Cash value life insurance is defined as permanent life insurance that combines a death benefit with a tax-advantaged savings component that grows over time. For Baby Boomer business owners, the role of cash value life insurance in retirement goes well beyond basic protection. It creates a source of tax-free income, shields your portfolio during market downturns, and supports the legacy and liquidity goals that standard retirement accounts simply cannot address. The industry term for this strategy is a Life Insurance Retirement Plan, or LIRP, and understanding how it works is the first step toward using it well.

How does cash value accumulate and how can it be accessed in retirement?

Permanent life insurance builds cash value through a portion of each premium payment that is credited to a separate account inside the policy. That account grows tax-deferred over time, meaning you owe no taxes on the growth until you access it. The cost of the death benefit is deducted from this account each year, so the net growth depends on how the policy is designed and funded.

Accessing that cash value in retirement works in two ways: policy loans and withdrawals. Policy loans are not taxable income because you are technically borrowing against the policy, not withdrawing funds. Withdrawals up to your cost basis are also tax-free, but amounts above that basis are taxed as ordinary income. Unpaid loans reduce the death benefit paid to your beneficiaries, so tracking loan balances matters.

The timeline to build meaningful cash value is real. LIRPs typically require 10–15 years of consistent funding before they hold enough cash value to generate useful retirement income. That means a business owner who starts at age 50 may not see full benefit until their mid-60s. Starting earlier produces better results.

One of the most powerful features is the interest rate spread. When a policy credits a 6.10% dividend rate while charging only 3% loan interest, the borrowed cash still earns a positive net return inside the policy. That spread lets you access liquidity without fully surrendering growth.

Pro Tip: Design your policy with the minimum death benefit required to maximize cash value accumulation. A policy engineered for retirement income looks very different from one designed primarily for death benefit protection.

One critical design rule governs all of this. Funding a policy too aggressively triggers Modified Endowment Contract status under IRC Section 7702. MEC status eliminates the tax-free loan advantage and adds a 10% penalty on withdrawals before age 59½. Avoiding MEC classification requires careful coordination between premium amounts and the minimum death benefit.

What are the key benefits and limitations of using cash value in retirement?

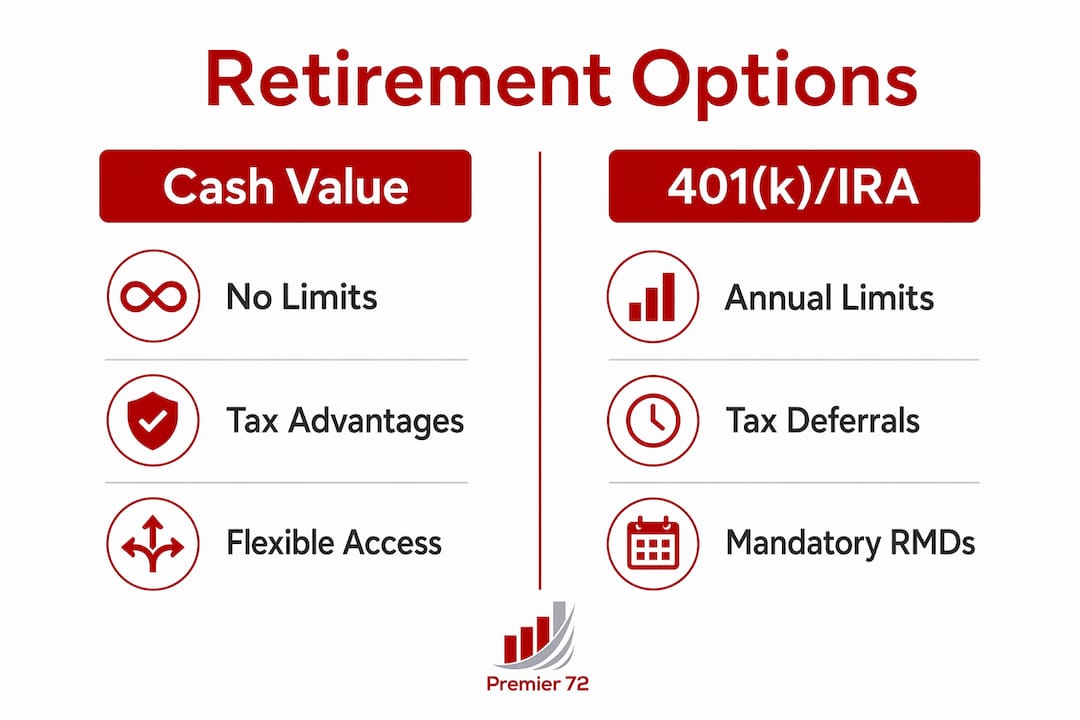

Cash value life insurance delivers benefits that no 401(k) or IRA can replicate. The core advantages include:

- Tax-free income. Policy loans do not appear as taxable income, which keeps your adjusted gross income lower and may reduce Medicare premium surcharges.

