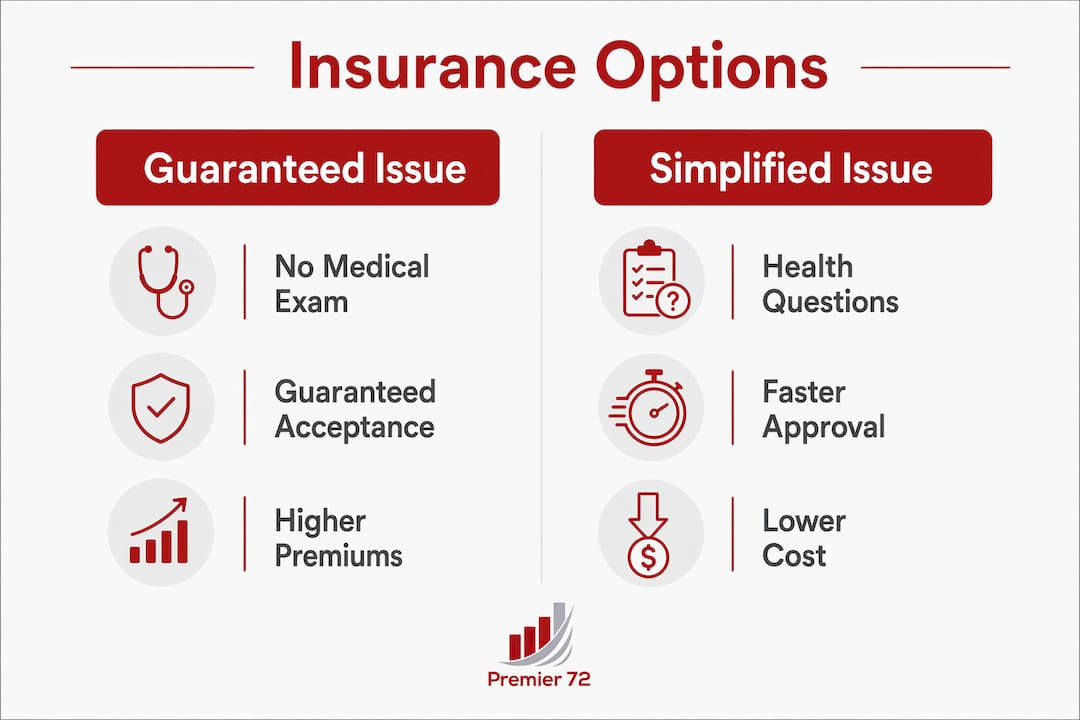

Guaranteed issue life insurance is a permanent whole life policy that accepts any applicant within the eligible age range, with no medical exam and no health questions asked. Coverage amounts typically run from $5,000 to $25,000, and eligibility generally spans ages 45 to 85. The industry also calls this product "guaranteed acceptance life insurance," and both terms refer to the same policy structure. For adults over 50 who have been declined for traditional coverage due to health conditions, this policy type removes the single biggest barrier to getting insured. The trade-off is real: premiums run higher, coverage limits are modest, and a graded death benefit period applies during the first two to three years.

What is guaranteed issue life insurance and how does it work?

Guaranteed issue life insurance works through automatic acceptance. You apply, you meet the age requirement, and the insurer approves you. No doctor visits, no blood draws, no health questionnaires. The application process is straightforward by design.

Here is the core mechanics in plain terms:

- Apply within the eligible age window. Most carriers set this between 50 and 85, though some start at 45. Age is the only qualifying factor.

- Choose your coverage amount. Face amounts typically range from $5,000 to $25,000. This is not a policy built for income replacement. It covers final expenses.

- Lock in your premium. Premiums are fixed at issue based on your age, gender, and the coverage amount you select. They do not increase over time.

- Understand the graded death benefit. Most policies include a 2 to 3 year waiting period before the full face value pays out on natural death. If you die from natural causes during this window, your beneficiaries receive the premiums paid plus a small amount of interest, not the full benefit.

- Keep paying premiums. Coverage is permanent as long as premiums are paid. A lapse cancels the policy, and you lose the premiums paid during the graded period.

The graded benefit period is the detail that surprises most buyers. It exists because the insurer accepts everyone, including people in poor health, without knowing their risk level. The waiting period protects the insurer from immediate large claims.

Pro Tip: If you die from an accident during the graded period, many policies pay the full face value immediately. Read the accidental death clause carefully before you sign.

