An executive bonus plan life insurance is a compensation strategy where a business pays tax-deductible bonuses to key employees to fund personally owned permanent life insurance policies. Governed by IRC Section 162, this approach lets employers deduct the bonus as a business expense while employees gain a policy they own outright. The result is a rare compensation tool that benefits both sides of the table. For business owners focused on retaining top talent and building a stronger exit position, understanding how these plans work is worth your time.

What is executive bonus plan life insurance and how does it work?

An executive bonus plan, formally called a Section 162 bonus plan, is defined as a non-qualified arrangement where the employer pays a bonus directly to fund a permanent life insurance policy owned by the employee. The employer deducts the bonus as ordinary compensation under IRC Section 162. The employee reports the bonus as taxable income and owns the policy personally.

This structure separates it from qualified plans like 401(k)s in one critical way: there are no IRS contribution caps limiting how much you can fund. The 2026 defined contribution limit for qualified plans sits at $72,000. An executive bonus plan carries no such ceiling, making it especially useful for high-earning executives who have already maxed out traditional retirement vehicles.

The policy types used are permanent life insurance products: Whole Life, Indexed Universal Life, or Variable Universal Life. These policies build cash value over time, which the employee can access for retirement income. The death benefit also passes to the employee's named beneficiaries, not the company. That personal ownership is what makes this tool genuinely attractive to executives, not just employers.

What do you need before setting up a plan?

Before implementing a bonus plan life insurance arrangement, you need to identify which employees qualify. These plans work best for key executives, top producers, or owner-adjacent talent whose departure would materially harm the business. You do not need to offer the plan to all employees, which is a meaningful advantage over qualified plans.

Key prerequisites include:

- Employee selection: Identify the specific executives or key employees the plan will cover. There is no requirement for nondiscrimination testing.

- Policy type selection: Choose a permanent life insurance product with cash value accumulation. Term life does not qualify because it builds no cash value.

- Tax planning coordination: The employee will owe income tax on the bonus in the year it is paid. Both parties need to understand this before the plan launches.

- Compensation agreement: Draft a written agreement documenting the bonus arrangement, the policy details, and any conditions attached.

- Restrictive endorsement (optional): If retention is the primary goal, a Restrictive Executive Bonus Arrangement (REBA) adds a formal endorsement filed with the insurer that limits the employee's access to the policy until vesting conditions are met.

One underappreciated advantage: these plans avoid ERISA and Department of Labor filing requirements entirely. Because the bonus is treated as current compensation, not deferred compensation, the administrative burden is far lighter than a qualified plan. For small and mid-sized businesses, that difference is significant.

| Requirement | Purpose |

|---|---|

| Key employee identification | Defines who receives the benefit; no nondiscrimination rules apply |

| Permanent life insurance policy | Provides cash value growth and death benefit for the employee |

| Written compensation agreement | Documents the arrangement and protects both parties |

| Tax planning review | Prepares the employee for income tax on the bonus amount |

| Restrictive endorsement (REBA) | Adds vesting conditions to support retention goals |

How do you execute an executive bonus plan step by step?

