Legacy planning is the intentional process of deciding how your assets, values, and personal wishes transfer to the next generation. It goes beyond writing a will. A well-built legacy plan combines legal structures, financial tools, and personal communication to protect what you have built and ensure it reaches the right people in the right way. For families preparing for generational wealth transfer, understanding what legacy planning involves is the first step toward making it real.

What is legacy planning, and why does it matter?

Legacy planning is defined as a holistic framework that incorporates personal values, philanthropic goals, and family governance alongside legal asset transfer. That definition matters because it separates legacy planning from a simple legal checklist. Most families think a will covers everything. It does not.

A will tells your heirs what they receive. A legacy plan tells them why, and what you expect them to do with it. That distinction shapes how families handle inherited wealth, businesses, and even personal heirlooms for decades after you are gone.

The importance of legacy planning grows with the size and complexity of what you own. Families with real estate, retirement accounts, a business, or charitable intentions face decisions that a standard will cannot address. Legacy planning creates the structure and the story behind those decisions.

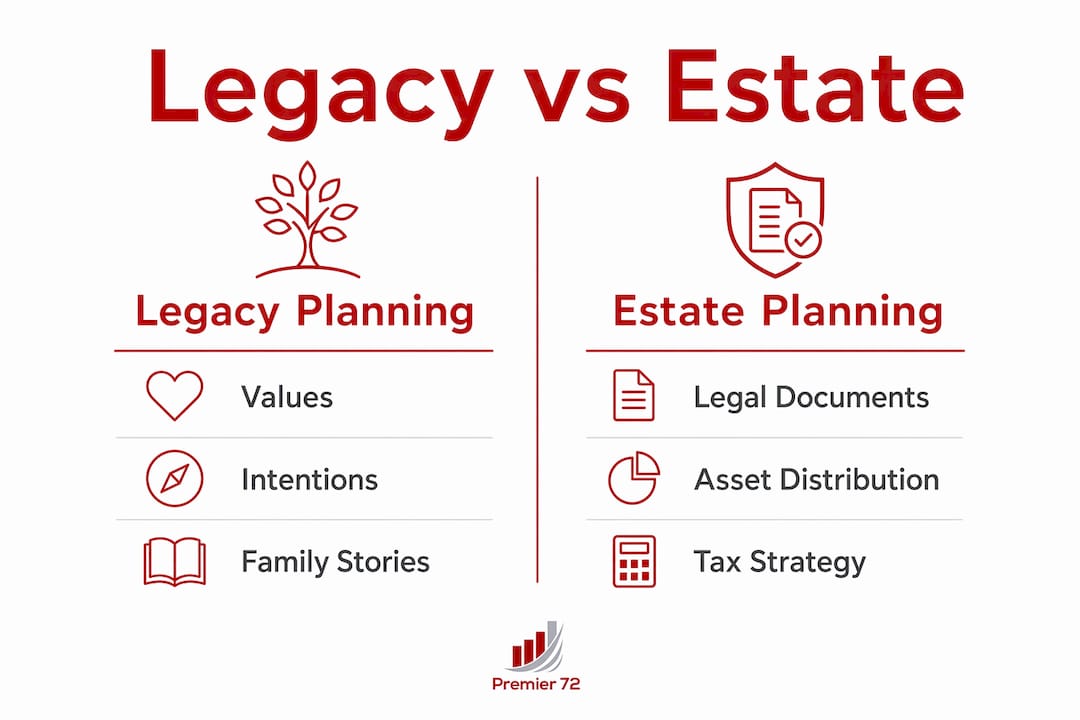

How does legacy planning differ from estate planning?

Estate planning and legacy planning are not the same thing, though they work best together. Estate planning provides the legal structure for asset distribution. Legacy planning provides the heart and purpose behind how heirs manage what they inherit.

Estate planning produces binding legal documents: wills, trusts, powers of attorney, and beneficiary designations. These documents control what happens to your assets under the law. They are non-negotiable and enforceable. Legacy planning produces something different. It produces clarity, intention, and connection.

