A life insurance beneficiary is the person or entity you name to receive your policy's death benefit when you pass away. This designation is one of the most consequential decisions in personal financial planning, yet most people complete it in under two minutes without fully understanding the rules. Around 40% of policyholders name their spouse as the primary beneficiary. That statistic reflects a reasonable instinct, but it also shows how rarely people think beyond the obvious first choice. Premier72 works with business owners and families who need beneficiary designations that actually match their financial goals, not just their first instinct.

What is a life insurance beneficiary and how does it work?

A life insurance beneficiary is defined as any individual or legal entity you designate to receive your policy's death benefit. The insurer pays that benefit directly to the named beneficiary after your death, bypassing your estate entirely. This direct transfer is what makes the beneficiary designation so powerful in financial planning.

The designation lives inside your insurance contract, not your will. That distinction matters more than most people realize. Your will controls assets that pass through your estate. Your beneficiary designation controls who gets your life insurance proceeds, and the two documents do not need to agree. When they conflict, the beneficiary designation wins.

You can name one beneficiary or several. You can split the benefit by percentage among multiple people. You can also name a trust, a charity, or a business entity. The flexibility is broad, but each choice carries legal and financial consequences worth understanding before you sign.

Who can be named as a life insurance beneficiary?

The range of eligible beneficiaries is wider than most people expect. Insurers generally allow the following:

- Individuals: spouses, children, parents, siblings, friends, or any adult you choose

- Trusts: a revocable living trust or an irrevocable trust established for specific purposes

- Charities and nonprofits: any registered charitable organization

- Businesses: a business entity, often used in key person or buy-sell arrangements

- Estates: the policyholder's own estate, though this option triggers probate

One firm legal requirement applies across all categories. Insurers require insurable interest in the policyholder to prevent someone from profiting financially from a stranger's death. Insurable interest means the beneficiary would suffer a genuine financial or emotional loss if you died. Spouses, children, and business partners typically satisfy this standard without question.

Special cases require extra planning. Naming a minor child directly as a beneficiary creates a legal problem. Minors cannot legally manage large sums of money, so a court will appoint a guardian to control the funds until the child reaches adulthood. That process is slow, expensive, and removes your control over how the money is used. A trust is the cleaner solution. For beneficiaries with disabilities, a special needs trust protects their eligibility for government benefits like Medicaid and SSI. You can read more about planning for disabled beneficiaries to understand how these trusts work in practice.

Geography also affects your options. In community property states, spouses may hold automatic rights to life insurance proceeds, and written spousal consent is often required before you can name anyone else as primary beneficiary. States like California, Texas, and Arizona follow community property rules. Failing to get that consent can invalidate your designation entirely.

Pro Tip: Always include a full legal name, date of birth, and Social Security number for each beneficiary. Vague designations like "my children" create disputes when insurers cannot identify who qualifies.