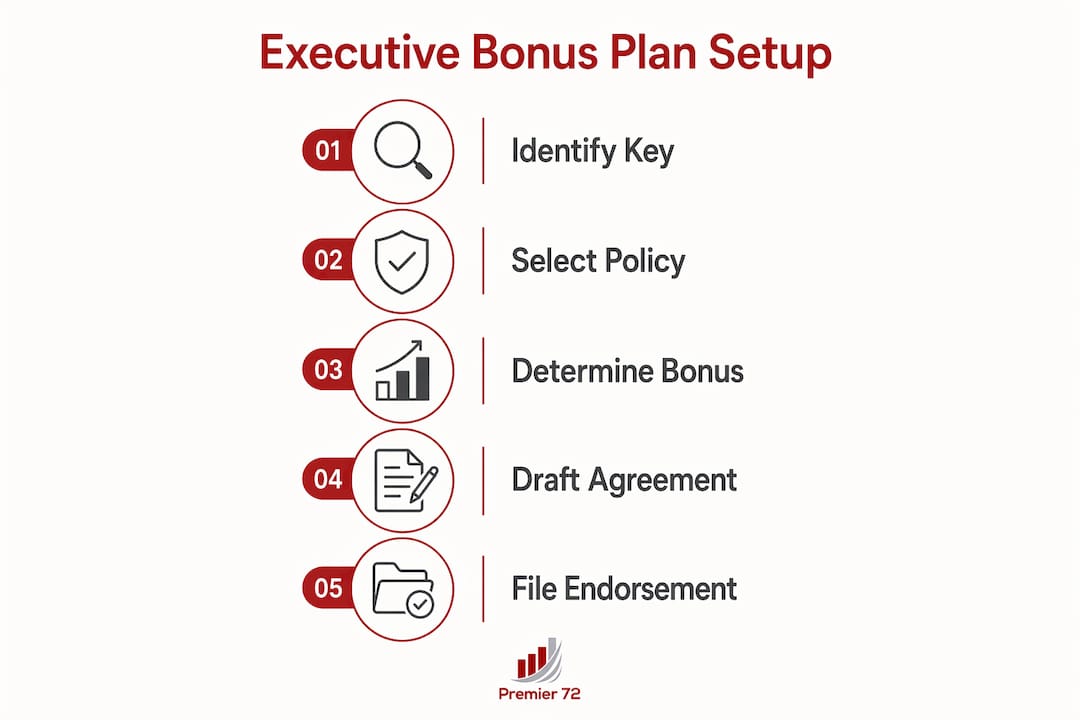

The implementation process is straightforward compared to most executive benefit structures. Follow these steps to set up and manage the plan correctly.

-

Select the executive and policy. Work with a life insurance advisor to choose the right permanent policy for the executive's age, health, and retirement timeline. The employee applies for the policy and is the named owner and insured.

-

Draft the bonus agreement. Create a written agreement specifying the bonus amount, payment schedule, and any conditions. If using a REBA, the restrictive endorsement is filed with the insurer at this stage.

-

Pay the bonus. The employer pays the bonus directly to the employee or, in some arrangements, directly to the insurance carrier. The bonus is reported as W-2 income to the employee.

-

Handle tax withholding. The employee owes income tax on the bonus. Many employers use a "double bonus" structure to cover this liability. Under a double bonus, the employer pays an additional amount to offset the employee's tax bill, making the net benefit more attractive without reducing the policy funding.

-

Employee manages the policy. The employee owns the policy, names beneficiaries, and directs cash value investment options (where applicable). The employer has no claim on the policy's cash value or death benefit.

-

Administer annually. The employer pays the bonus each year, documents the payment, and maintains the compensation agreement. There are no annual government filings required.

Pro Tip: Use the double bonus structure from day one if retention is your goal. Executives who receive a bonus but then face a surprise tax bill often feel the benefit is less valuable than it appeared. Covering the tax cost removes that friction and reinforces the plan's intent.

The cash value access the employee gains over time is a genuine retirement planning asset. Policy loans and withdrawals from a properly structured permanent policy can supplement retirement income without triggering ordinary income tax, provided the policy remains in force.

What are the tax benefits for employers and executives?

The tax structure of a Section 162 bonus plan creates real advantages on both sides. The employer deducts the full bonus amount as ordinary business compensation. There is no separate category or limitation for life insurance premiums paid this way.

For the executive, the picture is more nuanced. Employer-paid bonuses are fully taxable as income in the year paid. There is no $50,000 exclusion like the one available under group term life insurance. The executive pays income tax on the full premium value each year. That upfront tax cost is the trade-off for owning a policy with tax-deferred cash value growth and tax-advantaged retirement access.

The long-term math often favors the executive. Cash value inside a permanent life insurance policy grows tax-deferred. Withdrawals up to the policy's cost basis come out tax-free. Loans against the cash value are also not taxable income, provided the policy does not lapse. For high earners who have exhausted 401(k) and IRA contribution limits, this supplemental retirement income channel carries real weight.

Portability is another advantage that qualified plans cannot match. The executive owns the policy personally. If they leave the company, they take the policy with them. That portability makes the benefit genuinely valuable to executives, not just a retention mechanism that evaporates on departure.

For executives managing broader wealth, private banking strategies often incorporate life insurance cash value as a liquid, tax-advantaged asset alongside traditional investment portfolios.

What mistakes should business owners avoid?

The most common mistake is misunderstanding who bears the tax burden. Owner-employees face a specific trap: the IRS requires that bonus payments represent reasonable compensation for services rendered. If the owner-employee's total compensation already exceeds what the IRS considers reasonable, the deduction may be challenged. Careful planning with a tax advisor is not optional here.

Failing to document a restrictive endorsement properly is the fastest way to lose the retention benefit of a REBA. If the endorsement is not filed with the insurer and reflected in the compensation agreement, the employee retains full access to the policy from day one. The "golden handcuffs" effect disappears entirely, and the employer has paid for a benefit with no retention strings attached.

Other pitfalls to watch for:

- Skipping the double bonus: Employees who owe unexpected income tax on the premium bonus may resent the benefit rather than value it. Budget for the double bonus if you want the plan to motivate.

- Choosing the wrong policy type: Term life does not work. Only permanent policies with cash value accumulation serve the plan's purpose.

- Assuming the plan runs itself: Annual documentation, bonus payments, and policy reviews require consistent attention. The administrative burden is light compared to qualified plans, but it is not zero.