- No required minimum distributions. LIRPs carry no IRS contribution limits and no RMDs, unlike traditional retirement accounts that force withdrawals starting at age 73.

- Market protection. Using whole life loans during downturns prevents forced sales of depreciating investments. Your portfolio recovers while the policy funds your living expenses.

- Legacy transfer. The death benefit passes to heirs income-tax-free, making it a direct legacy planning tool for business owners with estate goals.

- Business continuity. Cash value can fund buy-sell agreements or provide liquidity during ownership transitions.

The limitations are equally real and worth naming directly.

- High fees in early years. Premium payments in the first several years go heavily toward commissions and cost-of-insurance charges, not cash value.

- Funding commitment. Missing premium payments can reduce cash value or lapse the policy entirely.

- Complexity. Policy design errors, including MEC violations, can eliminate the tax benefits entirely.

- Reduced death benefit. Outstanding loans at death reduce what your beneficiaries receive.

Pro Tip: Cash value life insurance is best used as a supplemental layer after maxing out your 401(k), IRA, and HSA contributions. Treat it as a diversification tool, not your primary retirement account.

| Feature | Cash value life insurance | 401(k) / IRA |

|---|---|---|

| Contribution limits | None | IRS annual limits apply |

| Tax on growth | Tax-deferred | Tax-deferred |

| Tax on access | Tax-free via loans | Taxable as ordinary income |

| Required minimum distributions | None | Required starting at age 73 |

| Death benefit | Yes, income-tax-free | No |

| Market risk | Low to moderate | Full market exposure |

Cash value insurance benefits are strongest for high earners who have already maxed out standard retirement accounts. If you still have room in a 401(k) or IRA, fill those first. The tax advantages of those accounts are simpler and cheaper to access.

How do different types of cash value policies compare?

Three policy types dominate the market for retirement planning with life insurance, and each fits a different risk profile.

Whole life insurance offers guaranteed cash value growth and fixed premiums. The growth rate is conservative but predictable. Dividends from mutual insurers like Guardian Life or MassMutual can increase cash value beyond the guaranteed floor. Whole life suits business owners who want certainty and are willing to pay higher premiums for it.

Universal life insurance offers flexible premiums and an adjustable death benefit. Cash value growth is tied to current interest rates credited by the insurer. That flexibility is useful but introduces risk. If credited rates fall or premiums are underfunded, the policy can lapse.

Indexed universal life (IUL) links cash value growth to a market index such as the S&P 500, with a floor that prevents losses and a cap that limits gains. A typical structure might offer a 0% floor and a 10–12% cap. IUL suits owners who want more growth potential than whole life provides without direct market exposure.

| Policy type | Growth mechanism | Premium flexibility | Risk level |

|---|---|---|---|

| Whole life | Guaranteed rate plus dividends | Fixed | Low |

| Universal life | Credited interest rate | Flexible | Moderate |

| Indexed universal life | Index-linked with floor and cap | Flexible | Moderate |

The right choice depends on your timeline, income stability, and tolerance for variability. A business owner with irregular cash flow may prefer the premium flexibility of IUL over the fixed commitment of whole life. An owner prioritizing certainty for estate planning typically favors whole life. Explore the whole life insurance benefits in detail before committing to a policy type.

When should Baby Boomer business owners consider this strategy?

The decision to add cash value life insurance to a retirement plan depends on specific financial conditions, not general enthusiasm for the product. Life insurance in retirement makes the most sense when you have clear debt obligations, a spouse who depends on your income, or defined legacy goals. Without those factors, the cost may outweigh the benefit.

The strongest candidates share these characteristics:

- You have maxed out your 401(k), IRA, and HSA and still have surplus income to deploy.

- You own a business and need permanent coverage for buy-sell agreements or key person protection.

- You want a tax-free income source that does not affect Social Security taxation or Medicare premiums.

- You need a buffer asset to draw from during market downturns without selling investments at a loss.

