Survivorship life insurance is defined as a joint permanent policy covering two individuals that pays a single death benefit only after both insured people have died. Unlike traditional life insurance, which pays upon the first death, this structure is built for estate and legacy planning, not for replacing income during a surviving spouse's lifetime. Business owners, professionals, and high-net-worth families use it to fund estate taxes, protect heirs, and transfer wealth efficiently. The IRS treats qualifying death benefits as income-tax-free, which makes the payout even more powerful as a planning tool.

What is survivorship life insurance and how does it work?

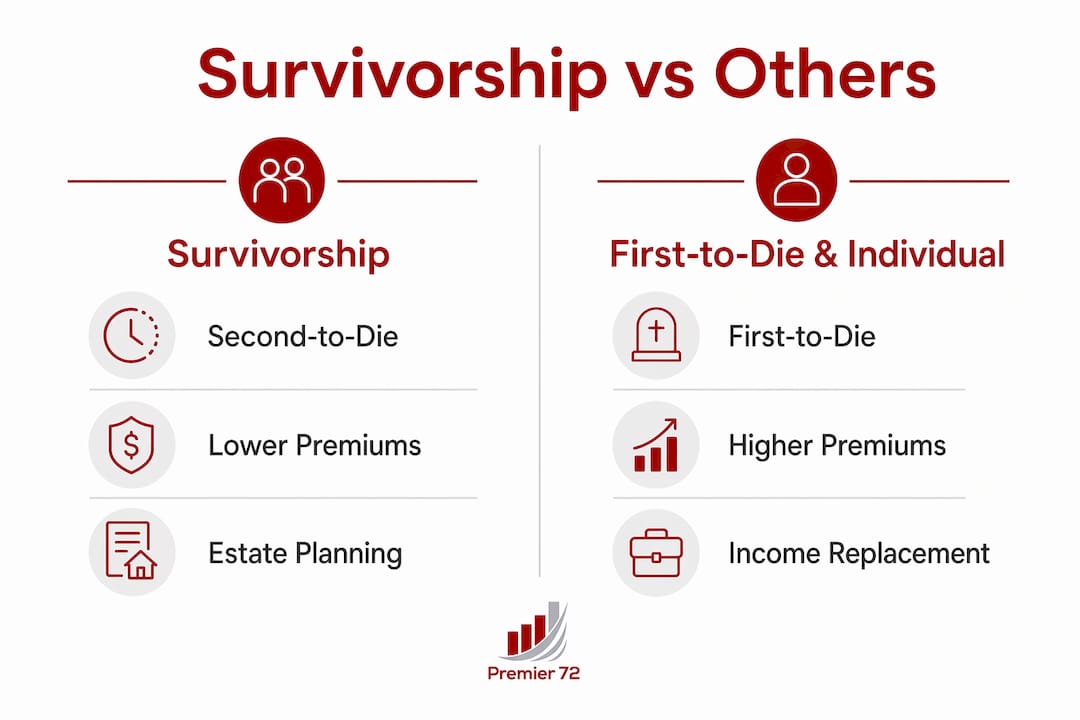

Survivorship life insurance, also called second-to-die insurance, pays a death benefit only after the second insured person passes away. That delayed payout is the defining feature of the policy. It means the surviving spouse receives no direct benefit from the policy during their lifetime. The policy exists to protect what comes after both lives end.

The mechanics are straightforward. Two people, typically spouses or business partners, are covered under one policy. Premiums are paid throughout both lifetimes. When the second insured dies, the named beneficiaries receive the full death benefit. Those beneficiaries are usually heirs, a trust, or a business entity.

How survivorship differs from first-to-die and individual policies

A first-to-die joint policy pays when the first insured dies, functioning more like income replacement for the survivor. Individual policies each cover one person and pay independently. Survivorship insurance does neither. It holds the benefit in reserve until both insured are gone, which is exactly what estate planning requires.

The cost structure reflects this difference. Premiums are typically lower than the combined cost of two separate permanent policies. The insurer carries less immediate risk because payout is delayed across two lifetimes. That pricing advantage makes survivorship insurance attractive for couples who want large death benefits without paying for two full individual policies.

Most survivorship policies are permanent, meaning they include a cash value component. That cash value grows over time and can be accessed, but with important limits. The flexible premium design and cash value component provide long-term options but require disciplined management to maintain death benefit security.