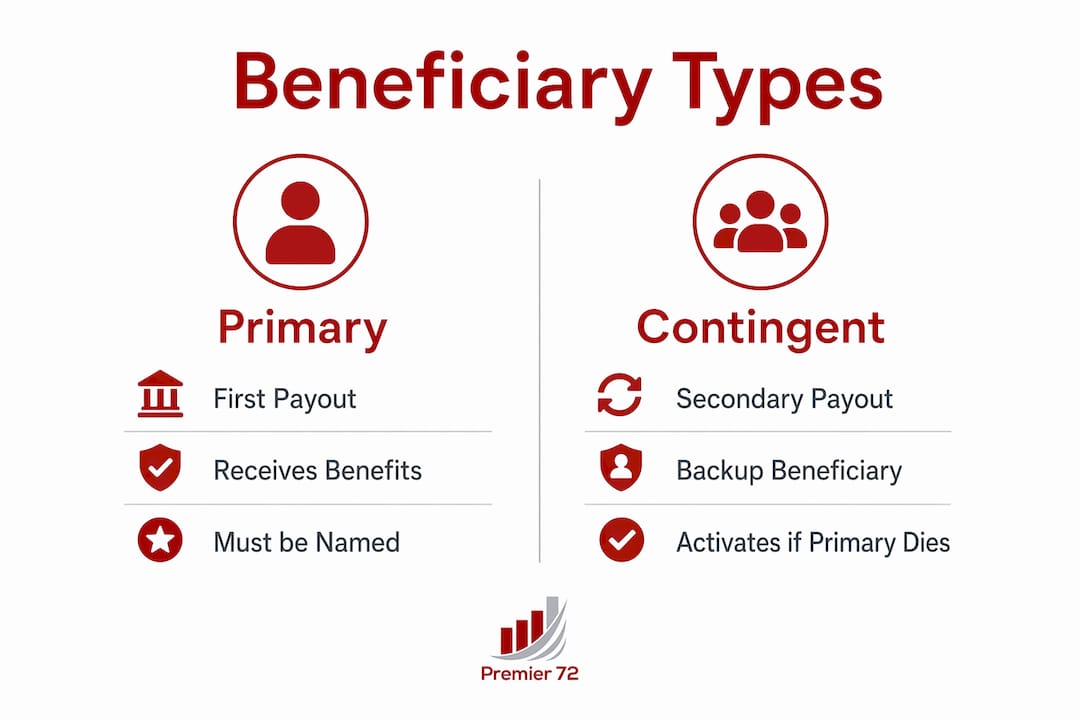

Primary vs. contingent beneficiaries: what's the difference?

Most people know they need a beneficiary. Far fewer know they need two layers of them.

A primary beneficiary receives the death benefit first. A contingent beneficiary, also called a secondary beneficiary, receives the benefit only if the primary beneficiary cannot. That "cannot" covers two main scenarios: the primary beneficiary has already died, or the primary beneficiary formally disclaims the benefit.

Here is why the contingent designation matters so much:

- If your primary beneficiary dies before you and you have no contingent named, the proceeds fall into your estate. They then go through probate, which costs time and money and exposes the funds to creditor claims.

- If your primary beneficiary is incapacitated and cannot legally accept the funds, a contingent beneficiary provides a clean alternative path.

- If your primary beneficiary disclaims the benefit for tax planning reasons, the contingent beneficiary steps in without court involvement.

- If you name multiple primary beneficiaries and one predeceases you, the contingent layer catches that share rather than leaving it in limbo.

You can name multiple people at each level. The standard approach is to assign percentages that total 100% among all primary beneficiaries, then do the same for contingent beneficiaries. Using percentages rather than fixed dollar amounts prevents calculation errors when policy values change over time. A fixed dollar amount that made sense when you bought the policy may be wildly off a decade later.

Pro Tip: Name at least one contingent beneficiary on every policy you own. Treat it as a non-negotiable step, not an optional extra.

How beneficiary designations interact with wills and estate plans

This is the area where the most expensive mistakes happen. Many people assume their will controls everything they own. For life insurance, that assumption is wrong.

Life insurance proceeds bypass probate and go directly to the named beneficiary. No court involvement. No waiting period tied to estate settlement. No exposure to creditor claims against your estate. This is one of the primary reasons life insurance is such a powerful estate planning tool.

The table below shows how beneficiary designations compare to wills across key factors:

| Factor | Beneficiary designation | Will |

|---|---|---|

| Controls life insurance proceeds | Yes | No |

| Subject to probate | No | Yes |

| Exposed to estate creditors | No | Yes |

| Can be changed without an attorney | Yes | Typically requires legal process |

| Takes effect immediately at death | Yes | After probate concludes |

The conflict risk is real. Suppose your will leaves everything to your current spouse, but your life insurance policy still names your ex-spouse from a prior marriage. The insurer pays the ex-spouse. Your will cannot override that. Beneficiary designations are contractual and legally binding on the insurer regardless of what your will says.

Trusts offer a way to coordinate both documents. You can name a trust as your beneficiary, then use the trust document to specify exactly how and when proceeds are distributed. This approach works well for blended families, minor children, or situations where you want conditions attached to the inheritance. For a deeper look at how life insurance interacts with estate tax planning, the guide on life insurance and estate taxes covers the mechanics clearly.

Common mistakes that cost families the most

Beneficiary designation errors are common, correctable, and often discovered too late.

- Naming a minor directly. Courts appoint a guardian to manage the funds, which delays distribution and removes your control over how the money is spent. A trust eliminates this problem entirely.

- Forgetting to update after major life events. Designations need review after marriage, divorce, the birth of a child, or the death of a named beneficiary. An outdated designation can send money to the wrong person with no legal remedy.