The tools of legacy planning include:

- Ethical wills: Personal documents that share your values, life lessons, and hopes for your family. They carry no legal weight but carry enormous emotional weight.

- Letters of intent: Written guidance that explains the reasoning behind your financial decisions, helping heirs understand your expectations.

- Charitable trusts: Legal vehicles that direct assets toward causes you care about, often across multiple generations.

- Education funds with conditions: Accounts structured to support learning while encouraging specific behaviors or achievements.

- Family governance structures: Agreements that define how family members make decisions together about shared assets.

Legal documents alone cannot dictate the spirit or values behind asset management. That is the gap legacy planning fills. When you combine a solid estate plan with a thoughtful legacy plan, you give your family both the legal protection and the personal guidance they need.

What are common legacy planning strategies and tools?

Effective legacy planning strategies fall into three categories: financial tools, legal instruments, and personal communication. Each serves a different purpose, and the strongest plans use all three.

Financial tools

Charitable giving vehicles like donor-advised funds and charitable remainder trusts let you direct wealth toward causes that reflect your values while also providing tax advantages. Annuities in legacy planning offer another way to create predictable income streams for heirs or fund long-term obligations. Education funds, particularly 529 plans, allow you to invest in the next generation's future with clear purpose.

Legal instruments

Buy-sell agreements protect business interests. Life insurance policies fund those agreements and provide liquidity at death. Revocable and irrevocable trusts control how and when assets transfer. Each of these tools requires professional guidance to structure correctly.

Personal communication

Ethical wills and letters of intent articulate personal values and family narratives. These documents complement legal wills by providing emotional and cultural context. They answer the questions your heirs will ask after you are gone: Why did you make these choices? What did you want for us? What do you believe in?

Pro Tip: Involve your adult children or heirs in legacy conversations while you are still alive. Discussing expectations early prevents surprises and reduces conflict after death. A single family meeting can accomplish more than years of legal paperwork.

The most overlooked area in legacy planning is digital assets. Online accounts, cryptocurrency, intellectual property, and digital businesses all require specific instructions. Without them, heirs may lose access permanently. Add a digital asset inventory to your plan and update it annually.

How does legacy planning support business legacy preservation?

Business legacy preservation planning is one of the most complex and most neglected areas of legacy planning. An estimated 12 million businesses with $10 trillion in assets are expected to change hands in the next 10–15 years. Yet nearly 60% of business owners lack a formal succession plan. That gap represents enormous risk for families whose wealth is tied up in a business.

Business succession within a legacy plan typically takes one of three forms:

- Family transfer: Passing ownership to a family member, which requires leadership development, governance agreements, and clear documentation of roles and expectations.

- Sale to a third party: Selling the business to an outside buyer, which requires valuation, deal structure planning, and tax strategy.

- Liquidation: Closing the business and distributing assets, which is often the least favorable outcome but sometimes the most realistic one.

Starting succession planning at least 5 to 10 years before your planned exit is critical. That timeline allows you to optimize tax structures, develop internal leadership, and put key legal documents in place. Waiting until retirement is too late.

Pro Tip: A buy-sell agreement funded with life insurance is one of the most effective tools for protecting a business during ownership transition. It sets a clear price and funding mechanism before a crisis forces the issue.

Failing to align ownership rights with governance expectations can cause successors to fail despite their capability. Documenting the reasoning behind your decisions, not just the decisions themselves, is what separates a succession plan from a true business legacy plan. Premier72's estate planning guide for business owners covers this distinction in detail.

The 2026 tax environment adds urgency. Federal estate and gift tax exemptions are subject to legislative change, and business owners with significant asset values need to act before any reductions take effect. Waiting costs options.

What are real-life examples of legacy planning approaches?

Concrete examples make legacy planning easier to understand and easier to act on. The following cases illustrate how families put these strategies into practice.

-

The education-first family: A retired couple funds a 529 plan for each grandchild, but attaches a letter of intent explaining that the money is meant for education, not lifestyle. They hold an annual family meeting to discuss values around learning and work. The money comes with context, not just cash.