Pro Tip: Ask your advisor to model the policy's internal rate of return at different death ages. This shows whether the premium cost justifies the death benefit for your specific estate planning goal.

Key benefits of survivorship life insurance for estate and business planning

The practical value of a survivorship policy shows up in four specific planning scenarios. Each one addresses a financial gap that other insurance structures cannot fill as efficiently.

- Estate tax liquidity. When both spouses die, heirs often face a large estate tax bill due within nine months of death. A survivorship policy delivers a tax-free death benefit precisely at that moment, giving heirs cash to pay the IRS without selling family assets or a business at a discount.

- Business succession funding. Partners in a closely held business can use a survivorship policy to fund a buy-sell agreement. When both founding partners are gone, the policy payout transfers ownership cleanly to surviving partners or heirs. Premier72 works with business owners on exactly this kind of buy-sell funding structure.

- Special needs trusts. Parents of a child with a disability need to fund a trust that will support that child for decades after both parents are gone. A survivorship policy is purpose-built for this. The payout funds the trust at the exact moment it is needed most.

- Charitable legacy gifting. Couples who want to leave a significant gift to a foundation or nonprofit can use a survivorship policy to guarantee the gift size. The charity is named as beneficiary, and the death benefit funds charitable bequests without reducing the estate passed to heirs.

The income-tax-free nature of the death benefit applies in all four scenarios, assuming the policy is structured correctly. That tax advantage compounds the value of every dollar of coverage purchased.

Important considerations when choosing a survivorship policy

Survivorship insurance is not the right tool for every situation. Several factors determine whether it fits your plan, and getting them wrong is costly.

Health, underwriting, and the insurability hedge

Both insured individuals go through underwriting, but the insurer prices risk across two lives combined. When one partner is uninsurable but the other is healthy, premiums may remain affordable because the insurer averages risk across both lifetimes. This is one of the most underused advantages of survivorship insurance. A couple where one spouse has a serious health condition can still obtain meaningful coverage that would be impossible or prohibitively expensive with two individual policies.

Survivorship insurance also acts as an insurability hedge. If one partner becomes uninsurable after the policy is issued, both remain covered. That protection cannot be replicated with separate policies.

Ownership structure and the ILIT

Who owns the policy matters as much as the policy itself. If the insured own the policy personally, the death benefit may be included in their taxable estate. That defeats the purpose of using insurance to provide estate liquidity. Placing the policy in an Irrevocable Life Insurance Trust removes the proceeds from the taxable estate entirely. The ILIT owns the policy, pays the premiums, and receives the death benefit outside the estate. Heirs then receive the funds through the trust, free of estate tax.

- Beneficiary designations must be reviewed regularly. A policy naming the wrong beneficiary, or no beneficiary, creates legal and tax problems that take years to resolve.

- Cash value withdrawals carry real risk. Excessive withdrawals can undermine the death benefit and potentially cause the policy to lapse. Cash value is a long-term stability feature, not a savings account.

- Modified Endowment Contract classification is a hidden trap. Overfunding a policy too quickly can trigger MEC status, which changes the tax treatment of withdrawals and loans. Careful monitoring of contributions prevents this.

Pro Tip: Review your survivorship policy's in-force illustration every three years. Rising cost-of-insurance charges inside the policy can erode cash value faster than expected, especially in older policies.

How survivorship insurance supports business continuity and legacy

Business owners face a specific version of the legacy problem. When two founding partners or a married couple who co-own a business both die, the company faces a leadership vacuum and a liquidity crisis simultaneously. Survivorship insurance addresses both.

- Fund the buy-sell agreement. A survivorship policy provides the capital to execute a pre-agreed ownership transfer. Surviving partners or heirs use the death benefit to buy out the deceased owners' shares at a predetermined price. This prevents forced sales and family disputes.

- Protect the business from estate taxes. A business interest is often the largest asset in an estate and the hardest to liquidate quickly. The policy payout gives heirs the cash to cover estate taxes without selling the business.

- Complement key person coverage. Survivorship insurance works alongside individual key person policies. Key person coverage protects the business during the owners' lifetimes. Survivorship coverage protects the transfer of ownership after both are gone.