- Using fixed dollar amounts instead of percentages. A policy worth $500,000 today may be worth $750,000 in ten years. Fixed amounts create gaps or overages. Percentages always add up correctly.

- Leaving the beneficiary field blank. When no beneficiary is named, proceeds go to your estate, enter probate, and become accessible to creditors. This outcome is almost always unintended.

- Naming your estate as beneficiary. This deliberately routes proceeds through probate, which defeats one of the core advantages of life insurance.

- Failing to coordinate with your overall estate plan. A beneficiary designation that conflicts with your trust or will creates legal disputes that cost your family time and money.

The fix for all of these is a periodic review. Reviewing designations after life events keeps your wishes current and your family protected. A good rule is to review every policy at least once every three years and immediately after any major personal or financial change. The policy review checklist for families walks through exactly what to look for during that process.

You should also avoid the most common estate planning mistakes that go beyond beneficiary designations, since life insurance is only one piece of a complete estate plan.

Key Takeaways

A beneficiary designation is a legally binding contract that overrides your will and determines who receives your life insurance proceeds, making it one of the most critical documents in your financial plan.

| Point | Details |

|---|---|

| Designation overrides your will | The insurer pays the named beneficiary regardless of what your will instructs. |

| Name a contingent beneficiary | A secondary beneficiary prevents proceeds from falling into probate if the primary cannot receive them. |

| Avoid naming minors directly | Courts appoint guardians for minor beneficiaries; a trust gives you control over how funds are used. |

| Use percentages, not fixed amounts | Percentage splits stay accurate as policy values change over time. |

| Review after every major life event | Marriage, divorce, birth, or death of a beneficiary all require an immediate designation review. |

Why I think most people get this completely backward

Most people treat beneficiary designation as the last box to check when buying a life insurance policy. They fill it in quickly, file the paperwork, and never look at it again. That approach is backward. The designation is not the final step in buying insurance. It is the first step in building a legacy.

I have seen families lose hundreds of thousands of dollars because a policyholder named an ex-spouse twenty years earlier and never updated the form. I have seen business owners leave their families exposed because they named their estate as beneficiary, not realizing that choice triggers probate. These are not edge cases. They are common outcomes of treating a critical decision like a formality.

The deeper issue is that most people do not connect their beneficiary designations to their broader financial picture. Your life insurance proceeds should work in coordination with your retirement accounts, your business interests, and your estate plan. When those pieces are aligned, the death benefit does exactly what you intended. When they are not, the results can be the opposite of your wishes.

The most underrated advice I give is this: tell your beneficiaries they are named. An insurer cannot find a beneficiary who does not know to file a claim. Billions of dollars in life insurance benefits go unclaimed every year because beneficiaries simply did not know the policy existed. That is a failure of communication, not planning.

— Asa

How Premier72 approaches beneficiary planning

Life insurance beneficiary planning is not a one-time form. It is an ongoing part of your financial and legacy strategy, and it deserves the same attention as your investment portfolio or business succession plan.

Premier72 works with business owners, professionals, and families to review existing policies, identify designation gaps, and align coverage with long-term financial goals. Whether you need to coordinate a trust structure, update designations after a major life change, or build a complete legacy planning strategy, Premier72 provides the guidance to get it right. Reach out to Premier72 to schedule a beneficiary and life insurance review before your next major life event makes the decision for you.

FAQ

What is the life insurance beneficiary definition?

A life insurance beneficiary is the person or entity named in a policy to receive the death benefit when the policyholder dies. The designation is contractual and legally binding on the insurer.

Who can be a beneficiary on a life insurance policy?

Eligible beneficiaries include individuals, trusts, charities, and business entities. The person or entity must have an insurable interest in the policyholder, meaning they would suffer a genuine loss from the policyholder's death.

What is the difference between a primary and contingent beneficiary?

A primary beneficiary receives the death benefit first. A contingent beneficiary receives it only if the primary beneficiary has died or cannot accept the proceeds.

Can a beneficiary designation be changed after the policy is issued?

Yes, most life insurance policies allow you to change your beneficiary designation at any time by submitting a change form to the insurer. Irrevocable beneficiary designations are the exception and require the beneficiary's written consent to change.

Does a will override a life insurance beneficiary designation?

No. Life insurance proceeds bypass probate and go directly to the named beneficiary, regardless of what your will states. The beneficiary designation controls the proceeds as a contractual matter, not an estate matter.