What are the benefits and limitations of guaranteed issue coverage?

Guaranteed issue coverage delivers one benefit no other policy type can match: acceptance is certain. If you are within the age range, you cannot be turned down. That single feature makes this policy worth considering for adults who have exhausted other options.

Key benefits

- No health barriers. Chronic illness, diabetes, heart disease, and prior cancer diagnoses do not disqualify you.

- No medical exam. There are no lab tests, no doctor visits, and no waiting on underwriting decisions.

- Permanent coverage. Unlike term life, this policy does not expire. It stays in force for life as long as you pay premiums.

- Fixed premiums. Your rate is set at issue and never increases, which helps with budgeting on a fixed income.

- Final expense coverage. The policy is designed to cover end-of-life costs such as funeral arrangements, outstanding medical bills, and small debts.

Key limitations

- High premiums per dollar of coverage. Because the insurer assumes full health risk, premiums are significantly higher than medically underwritten alternatives. You pay more for less.

- Low coverage ceiling. The $25,000 maximum is not enough to replace income or pay off a mortgage. This is a final expense tool, not a wealth transfer vehicle.

- Graded death benefit. The waiting period means the policy is not suitable for someone with a terminal diagnosis expecting to die within two years.

- Policy lapse risk. Missing premium payments during the graded period results in cancellation and loss of all premiums paid.

The difference between guaranteed issue and simplified issue policies matters here. Simplified issue requires you to answer a short set of health questions, but skips the medical exam. Applicants who qualify for simplified issue typically get better value because the insurer has some health data to price the risk more accurately. If you can qualify for simplified issue, that option usually costs less for the same coverage amount.

Pro Tip: Ask your adviser about simplified issue policies before defaulting to guaranteed issue. A few health questions could save you hundreds of dollars per year in premiums.

How does guaranteed issue compare to other life insurance options?

Understanding where guaranteed issue fits among life insurance policy types helps you make a better decision. Three main options exist for adults over 50: guaranteed issue, simplified issue, and traditional whole life.

| Feature | Guaranteed issue | Simplified issue | Traditional whole life |

|---|---|---|---|

| Medical exam required | No | No | Yes |

| Health questions required | No | Yes (short form) | Yes (full underwriting) |

| Acceptance guaranteed | Yes | Not guaranteed | Not guaranteed |

| Typical coverage range | $5,000–$25,000 | $5,000–$50,000 | $25,000 and up |

| Premium cost | Highest | Moderate | Lowest for healthy applicants |

| Graded death benefit | Yes (2–3 years) | Sometimes | Rarely |

| Cash value accumulation | Minimal | Varies | Yes |

| Best for | Uninsurable applicants | Moderate health issues | Healthy applicants |

Traditional whole life requires full medical underwriting. Healthy applicants get the best rates, but anyone with significant health conditions risks denial. Simplified issue sits in the middle. It asks health questions but skips the physical exam, and it accepts a broader range of health profiles than traditional whole life.

Guaranteed issue sits at the end of the spectrum. It accepts everyone within the age range, but the cost-to-benefit ratio is intentionally unfavorable because the insurer assumes full health risk with no information. Adults who can qualify for either of the other two options should consider those first. Guaranteed issue is the right choice only when other options are unavailable.

For adults interested in how permanent life insurance builds long-term value, traditional whole life offers cash value growth that guaranteed issue does not meaningfully provide.

What should you consider before choosing a guaranteed issue policy?

Choosing the right guaranteed issue plan requires more than comparing premium quotes. Several practical factors determine whether this policy actually serves your needs.

- Affordability over the long term. Premiums are fixed, but they must be paid consistently for life. Calculate whether the monthly cost fits your retirement budget without strain. A policy you cannot sustain is worse than no policy.

- Your current health status. If you have not been formally declined for other coverage, apply for simplified issue or traditional whole life first. Many adults assume they cannot qualify when they actually can.

- The graded benefit timeline. If you have a serious illness and a short life expectancy, the graded period may mean your beneficiaries receive only a fraction of the face value. This policy is not appropriate for imminent terminal conditions.

- Policy fine print on exclusions. Read the suicide clause and the accidental death provision carefully. Accidental death often receives full coverage even during the graded period, while natural death does not. These distinctions affect what your family actually receives.

- Coverage amount versus actual final expenses. The average funeral in the United States costs several thousand dollars, and outstanding medical bills can add more. Match your coverage amount to a realistic estimate of your final expenses rather than choosing the maximum by default.