- Support retirement and wealth transfer planning. For business owners using Premier72's Retirement Bank Method™, survivorship insurance fits into a broader plan that converts a successful business into a transferable retirement asset. The policy guarantees a legacy transfer even if the business sale does not generate the expected proceeds.

- Extend legacy beyond the estate. A business legacy strategy that includes survivorship insurance gives heirs options. They can sell the business, keep it, or use the death benefit to fund a new venture. The policy creates flexibility that a business alone cannot provide.

Survivorship insurance is not a standalone solution. It works best as one layer in a coordinated plan that includes proper business valuation, a funded buy-sell agreement, and a clear succession structure.

Key Takeaways

Survivorship life insurance is the most cost-effective permanent coverage structure for estate liquidity, business succession, and legacy transfer after both insured individuals have died.

| Point | Details |

|---|---|

| Second-to-die payout | The death benefit pays only after both insured die, making it a legacy and estate tool, not income replacement. |

| Lower premium cost | Premiums are typically lower than two separate permanent policies because payout is delayed across two lifetimes. |

| ILIT ownership matters | Placing the policy in an Irrevocable Life Insurance Trust removes proceeds from the taxable estate. |

| Insurability hedge | One unhealthy partner can still be covered because insurers price risk across both lives combined. |

| Cash value discipline | Withdrawals can trigger tax consequences and reduce the death benefit, so cash value requires careful management. |

Why most business owners misread this policy

The most common mistake I see is treating survivorship insurance like a safety net for the surviving spouse. It is not. The surviving spouse gets nothing from this policy while they are alive. That is not a flaw. It is the design. The policy is built to protect the people and causes that matter after both of you are gone.

What surprises most business owners is the insurability angle. I have worked with couples where one partner was uninsurable due to a serious diagnosis. They assumed life insurance was off the table entirely. A survivorship policy changed that. The healthy partner's insurability carried the underwriting, and the couple secured a meaningful death benefit at a reasonable premium. That outcome is simply not available with two individual policies.

The ILIT piece is where I see the most costly errors. Owners buy a large survivorship policy, feel good about the coverage, and never think about who owns it. Years later, the death benefit lands inside a taxable estate and the heirs lose a significant portion to taxes. The policy did its job. The ownership structure did not. Getting the structure right from day one costs almost nothing compared to fixing it later.

Survivorship insurance is also not a substitute for a funded buy-sell agreement or a proper succession plan. It is the funding mechanism that makes those plans work. Premier72 treats it as one piece of a coordinated exit and legacy strategy, not a product to be sold in isolation.

— Asa

How Premier72 helps you plan with survivorship insurance

Survivorship life insurance is a precise planning tool. Getting it right requires more than selecting a policy. It requires a coordinated strategy that connects the policy to your estate plan, your business succession structure, and your long-term retirement goals.

Premier72 works with business owners and professionals to design survivorship insurance strategies that fit their full financial picture. That includes ownership structure, beneficiary design, ILIT coordination, and integration with buy-sell agreements and exit planning. If you are building a legacy or preparing your business for succession, the right coverage structure makes the difference between a plan that works and one that falls apart under pressure. Visit Premier72 to schedule a consultation and build a plan that protects what you have built.

FAQ

What is the main purpose of survivorship life insurance?

Survivorship life insurance is designed to provide estate liquidity and legacy transfer after both insured individuals have died. It is not an income replacement tool for the surviving spouse.

How does survivorship insurance differ from joint life insurance?

Joint life insurance can refer to either first-to-die or second-to-die policies. Survivorship insurance is specifically a second-to-die policy, meaning it pays only after both insured individuals have passed away.

Is the death benefit from a survivorship policy taxable?

The death benefit is typically received free of federal income tax. However, if the insured own the policy personally, the proceeds may be included in the taxable estate, which is why ILIT ownership is recommended.

Who benefits most from a survivorship life insurance policy?

High-net-worth couples, business partners, and parents of special needs dependents benefit most. The policy works best when the goal is estate tax liquidity, business succession funding, or long-term trust funding after both insured are gone.

Can survivorship insurance cover one unhealthy partner?

Yes. Because insurers price risk across two lives, one unhealthy partner can often be included on a survivorship policy when the other is insurable, making coverage accessible in situations where individual policies would be denied or unaffordable.