-

The charitable foundation: A business owner sells her company and directs a portion of the proceeds into a donor-advised fund. She names her children as successor advisors. The fund reflects her lifelong commitment to workforce development, and her children continue that work after her death.

-

The family heirloom protocol: A family creates a written inventory of meaningful personal property, from jewelry to furniture to photographs. Each item includes a note explaining its history. Heirs know what they are receiving and why it matters.

-

The letter of intent for a family business: A father writes a detailed letter explaining why he wants his son to run the business, what values he expects him to uphold, and what he hopes the company will mean to the community in 20 years. The letter sits alongside the legal succession documents and gives the son a foundation to lead from.

Transparent family communication is the thread connecting all of these examples. The families that handle wealth transfer well are not necessarily the wealthiest. They are the most intentional.

Preserving generational wealth across multiple generations requires more than financial tools. It requires shared values and clear expectations. Families that build both tend to keep more of what they earn and pass on more of what they believe.

Key Takeaways

Legacy planning combines legal structures, financial tools, and personal communication to protect assets and transfer values across generations.

| Point | Details |

|---|---|

| Legacy planning defined | It is a framework that transfers assets, values, and intentions, not just property. |

| Estate vs. legacy planning | Estate planning handles legal distribution; legacy planning adds purpose and personal guidance. |

| Start business succession early | Begin at least 5–10 years before exit to protect tax position and leadership continuity. |

| Personal documents matter | Ethical wills and letters of intent give heirs context that legal documents cannot provide. |

| Family communication is the foundation | Discussing expectations while you are alive reduces conflict and confusion after death. |

Legacy planning is an act of love, not just a legal task

I have worked with enough families to know that the ones who struggle most after a death are rarely the ones with the smallest estates. They are the ones where nobody talked about it. The will existed. The accounts were titled correctly. But nobody knew why certain decisions were made, who was supposed to lead, or what the family actually stood for.

Legacy planning as an act of love means reducing the emotional burden on the people you leave behind. It means creating a roadmap that defines not just what they receive but the values behind the assets. That framing changes everything about how families engage with the process.

The most common mistake I see is treating legacy planning as a one-time event. You do not write a letter of intent once and forget it. You update it as your family grows, as your business changes, and as your values sharpen. A legacy plan is a living document, not a filing cabinet item.

Wealth size does not determine whether you need a legacy plan. If you have people who depend on you, a business you have built, or values you want to pass on, you have a legacy worth planning. The families who start early, communicate openly, and revisit their plans regularly are the ones whose wealth and values actually survive the transfer.

— Asa

How Premier72 helps families build meaningful legacy plans

Premier72 works with business owners, professionals, and families who want to protect what they have built and pass it on with intention.

Premier72 integrates life insurance in wealth transfer, business succession planning, and personal legacy tools into a single, coordinated plan. The goal is not just to move assets from one generation to the next. The goal is to move values, clarity, and financial security alongside them. Whether you are a business owner preparing for exit or a family thinking about generational wealth for the first time, Premier72 provides the guidance to build a plan that actually works. Visit premier72.com to take the first step.

FAQ

What is the legacy planning definition in simple terms?

Legacy planning is the process of deciding how your assets, values, and personal wishes transfer to the next generation. It combines legal documents, financial tools, and personal communication into one coordinated plan.

Why does legacy planning differ from estate planning?

Estate planning creates legally binding documents that control asset distribution. Legacy planning adds the personal values, intentions, and family guidance that legal documents cannot provide.

When should you start a legacy plan?

The right time to start is when you have dependents, significant assets, or a business. For business owners, starting succession planning at least 5 to 10 years before exit gives you the most options.

What does legacy planning involve for business owners?

Business legacy preservation planning includes succession structures, buy-sell agreements, leadership development, and documentation of the values and expectations behind ownership transfer.

Do you need to be wealthy to benefit from legacy planning?

No. Any family with dependents, a business, or values they want to pass on benefits from a legacy plan. The process matters more than the dollar amount involved.