- You have a legacy goal, such as funding a trust, equalizing an estate, or leaving a tax-free inheritance.

Business owners who are still building their companies and carrying significant debt should evaluate whether the premium commitment fits their cash flow. Term life insurance remains the right choice for pure death benefit needs at lower cost. The life insurance and business legacy connection is strongest when permanent coverage aligns with both personal retirement goals and business succession plans.

A gap analysis with a qualified financial advisor is the right starting point. Map your projected retirement income from Social Security, business sale proceeds, and existing retirement accounts. If a gap exists, cash value insurance can fill part of it with tax-free income. If no gap exists, the policy may serve a legacy or liquidity role rather than an income role.

Key Takeaways

Cash value life insurance works best as a supplemental retirement tool for business owners who have maxed out traditional accounts and need tax-free income, legacy protection, and market downside coverage.

| Point | Details |

|---|---|

| Start early for best results | LIRPs need 10–15 years of funding to build meaningful retirement income. |

| Avoid MEC status | Overfunding triggers taxes and penalties that eliminate the core tax advantage. |

| Use loans, not withdrawals | Policy loans provide tax-free income without triggering ordinary income tax. |

| Layer on top of 401(k) and IRA | Max out standard retirement accounts before funding a cash value policy. |

| Match policy type to your goals | Whole life suits certainty; IUL suits growth potential with downside protection. |

What I've learned after years of working with business owners on this

Most business owners I work with encounter cash value life insurance twice. The first time, someone sells it to them as a retirement miracle. The second time, they come to me confused about why it is not performing as promised. The gap between those two experiences almost always traces back to poor policy design and unrealistic expectations.

Cash value life insurance is a genuinely useful tool. It is not a replacement for a 401(k). It is not a guaranteed path to wealth. It is a tax-efficient liquidity and legacy vehicle that works well when it is built correctly and funded consistently. The owners who benefit most treat it as one layer in a diversified retirement plan, not the whole plan.

The MEC risk is the one I see underestimated most often. An owner eager to fund aggressively pushes past the IRS limits, triggers MEC status, and loses the tax-free loan benefit entirely. At that point, the policy becomes an expensive taxable savings account. Careful policy engineering from the start prevents this entirely.

My honest advice: use cash value insurance for what it does uniquely well. It provides tax-free income that does not show up on your tax return, a death benefit that transfers wealth without income tax, and a buffer you can draw from when markets drop without selling your portfolio at the worst moment. Those three things together are worth the complexity, provided you go in with clear eyes and a well-designed policy.

— Asa

How Premier72 helps business owners build retirement income with life insurance

Premier72 works specifically with Baby Boomer business owners who need retirement income strategies that go beyond standard accounts. The firm's approach integrates cash value life insurance with business exit planning, legacy goals, and income gap analysis to build a plan that fits your actual situation.

Through The Retirement Bank Method™, Premier72 helps owners identify income gaps, design policies that avoid MEC pitfalls, and coordinate life insurance with business succession plans. If you have maxed out your 401(k) and IRA and want to know whether a LIRP fits your retirement picture, Premier72's advisory team can walk you through a personalized analysis. The goal is a retirement plan that covers income, legacy, and liquidity without leaving any of the three to chance.

FAQ

What is a Life Insurance Retirement Plan (LIRP)?

A LIRP is a permanent life insurance policy structured to maximize cash value accumulation for retirement income. It provides tax-deferred growth and tax-free access through policy loans, with no IRS contribution limits or required minimum distributions.

How does cash value life insurance differ from a 401(k)?

A 401(k) has annual IRS contribution limits, requires minimum distributions at age 73, and distributions are taxed as ordinary income. Cash value life insurance has no contribution limits, no RMDs, and policy loans are not taxable income.

What is MEC status and why does it matter?

MEC stands for Modified Endowment Contract. A policy achieves MEC status when it is funded too aggressively relative to its death benefit, which eliminates the tax-free loan advantage and adds a 10% early withdrawal penalty under IRC Section 7702.

Who benefits most from cash value life insurance in retirement?

High earners who have maxed out their 401(k), IRA, and HSA contributions benefit most. Business owners with legacy goals, buy-sell funding needs, or a desire for tax-free income that does not affect Medicare premiums are the strongest candidates.

Can I use cash value life insurance during a market downturn?

Yes. Policy loans let you draw tax-free income from the policy while your investment portfolio recovers. This approach manages sequence-of-returns risk by avoiding forced sales of depreciating assets during a downturn.