- Ignoring the employee's perspective: A plan the executive does not understand is a plan that does not retain anyone. Clear communication about the policy's value, tax treatment, and retirement potential is part of the implementation.

How does a REBA enhance executive retention?

A Restrictive Executive Bonus Arrangement (REBA) is a Section 162 bonus plan with an added layer of control. The employer files a restrictive endorsement with the insurer that prevents the executive from surrendering, borrowing against, or transferring the policy without the employer's written consent. That restriction stays in place until defined vesting conditions are met.

Vesting triggers vary by design. Common structures tie vesting to years of service, reaching a specific age, or achieving a retirement milestone. Until those conditions are satisfied, the executive has a policy they can see growing but cannot fully access. That structure creates a genuine incentive to stay.

The legal effect is enforceable. Because the endorsement is filed with the insurer, not just documented in a side agreement, the restriction has teeth. Simple executive bonus plans offer immediate ownership and access. REBAs trade that immediacy for a retention mechanism the employer controls.

Pro Tip: If your primary goal is retention rather than pure compensation, start with a REBA. The added complexity is minimal, and the vesting structure gives you a meaningful tool to keep key people through a planned transition or sale.

The REBA structure fits naturally into business continuity planning. For owners preparing for an exit, keeping key executives in place through the transition period is often the difference between a clean sale and a distressed one.

Key Takeaways

An executive bonus plan life insurance is the most tax-efficient way for business owners to reward key executives with personally owned life insurance while deducting the full cost as ordinary compensation.

| Point | Details |

|---|---|

| IRC Section 162 governs the plan | Employer deducts bonuses; employee reports them as taxable income and owns the policy. |

| No contribution caps apply | Unlike 401(k)s, there is no IRS limit on how much can be funded each year. |

| REBA adds retention control | Restrictive endorsements prevent policy access until vesting, creating enforceable retention incentives. |

| Double bonus covers employee taxes | Employers can pay an extra amount to offset the executive's income tax on the premium bonus. |

| Cash value builds retirement income | Tax-deferred growth and tax-advantaged loans make the policy a real supplemental retirement asset. |

Why I think most business owners underuse this tool

Business owners tend to overlook executive bonus plans because they assume the tax complexity outweighs the benefit. That assumption is wrong, and I have seen it cost owners real talent.

The plan is genuinely simple compared to a SERP or a deferred compensation arrangement. There are no ERISA filings, no nondiscrimination testing, and no trust structure required. The employer pays a bonus, deducts it, and the executive owns a growing asset. The documentation is straightforward when done correctly from the start.

What I find most underappreciated is the portability angle. Executives know that most company-sponsored benefits disappear when they leave. A personally owned life insurance policy does not. That permanence changes how executives perceive the benefit, and it changes how they weigh the decision to stay.

The one area where I see plans fail is communication. Owners implement the plan, pay the bonus, and assume the executive understands the value. They rarely do without a clear explanation of the cash value growth, the retirement income potential, and the tax treatment. Spending thirty minutes walking the executive through the policy mechanics pays back in years of loyalty.

For owners using Premier72's Retirement Bank Method, integrating an executive bonus plan into the broader exit and succession strategy is a natural fit. Retaining key people through a transition is as important as the financial structure of the deal itself.

— Asa

How Premier72 helps you build an executive bonus plan

Business owners who want to implement a Section 162 bonus plan need more than a life insurance policy. They need a plan that fits their compensation goals, tax situation, and retention priorities.

Premier72 works with business owners to design executive bonus plans that align with their broader financial and exit strategies. From selecting the right permanent life insurance policy to structuring a REBA with proper documentation, Premier72 provides guidance at every stage. If you are considering key employee life insurance as part of your compensation strategy, the right structure matters as much as the product. Contact Premier72 at premier72.com to schedule a consultation and build a plan that works for your business and your key people.

FAQ

What is an executive bonus plan life insurance?

An executive bonus plan life insurance is a compensation arrangement under IRC Section 162 where an employer pays a tax-deductible bonus to fund a permanent life insurance policy owned by a key employee.

Is the bonus taxable to the executive?

Yes. The bonus is fully taxable as ordinary income to the executive in the year it is paid, with no exclusion available. Many employers add a double bonus to cover this tax cost.

How does a REBA differ from a standard executive bonus plan?

A REBA adds a restrictive endorsement filed with the insurer that limits the executive's access to the policy's cash value until specific vesting conditions are met, creating an enforceable retention incentive.

Are there contribution limits on executive bonus plans?

No. Unlike 401(k)s and other qualified plans, Section 162 bonus plans carry no IRS contribution caps, making them well-suited for high-earning executives who have maxed out traditional retirement accounts.

Can owner-employees use executive bonus plans?

Owner-employees can participate, but the IRS requires that bonus payments represent reasonable compensation for services rendered. Owners should work with a tax advisor to confirm deductibility before implementing the plan.