- Consulting a trusted adviser. A financial adviser or insurance professional can pull quotes across multiple carriers and help you compare total cost of ownership. Family members who will be affected by the benefit should also be part of the conversation.

Pro Tip: Ask for an illustration showing total premiums paid versus the death benefit over a 10 and 20 year period. This single comparison reveals the true cost of guaranteed issue coverage and helps you decide if it makes financial sense.

Consistent premium payment is the single most critical factor once you own the policy. Policy lapse results in complete loss of all premiums paid during the graded period. Set up automatic payments to eliminate that risk.

For adults thinking about how life insurance fits into broader family financial planning, coverage decisions connect directly to estate goals and legacy intentions.

Key Takeaways

Guaranteed issue life insurance is the right tool only when other coverage options have been exhausted, and understanding its cost structure before you buy prevents expensive surprises.

| Point | Details |

|---|---|

| Guaranteed acceptance | Any applicant within the eligible age range (typically 50–85) is approved with no health questions. |

| Graded death benefit | Natural death during the first 2–3 years pays back premiums plus interest, not the full face value. |

| Higher premiums | Costs run significantly higher than medically underwritten policies because the insurer assumes full health risk. |

| Explore alternatives first | Simplified issue policies offer better value for applicants who can answer basic health questions. |

| Premium consistency matters | Missing payments during the graded period cancels the policy and forfeits all premiums paid. |

The honest truth about guaranteed issue life insurance

Guaranteed issue coverage is the most misunderstood product in the life insurance market. Adults over 50 often come to it with the assumption that it works like any other life insurance policy, and that misunderstanding costs families real money.

The graded death benefit catches people off guard more than any other feature. I have seen families expect a full payout, only to learn the policy was purchased eight months before death and the benefit returned only premiums. That outcome is not a failure of the product. It is a failure of expectation-setting. The policy does exactly what it says it does. The problem is that most buyers do not read the terms carefully enough before signing.

My honest recommendation is this: treat guaranteed issue as a last resort, not a first call. If you have any reasonable chance of qualifying for simplified issue coverage, pursue that path first. The savings in premiums over a decade are substantial, and the coverage limits are often higher. Guaranteed issue earns its place for adults who have been declined elsewhere, who have serious health conditions, and who need some coverage rather than none.

The other misconception worth addressing is that guaranteed issue is an investment. It is not. The cash value accumulation in these policies is minimal. The purpose is narrow: cover funeral costs and final bills so your family does not absorb that financial burden. When you frame it that way, the higher premium becomes easier to accept. You are not building wealth. You are protecting your family from a specific, predictable expense.

Start the conversation early. The older you are at issue, the higher your premium. Every year you wait costs more.

— Asa

How Premier72 helps you find the right life insurance fit

Adults over 50 face a genuinely complex set of decisions when evaluating life insurance options. The difference between guaranteed issue, simplified issue, and traditional whole life is not always obvious, and the wrong choice can mean paying far more than necessary for coverage that does not fully serve your needs.

Premier72 works directly with older adults, business owners, and families to evaluate life insurance options as part of a broader legacy and retirement planning strategy. The team helps you assess whether guaranteed issue is actually your best option or whether a simplified issue or whole life policy fits your health profile and budget better. Premier72 also covers key person coverage, buy-sell funding, and income protection for those with ongoing business interests. If you want a clear picture of your options without the sales pressure, Premier72 is the right starting point.

FAQ

What is the age range for guaranteed issue life insurance?

Most guaranteed issue policies are available to adults between ages 45 and 85. Age is the only qualifying factor, and no health information is required.

What happens if I die during the graded benefit period?

If death results from natural causes during the first 2–3 years, beneficiaries receive the premiums paid plus a small amount of interest. Accidental death often triggers the full face value even during this period.

Is guaranteed issue life insurance worth the cost?

For adults who cannot qualify for other coverage, it provides essential final expense protection. For those who can qualify for simplified issue policies, that option typically delivers better value at a lower premium.

What is the difference between guaranteed issue and simplified issue life insurance?

Simplified issue requires answers to a short set of health questions but skips the medical exam. It generally costs less and offers higher coverage limits than guaranteed issue for applicants who qualify.

Can I lose my guaranteed issue policy after I buy it?

Yes. Missing premium payments cancels the policy. If cancellation occurs during the graded period, all premiums paid are forfeited. Setting up automatic payments protects against this outcome.