funding, and succession structure. Most owners have pieces of each. Few have all four coordinated.

Step 1: Secure personal and business income protection first

Personal disability insurance and BOE coverage are the foundation. Without them, a health event can collapse both your household finances and your business before any retirement plan has time to mature. Add key person insurance for yourself and any other revenue-critical employees. This protects business value during the years when your retirement funding is still accumulating.

Step 2: Fund retirement aggressively in the final decade

Defined benefit and cash balance plans work best when funded consistently over 3–5 years. The contribution limits are actuarially determined, which means older owners with shorter time horizons can contribute more. COLI policies layered on top provide tax-deferred accumulation and can fund deferred compensation agreements that retain your leadership team through the transition period.

Step 3: Align legal structure with financial intent

Your business entity structure, buy-sell agreement, and estate plan must reflect your exit timeline. A buy-sell agreement without life insurance funding is a legal promise with no financial backing. An estate plan that ignores business value will create tax exposure at death. Work with a business attorney, CPA, and financial advisor as a coordinated team, not three separate conversations.

Step 4: Document everything

Historical financial and payroll records are the baseline insurers use to validate claims. Owners who cannot produce clean pre-loss financials routinely receive lower payouts or face claim disputes. Maintain organized, updated records as a standard business practice, not just a pre-claim scramble.

| Integrated approach | Primary benefit | Timeline | Complexity |

|---|---|---|---|

| Personal disability + BOE | Immediate income and cost protection | Active now | Low |

| Key person + buy-sell | Business continuity and ownership transfer | Active now | Medium |

| Defined benefit/cash balance | Accelerated tax-deferred retirement savings | 3–10 years out | Medium-high |

| COLI + deferred compensation | Leadership retention and tax-deferred growth | 5–15 years out | High |

| Buy-sell + estate plan alignment | Clean ownership transfer and tax efficiency | Exit event | High |

What mistakes do business owners make in income replacement planning?

The most costly mistake is waiting. Income replacement planning requires a 10–20 year horizon worked backward from your target exit date. Owners who start at 60 with a plan to retire at 65 have five years to accomplish what should have taken two decades. The math rarely works in their favor.

A second critical error is conflating personal and business income protection. Many owners hold a single disability policy and assume it covers both their household and their business overhead. It does not. Each requires a separate policy with its own ownership structure, benefit trigger, and payout mechanism.

Common mistakes to avoid:

- Misaligned policy ownership. A business-owned personal disability policy can make benefits taxable. A personally owned key person policy removes the business tax deduction. Ownership determines tax treatment.

- No buy-sell funding. A buy-sell agreement without a funded mechanism, typically life insurance, is unenforceable in practice. Surviving partners rarely have the liquidity to buy out an estate at fair market value.

- Ignoring business interruption risk. Business income insurance typically carries a 48–72 hour waiting period before benefits begin. Owners who do not know this often assume coverage starts immediately and are caught short.

- Fragmented advisory relationships. When your CPA, attorney, and financial advisor do not communicate, gaps appear between your tax strategy, legal structure, and insurance coverage. Those gaps cost money.

- Poor recordkeeping. Lack of documentation causes disputes and reduced payouts during insurance claims. Maintain detailed financials and payroll records as a permanent business standard.

Pro Tip: Start your income replacement plan at least 10 years before your target retirement date. The tax-advantaged vehicles that create the most retirement income, defined benefit plans and COLI, require years of consistent funding to reach their full potential.

Key Takeaways

Effective income replacement planning for business owners requires two parallel protection strategies, one for personal income and one for the business, coordinated with tax-advantaged retirement funding and a legally structured succession plan.

| Point | Details |

|---|---|

| Dual protection is required | Personal disability and business overhead insurance must be separate policies with separate ownership structures. |

| Start planning early | A 10–20 year planning horizon gives defined benefit plans and COLI time to accumulate meaningful retirement income. |

| Tax alignment matters | Matching policy ownership to financial intent prevents taxable benefits and preserves deductions. |

| Documentation protects claims | Clean historical financial and payroll records are the baseline insurers use to validate and pay claims. |

| Integrated teams close gaps | A CPA, attorney, and financial advisor working together prevent costly misalignments between tax, legal, and insurance strategies. |

Why most owners underestimate this problem

I have worked with enough established business owners to recognize a pattern. They are confident. They have built something real. And that confidence, earned through years of solving hard problems, becomes the biggest obstacle to retirement readiness.

The assumption I hear most often is some version of "I'll sell the business and live off the proceeds." That plan has three failure points. First, most businesses sell for less than owners expect, particularly when the business is owner-dependent. Second, a sale is a one-time event, not a recurring income stream, and without structure, the proceeds erode faster than projected. Third, the gap between the sale and a stable retirement income is rarely bridged by anything other than a plan built years in advance.

What I have found actually works is treating income replacement as a parallel business, one that you fund, document, and review with the same discipline you apply to your core operations. The owners who retire well are not the ones who had the most revenue. They are the ones who coordinated their insurance, their retirement vehicles, and their succession structure into a single plan with a clear exit target.

Tax synchronization is where most of the money is left on the table. Defined benefit contributions, COLI cash value, and deferred compensation agreements all interact with your entity structure and compensation decisions. Getting that coordination right in your final working decade can add hundreds of thousands of dollars to your retirement income. Getting it wrong costs the same amount.

The trend I am watching in 2026 is that more Baby Boomer owners are finally engaging with retirement income planning earlier than previous cohorts. The ones who start with a 10-year runway have options. The ones who wait for an exit trigger have very few.

— Asa

How Premier72 helps business owners build a complete income plan

Premier72 specializes in helping established business owners build income replacement plans that cover both sides of the equation: personal financial security and business continuity.

Through The Retirement Bank Method™, Premier72 works with owners to assess their current income gaps, align insurance ownership with financial intent, fund tax-advantaged retirement vehicles, and structure succession plans that protect business value through the transition. Whether you are 10 years from exit or actively planning your final chapter, Premier72 advisors coordinate the insurance, tax, and legal pieces into one plan built around your timeline and goals. Connect with a Premier72 advisor at premier72.com to start a no-obligation assessment of your income replacement readiness.

FAQ

What is income replacement planning for business owners?

Income replacement planning for business owners is the coordinated strategy of sustaining personal and business income through insurance, tax-advantaged retirement plans, and succession structures when an owner retires, becomes disabled, or exits the business.

How much income should a business owner plan to replace in retirement?

Industry benchmarks show that most owners' current financial trajectories cover only 40–50% of their lifestyle needs in retirement, meaning a well-structured plan must close a gap of 50–60% through retirement savings, insurance, and business sale proceeds.

What is the difference between personal disability insurance and business overhead expense insurance?

Personal disability insurance replaces a portion of the owner's earned income, while business overhead expense insurance covers the business's fixed costs, such as rent and payroll, during a disability. Each requires separate ownership and serves a distinct financial purpose.

When should a business owner start income replacement planning?

The optimal planning horizon is 10–20 years before the target retirement or exit date. Starting earlier allows defined benefit plans and COLI policies to accumulate the tax-deferred growth needed to fund a meaningful retirement income.

Why does insurance policy ownership matter for business owners?

Policy ownership determines who receives the tax deduction on premiums and whether benefits are taxable at payout. Misaligned ownership, such as a business owning a personal disability policy, can make benefits taxable and eliminate the intended financial protection.